Central Bank Intervention

While most of the central banks across the globe were raising rates since 2010 after the big global reflationary boom of 2009, they have now switched gears and been slashing rates over the past year to spur economic growth. As seen below, central banks across the globe have slashed interest rates with Brazil leading the pack with its 3% (300 basis points) cut in the last six months alone (see green columns).

Source: Bloomberg

Outside of central bank rate cuts we have seen monetary expansion and in certain countries more fiscal stimulus. Two of the world’s three biggest economies are ramping up the stimulus engines as outlined below.

ECB Recap:

- The ECB since late July has been outlining a series of powerful policy responses aimed at arresting the debt crisis. Thursday’s press conference took an important step further in that direction.

- The old SMP is dead and the new one is called “OMT” (Outright Monetary Transactions).

- Bond purchases are unlimited, the ECB will accept the same legal status as private investors, buys will be sterilized, and purchases will focus on short-end of the curve (3yrs and under).

- The ECB is creating two classes of “bailout” so they are in effect making it easier for countries to request assistance. A country can ask for a Portugal/Ireland/Greece-like full program or instead seek a precautionary program (Enhanced Conditions Credit Line) – this latter option could make it easier for Spain or Italy to ask for help (it doesn’t have the stigma of a full Greece-like package).

- In addition to the OMT, collateral standards for ECB liquidity operations were eased Thursday in such a way so as to remove the risk of a Spain downgrade by Moody’s. Also, the ECB will now will accept securities denominated in currencies other than the euro.

- Rates were left unchanged and the growth outlook was cut.

China Recap:

- The Shanghai Comp surged 3.7% overnight, its largest single day advance since January 17th 2012 after the federal government in Beijing announced a ~0B stimulus spending plan.

- The National Development & Reform Commission, China’s top planning agency, said it approved plans to build 1,254 miles of roads as well as plans for subway projects in 18 cities.

- A slew of local governments have unveiled spending proposals in the last several months but this was the first to come from the federal government in Beijing and thus is considered more credible.

Monetary Stimulus Is Leading to Healing in Credit & Equity Markets

With all the central bank action over the last few months we are seeing a definitive payoff in the credit markets that came under stress this summer. Bloomberg’s Financial Conditions Index for the U.S. (red line, top panel) and for Europe (red line, bottom panel) are well off their 2012 lows and have nearly erased the decline that began during the U.S.’s debt ceiling fiasco in 2011. Along with the improved health in the credit markets has been a direct spillover into the equity markets as the S&P 500 hit a 4-year high (black line, top panel) while the Euro Stoxx 50 Index (black line, bottom panel) is assaulting its 2012 highs.

Source: Bloomberg

Looking at some key credit spreads, USD and EUR 2-year swap spreads have completely collapsed back to their lows over the past two years while the Ted Spread and LIBOR-OIS spread continue their declining trend that began at the start of the year.

Source: Bloomberg

Sovereign bond yields across Europe have come off their highs as credit tensions ease. Shown below are 5-year bond yields for select countries and their historical range over the last six months. As seen below, every single yield (blue dot) is below its 6-month average (orange dot) as the healing in Europe has occurred across the board.

Source: Bloomberg

Central Bank Intervention Pushing Reflationary Train Out of the Station

Big macro shifts in economics and financial markets are broad based, meaning they impact every economy and every market. This is clearly shown above as every single European 5-yr bond has declined in yield (bonds rallied) from their highs over the last six months. The way I look for broad based movements in currencies and precious metals is to not look at one currency pair (or gold priced in only one currency) but rather a basket of currency pairs and gold pairs. True trends in currencies and precious metals are broad-based and we are currently witnessing movements in gold and the USD that suggests the current reflationary wave is in fact broad-based and has a considerable amount of momentum building.

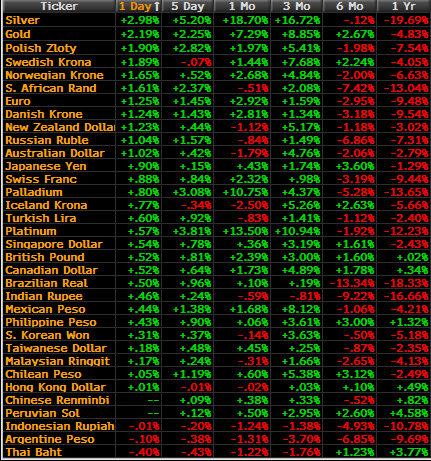

For example, I look at gold priced in 30 world currencies and today gold is up against every single one of them (far left column, “1-day”). But more than that, gold’s strength today was not a one-day event but rather looking at the table shows a theme that has been building now for 6 months, which is gold setting the stage for its next major advance. When gold first bottoms you see it show strength relative to a basket of currencies over a short time period while its prior weakness shows negative rates of change on a weekly or monthly basis. However, as its strength continues to improve you begin to see not just positive performance across a single day or week, but now across a month or quarter or half year. This is the story we see in gold as the strength it began to display six months ago continued to build to the point where gold is up across the bulk of world currencies over 1 day, 5 days, 1 month, 3 months, or even 6 months. For a sign that this bullish shift in gold’s momentum is turning we would first see weakness in the far left columns which would eventually spill over into the far right columns, which clearly isn’t the case at the moment. As such, it appears that gold bulls have complete control of the reins.

Gold’s Performance Relative to World Currencies

Source: Bloomberg

Similar to the picture for gold is the picture for world currencies relative to the USD. Shown below is the performance over different time periods for precious metals and foreign currencies relative to gold. Like gold we see foreign currencies beginning to strengthen relative to the USD on a short-term (1-day, 5-day) basis as well as on an intermediate basis (1-month, 3-month) as seen by the green columns on the left. It appears that gold sniffed out the USD top first as gold’s table above shows widespread positive 6-month performances while foreign currencies are predominantly down relative to the USD over a 6-month and 1-year time frames. Given the USD Index broke major trend line support this week I would expect foreign currencies and precious metals to continue to strengthen relative to the USD.

Foreign Currency Performance Relative to the USD

Source: Bloomberg

The seeds of reflation sown by central banks and governments appear to finally be arresting the weakness that began in the middle of 2011 as gold has broken out (bottom panel) while the USD Index has broken down (2nd panel from the bottom, shown inverted). We are likely to see further signs of reflation ahead as the 10-yr UST yield (black line), the Korean Kospi Index which is highly sensitive to Chinese activity (blue line), copper prices (orange line, middle panel), and US 5-yr breakeven inflation rates all appear to be challenging their resistance lines that have been in place seen 2011. Given the trend line breaks in gold and the USD, it is likely in the weeks ahead that we will have further confirmation that the reflationary train is leaving the station and gathering steam.

Source: Bloomberg

Conclusion

The customary response to an economy overheating and suffering from high inflation is to raise interest rates and reduce fiscal stimulus. This was the global outcome to the reflationary boom that came from the response to the 2008 debt crisis. However, global central banks began raising interest rates as early as late 2009 and well into 2010 and early 2011 and effectively brought down inflationary levels and economic growth as well. Inflationary pressures and economic activity levels have declined enough to prompt central banks to slash interest rates and in some countries launch another round of fiscal stimulus. The Eurozone finally appears to be getting its act together as they address their sovereign debt crisis and the moves announced this week are a step in that direction. China’s economy has been decelerating for some time now and it appears the decline has been enough to prompt the government to act with a new round of fiscal stimulus. All of these collective developments are coalescing around a central macro theme of reflation. The market is already telling us the train has left the station as seen by a breakdown in the USD Index and a breakout in gold, and it appears only a matter of time before other markets confirm the reflationary moves of gold and the USD.