One useful relationship that helps identify turning points in the USD Index is a look at foreign equities. Foreign stocks will often outperform the U.S. markets when the USD is weak; part of the reason for this is that foreign markets are very sensitive to inflation, so when their currencies advance relative to the USD, their inflation rates fall and their equities climb. Typically, we see a turn in foreign markets prior to a turning point in the USD, which was the case this summer. The iShares Emerging Markets ETF (EEM) bottomed on June 1st, with the USD Index topping on July 24th. Since the summer lows, the EEM has rallied nearly 20%, while the USD fell more than 6.5% before finding its footing in September. Over the last three months the USD Index has staged what looks like a very weak recovery rally, and the breakout in the EEM may be signaling that the USD Index is set to begin another leg down.

Go East Young Man

Since late 2010, emerging market stocks have been underperforming the S&P 500 on a consistent basis (see lower red panel below). However, the underperformance appears to be coming to a close as the ratio of EEM to the S&P 500 ETF (SPY) has just broken a 2-year downtrend and likely signals that the USD is set to decline further since its top in July (USD Index shown inverted and in green in top panel below).

Source: Bloomberg

It does appear that the best returns heading into 2013 will come from foreign markets, as their recoveries since this summer’s lows are very strong with broad-based market participation. For example, European, Middle Eastern, and Asian (EMEA) countries have many indexes with more than 70% of their members above their 200-day moving averages (200d MA), shown near the middle of the table below. Moreover, you may observe that a great number of EMEA country indexes have hit 52-week highs in the last month (middle column below, highlighted green). Also encouraging is that the monthly MACD, often a great tool for identifying bear and bull market bottoms and tops, indicates BUY signals for most of the country indexes. While some of the EMEA markets have had a tough year, the average country index is up over 10%, with some strong standouts like Pakistan (48.5%), Turkey (48.8%), and Germany (28.76%) up considerably year-to-date.

Source: Bloomberg

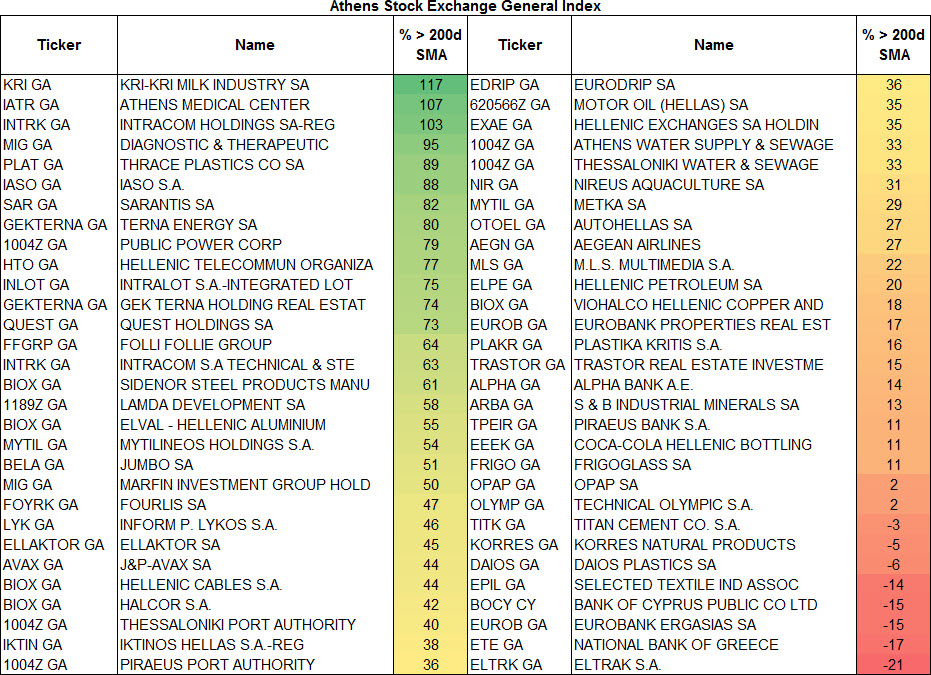

Many European markets are on fire as European leaders are finally working together to solve their collective debt crisis. Highlighting the liftoff seen in European equities is the fact that the 60-stock Athens Stock Exchange General Index features 87% of its members above their 200d MA; to show how sharp the rally has been in Greek stocks over the last few months, the average stock in the Athens Stock Exchange Index is 39% above its 200d MA, with some more than double the price of their 200d MA.

Source: Bloomberg

Zeroing in on Asia, we also see a strong recovery underway as many country indexes hit 52-week highs in the last month, with many seeing their monthly MACD’s turn from SELL to BUY.

Source: Bloomberg

Conversely, country stock exchanges in the Americas show weaker overall breadth and far more monthly MACD SELL signals.

Source: Bloomberg

USD set for Sharp Decline in H1 2013?

Moving back to what messages the emerging markets are signaling, it appears the USD Index is on the verge of breaking a rising trend line support (red line below), and if it weakens below the key 78 level, it looks like we will have a completed head-and-shoulders top, which would project a return to the 2011 summer lows near -. The Fed’s decision this week to expand QE3 with B monthly purchases of UST’s is likely a major catalyst that would lead to USD weakness in 2013.

Source: Bloomberg

Another slide in the USD would likely be bullish for gold, which is seen by many as the world’s most sound currency, and not merely a commodity. In the race to debase, with global QE in full swing (see previous article), we’ve reached a breakout in the combined balance sheets of the world’s four big central banks, which likely spells positive news for gold in the weeks ahead.

Source: Bloomberg

Summary

While the U.S. equity markets have been the world’s strong performer over the last two years, that appears to be changing as emerging markets are hitting fresh 52-week highs and have been outperforming the S&P 500 since September, with Europe, China, and Japan now in recovery mode. The outperformance of foreign equities has broader implications beyond relative performance to U.S. stocks, as they likely are portending a weak USD going forward. The technical landscape for the USD Index suggests as much, as it appears to be rolling over and in the process of forming a head-and-shoulders top. Completion of this formation would target a decline in the USD Index back to the 2011 summer lows. The implications of a slide in the USD would lead to higher import inflation, and so consumer discretionary spending may take a hit as consumers spend more on food and energy and less on non-essentials, which could impact retail sales and GDP. This appears to be the big risk for the U.S. economy in the first half of 2013 – a weak USD leading to higher inflation and less consumer spending. Adding that to any drag resulting from going over the fiscal cliff, in full or part, could put the U.S. economy at risk of its first recession since 2009. There are two sides to every coin, and while the U.S. economy may suffer from a weak USD, gold would likely benefit, being also aided by further expansion in global central bank balance sheets as global currency wars continue.