Earlier today the anonymous author of Wall Street Rant sent me a link to a commentary that asks the intriguing question Is This Bull Market Fundamentally Driven?

The approach used in the commentary to answer the question is to do some simple math with the Cyclically Adjusted P/E (CAPE) popularized by Yale Professor Robert Shiller.

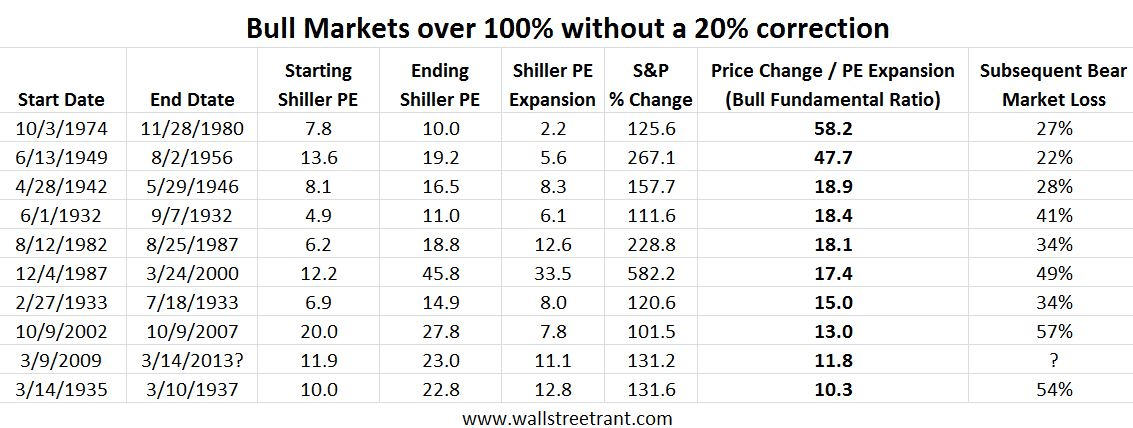

Here is the key concept and accompanying data:

Fundamentally driven bull markets should rely more on cyclically adjusted earnings growth and less on investors' willingness to pay ever increasing multiples on those earnings. To look into this I decided to focus only on bull markets of 100% or more. I looked at the Starting and Ending Shiller PE using Robert Shiller's online data and updated it with daily pricing data for the important dates (as he only has monthly prices). Then I divided the Bull Market gains by the amount of PE expansion to see how much gains investors were receiving per unit of PE expansion. The results are below, sorted by most fundamentally driven to least fundamentally driven. The results are quite interesting.

Take a look at the 1974-1980 Bull Market compared to today.... The magnitude of the advance is similar between the two, but the 1974-1980 advance only relied on a PE expansion of 2.2 versus 11.1 today. You will also notice that those that relied least on PE expansion tended to experience smaller subsequent bear markets. The top 5 averaged a bear market loss of 30.4% versus the bottom 4 which averaged a 48.5% loss. If history is any guide people should expect that the next bear market will be deeper than average because this bull market is lacking a fundamental underpinning.

In an email exchange with the author I pointed out that the current bull market came within a hair's breadth of a 20% decline at 19.39% in early October 2011, based on daily closes.

I received the following thoughtful response:

It's true that 10/2/11 only missed the 20% threshold by a hair (someone also made a post about it crossing if you count intraday) but that is also the case in many other bull markets. For instance, for the 1987-2000 bull market in 1998 the market went from 1186.75 to 957.28 or a fall of 19.34% (and using intraday highs and lows you can get beyond the 20% threshold as well...intraday 7/20/1998 to 10/8/1998). Or in 1990 the market fell from 368.95 to 295.46 or 19.9%.Then also for the 1974-1980 Bull market the market went from 107.46 on 12/31/76 to 86.9 on 3/6/1978 or down 19.1%. Haven't looked at all the others but I'm sure there are similar pullbacks....now that I look at these things maybe this is why the seemingly arbitrary 20% level is often used. Also, If 2011 was the start of a bull market then it's the second highest starting PE ratio for a bull market by a long shot (only 2002 matches it...and it is a big outlier).

Interesting perspective!

Source: Advisor Perspectives