Governments and economists around the world have not figured out that what the world economy is suffering from, to varying degrees, is “high-priced fuel syndrome”.

High-priced fuel syndrome has a number of symptoms:

- Slow economic growth, or contraction

- People in discretionary industries laid off from work

- High unemployment rates

- Debt defaults (or huge government intervention to prevent debt defaults)

- Governments in increasingly poor financial condition

- Declining home and business property values

- Rising food prices

- Lower tolerance for immigrants

- Huge difficulty in funding retirement programs, programs for disabled, and regular pension plans

- Rising international tensions related to energy supply

The countries with the most problem with high-priced fuel syndrome are the industrialized countries that are big importers of oil. This is the case because oil has been a particularly high-priced fuel in the past few years. Importing high-priced oil adds challenges of its own, since funds used for imported oil flow out of the country.

While oil is the biggest culprit in high-priced fuel syndrome, high-priced fuels of other sorts can play a role as well. Natural gas is recently high-priced in Europe and Japan, but not the USA. The higher natural gas price contributes to a higher average energy cost level for these countries. High-priced renewables, such as off-shore wind and solar photovoltaic, can be expected to act in a similar fashion, because they add to the price challenge customers face.

At this point, Europe is hardest-hit by high-priced fuel syndrome. In part this is because Europe is a big importer of both oil and gas, and both are high-priced. European countries have also encouraged the use of high-priced renewables, adding to their difficulties.

While many people have laughed at the issue of the world “running out of oil” (or natural gas, or some other substitute fuel), it seems to me that they have basically missed the point. There is always lots of fuel in the ground, or available through devices we create that produce “renewable” fuel. The major issue is that the fuel becomes too expensive for the economy to afford.

The United States, Europe, and Japan were industrialized back when fuels were cheap, in the pre-1972 era (Figure 1, above). The cost structure of government welfare programs (such as Social Security, Medicare, unemployment) also assume that the economy will continue as it did with low-priced fuels. Substituting ever more-expensive fuels can be expected to push a country toward economic contraction, reduction in programs that the economy can no longer afford, and the symptoms listed above.

Why We are Encountering Rising Fuel Prices

When companies begin extracting oil (or natural gas, or coal), they start with the easiest, cheapest-to-extract first. In Figure 2, oil (or natural gas or coal) extraction starts at the top of the triangle, and gradually works down the triangle.

As we require more and more fuel, we gradually seek out less-desirable sources of fuels. These fuels tend to be slower to extract, and are more expensive for what we get. They are often more polluting as well.

Oil is the fuel that we recently have had a problem with easy-to-extract supply running low. We had a somewhat similar problem in the mid 1970s and early 1980s. At that point there was still plenty of cheap oil left in areas where we had not yet drilled (Alaska, North Sea and Mexico, for example), so the problem was temporary, lasting only until we could drill more oil.

This time, the problem seems to be permanent. The chief executives of oil companies Total and Shell have been quoted as saying, “The days of so-called ‘easy oil’ are over, making it harder to meet demand without complicated and expensive projects.” (Voss, 2007). Examples of such expensive-to-extract oil include deep-water oil and tight oil that must be “fracked”. The fact that the cheap oil is mostly gone is the major reason why oil prices are higher than they were five or ten years ago. If oil prices had not risen, it is likely that the amount of oil extracted each year would be declining.

There are alternative fuels such as ethanol and biodiesel, but they also tend to be expensive.

Natural gas and coal aren’t immediate substitutes for oil. For example, they won’t act as fuels in most of today’s cars, trucks and airplanes. While there are long-term possibilities for substitution, the high-priced fuel syndrome is today’s problem, not a future problem.

Rising Fuel Costs Cause the Economy to Contract

There are a number of ways rising fuel costs can cause the economy to contract. The problem is that consumers’ incomes don’t rise, just because oil prices rise. If consumers are required to pay more for a necessity, they will cut back on discretionary goods and services. A few examples:

Food prices. If oil prices rise, the price of food tends to rise as well, because oil is used in many ways in producing food: cultivation of fields, planting fields, chemical sprays (herbicides, pesticides), transporting soil amendments, harvesting fields, and transporting food to market.

Low-income customers tend to be disproportionately affected by rising food prices. They especially tend to cut back on discretionary spending, such as buying a car or going out to a restaurant, in order to be able to afford enough food. As a result, workers in discretionary industries are laid off.

Commuting cost. If oil cost rises, the price of auto travel rises. Some auto travel, particularly commuting, is a necessity. Consumers, particularly lower-income consumers, tend to cut back on discretionary spending, such as vacation trips, to afford essential trips.

Businesses. Businesses are affected in multiple ways by rising oil prices. First, businesses in discretionary industries find that their “unit-sales” are down, because customers are spending more on food and commuting, as a result, need to cut back elsewhere. Lower unit-sales are likely to lead to lay-offs.

In many instances, businesses also use oil directly in the products they sell. For example, airlines use jet fuel. If oil prices rise, they have they either face lower profits, or need to raise prices to recoup their higher costs. This type of price increase further stresses customers’ budgets.

Electricity. While the current US problem is oil prices, rising electricity prices would be expected to have a similar effect. Every business today uses electricity in various ways–electric lights, running computers, running elevators, operating tools of various sorts. If electricity costs rise because of higher natural gas prices or because of greater renewable surcharges, it will raise the cost of the product produced.

Businesses again have the choice of raising the price to consumers, or facing declining profits. If they raise prices, they will be less competitive with suppliers from other countries, who may not be facing rising electricity costs, if their source of electricity (perhaps coal or nuclear) is not rising in price as fast.

If electricity prices rise, consumers’ budgets will be stressed in a similar way to the way that they are stressed by rising oil prices. This, too, can be expected to lead to a cutback in discretionary expenditures.

Follow-on effects. Laid-off workers may move in with relatives and cut back on driving to save on costs. This helps reduce demand for both homes and automobiles. With less demand for homes, housing prices may decline, especially in parts of the country with significant layoffs and plentiful housing supply.

Laid-off workers may default on loans, creating financial distress for banks. Even people who still have jobs may find the hours they work reduced, so that their take-home pay is lower. They too may cut back on discretionary expenditures.

Impact on Governments

Governments suffering from high-priced energy syndrome can expect a number of negative impacts:

- Laid-off workers expect to collect unemployment benefits. If there are other kinds of benefits that they might collect under some other program (disability, retirement, low-income assistance), they will want them as well.

- If citizens are working fewer hours or laid off, the amount of taxes they pay is lower.

- Banks and other industries are likely to need bailing out, as borrowers default on loans.

- The government will be faced with direct increases in costs, because the government uses oil to fuel its autos and jets.

- The government will face increasing costs on products it buys that use oil, such as asphalt for highway projects.

- Local governments may face reduced tax revenue because of declining home and business property values.

Figure 4 below shows US Federal Government Income and Outlays, in recent years:

It is clear from Figure 4 that income had dropped at the same time outlay has risen. Even though the crisis is supposedly past, there is still a huge gap between income and outlays. Outlays in recent years are higher than would be expected based on pre 2005 trends, while revenues are lower than would be expected. Revenue would need to be more than 50% higher, to match outgo, for 2009 through 2012 fiscal years.

The amounts shown in Figure 4 are consolidated, so include programs such as Social Security and Medicare, besides “on budget” spending. How many readers could afford to contribute 50% more than they currently pay for the sum of (Federal Income Taxes + Social Security + Medicare funding)? If the government were to actually raise taxes this much, there would be a huge new round of lay-offs, because consumers would find their after-tax income much reduced, leading to even more cuts in discretionary spending.

Needless to say, the US government will do everything in its power to cover up its problems. In a later section, we will discuss how this huge deficit is being hidden.

Note that the only years during which US Federal Government income exceeded outgo in Figure 4 are 1998 through 2001. These years approximately coincide with the time period when historical oil prices were at the lowest level in recent years (Figure 5, below).

Impacts of the Oil Price Increase in 2006 – 2008 Period

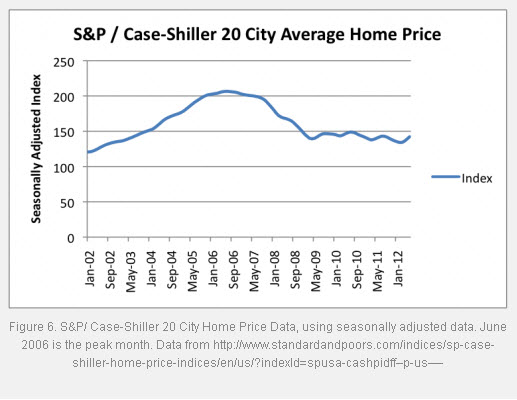

While most people now don’t think of oil prices in 2006 as being high, according to Figure 5, oil prices already had more than doubled from 2002 levels by 2006. If we look back at the financial situation in 2006-2007, we see impacts very similar to what we would expect from rising oil prices.

Sub-prime borrowers began to default as early as 2006 (Bernanke, 2007). As mentioned earlier, it was people who were on the “edge” financially who were most at risk of defaults on home loans. Sub-prime borrowers would seem to be on the “edge” financially and thus were particularly as risk, because they lacked the financial qualifications to obtain “prime” interest rates.

Home prices started to drop in 2006 as well (Figure 6, above), and they haven’t been able to recover yet. We don’t think of homes as being discretionary spending items, but people can’t move into more expensive homes unless their incomes are rising. First-time buyers will also tend to put off purchases, if their financial situation is tight. The construction industry was one of the industries to face large lay-offs.

Defaults on loans caused considerable problems in the financial industry. “Short sales” (in which the sales price of a home is insufficient to pay off the remaining mortgage because the price of a home has fallen) also caused losses to the financial industry. The financial system was not set up with the idea that there may be a systemic problem of this sort. As a result, many banks found themselves in financial difficulty and needed governmental bailouts.

Other industries, such as auto manufacturing and insurance, also required bailouts. These patterns are precisely what one might expect from rising oil prices.

I make arguments similar to these in Oil Supply Limits and the Continuing Financial Crisis. James Hamilton (2009) has shown that the rise in oil prices alone were sufficient to bring on recession in the 2007-2008 recession.

One other important factor also affecting the 2006 to 2008 period was target interest rates. The Federal Reserve Open Market Committee (FOMC) raised interest rates during the 2004 to 2006 period (Figure 7, below).

The basic idea in manipulating interest rates is that low interest rates are supposed to increase economic activity, because low interest rates make it less expensive to buy a car, using a loan, or to take out a home improvement loan. They also make it less expensive for businesses to finance expansion with a loan. Higher interest rates are supposed to decrease economic activity, because of the opposite impact.

Ludlum (2009) reviewed the minutes of the Federal Reserve Open Market Committee (FOMC). The FOMC noticed rising energy and food prices as early as December 9, 2003. It wasn’t until June 2004, though, that the FOMC first raised interest rates, in an attempt to “damp down” demand for oil. The committee’s view (not stated in the minutes, but implied by rising interest rates) was that the rapid expansion of the US economy was leading to rising oil and food prices. The expectation was that raising interest rates would damp down US demand for oil, and bring inflationary pressures affecting oil prices under control. The FOMC continued to raise interest rates by 0.25% at each of its meetings (the minutes repeatedly comment about rising energy and food prices), until the target interest rate reached 5.25% in June 2006). The FOMC did not start bringing interest rates down again until September 2007.

If the problem were really rising US demand for oil, this approach might have worked. In fact, the real issue was rising oil demand elsewhere, especially China, India and other Asian countries. China had joined the World Trade Organization in December 2001, and was ramping up its exports starting in 2002 and 2003. It also didn’t help that world oil supply was not rising very quickly, so rising demand led to rising oil prices.

The combination of higher interest rates and rising oil prices provided a “double whammy” to the US economy, helping push the US economy into recession. Europe and Japan also experienced major recession. The parts of the world with rapidly growing oil consumption generally did not experience recession.

The Growing Economy Problem

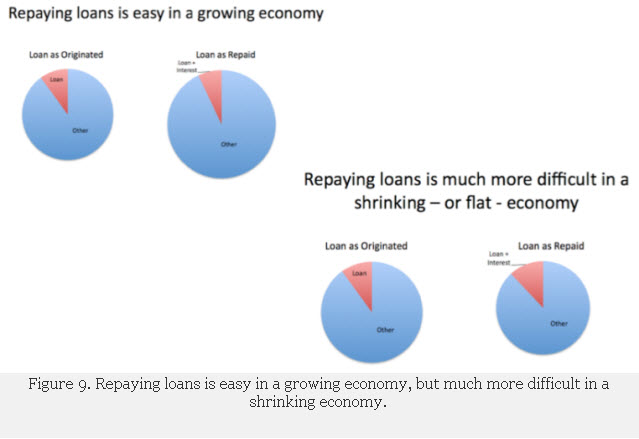

At least part of the reason for the High-Priced Fuel Syndrome is the fact that with all of the world’s debt, there is a need for growth to continue indefinitely. In a growing economy, it is as if we can always “borrow from the future,” because the future is always bigger and better than the past. We start running into huge problems if this is not true.

Part of the problem is that repaying loans is difficult in a shrinking economy (Figure 9), because less funds are “left over” after loan repayment. If we think of the situation as a government whose revenues start declining, we can understand what the problem is with repaying debt, plus interest on that debt. (Arguably inflation could play a role for a while, but lenders soon would catch on, and require higher interest to compensate for inflation.)

As long as the economy grows each year (and government revenue is higher), it makes sense for the government (and many others) to keep borrowing. But if the economy starts shrinking, we have a serious issue, because the government not only needs to stop borrowing more, but it also has to face the prospect of repaying what it already owes.

The situation is not too different for individual borrowers and for businesses. For individual borrowers, the risk is of being laid off from work, and not being able to find new job. For businesses, it is the risk of fewer buyers for their products, and because of this, less revenue in the future. With less revenue, fixed costs become a larger and larger share of total revenue, making it harder to repay debt.

Thus, in a shrinking (or even a flat) economy, debt defaults become more and more of a problem. Banks find themselves in more and more financial difficulty. This is basically the issue referred to earlier, with respect to high oil prices causing loan defaults.

Paying for Social Security and Medicare benefits is another area where growth makes a big difference. If an economy is growing, there is always a growing population of young workers to pay for benefits to the elderly. If the number of workers shrinks relative to the retired population because of high unemployment or few children, funding becomes a problem. This is yet another area where we have been counting on growth to continue indefinitely, to keep the model functioning as planned.

Recent Government Cover Up of High-Priced Fuel Syndrome

We noted above that the Federal Reserve raised interest rates in the 2004 to 2006 period, in an apparent attempt to damp down oil demand. Starting in September 2007, the FOMC took the opposite tack. Instead of raising interest rates, they brought them down, bringing them as close to zero as they could by late 2008. See Figure 7, above. The intent of this move was to stimulate the economy, by making borrowing less expensive.

Then the Federal Reserve decided to go further, and take up what it called Quantitative Easing, which is what other people call “printing money”—buying the government’s own debt, and some related debt. Target interest rates affected only short-term debt. Through the use of Quantitative Easing, it hoped to lower longer-term interest rates, as well, and thus provide even more of the low-interest rate benefit to potential borrowers. The United Kingdom and the Eurozone are taking a somewhat similar approach.

A major reason for Quantitative Easing (besides the stated business reasons for decreasing interest rates) seems to be lowering the amount of interest payments that the government itself would need to pay. This would help reduce the big gap between governmental outgo and income (Figure 4, above).

A second reason for Quantitative Easing is that it was a way of enabling the huge amount of deficit spending taking place. Without Quantitative Easing, the government would have had to go, “hat in hand”, to the world market, asking for additional loans. There might be a possibility of not all of the loans being sold, or of higher interest rates being required. By buying back a large share of the US’s own debt, it was able to make certain that interest rates would stay low, and that there would be an adequate market for the debt.

Impacts of Government Cover-up

One problem with artificially low interest rates is that the interest rates, in effect, steal from one segment of society, and use it to subsidize a different segment of the economy. The segment of the economy that is “stolen from” consists of pension plans, and people who would otherwise be saving their money, perhaps for retirement, and would benefit from interest income. Part of the reason that pension plans are having so much difficulty with funding now is because of artificially low interest rates. Pensions plans will need to be bailed out, or contributions will need to be much higher, if the system continues with artificially low interest rates.

Another even more major problem is that without a return to growth, there is no nice way to end the low interest rate/Quantitative Easing policy. One possibility is that at some point, the dollar will drop relative to other currencies, and the price of imported oil will become even higher. This will make the situation worse.

Somehow the situation must be resolved. One possibility is that the government will greatly reduce benefits and raise taxes, so as to balance its budget. Alternatively, there could be a major governmental change, perhaps leading to a totally new governmental structure and different currencies. It is possible that there will be hyperinflation, or some type of break in international trade. Countries may trade more with trusted partners, or may require collateral for trade.

Impact of High-Priced Fuel Syndrome on Exporters

This post has mostly been about the impact of High-Price Fuel Syndrome on energy importers, such as the United States, Europe, and Japan. The situation isn’t quite as bad for energy exporters, but they are not completely spared.

Energy exporters are usually in a better position financially than importers, because they collect funds from the oil or other type of high priced energy they sell. These funds can be used to fund government programs. If the energy exporter is fortunate to still have some “cheap to extract” oil left, the energy exporter can perhaps subsidize oil prices for its own people. This approach works much better when population is relatively small, such as Saudi Arabia, than when population is large, such as Russia, because with subsidy, internal use tends to rise, and exports decline.

Even when a country is an energy exporter, high oil prices or other high energy prices can be a problem. One issue is that those who benefit from high oil prices (oil companies, oil workers, local economies, governments that tax oil production) are not the same as the economy in general. For example, if oil prices are high, the major producing areas, such as Alberta, Canada can benefit, even as the rest of Canada behaves much like an oil importer, with job losses.

Another issue is the one illustrated in Figure 3, that of food prices tending to rise as oil prices rise. The Middle East is an oil exporter, but a food importer. If food prices rise at the same time as oil prices, the government finds it necessary to cushion this cost increase for the poor. To do this, they must raise food subsidies, or increase the level of payments to those who are unemployed. Making these changes quickly is not necessarily easy. There is considerable evidence that the 2011 “Arab Spring” uprisings were related to high food prices (Lagi, 2011).

So even for oil exporters, high oil prices may lead to problems.

In Summary

In summary, we are running short of cheap energy, especially cheap oil. High priced oil (or high priced energy of any type) tends to slow down the economy, leading to economic contraction. Our financial system is not made for contraction. Ben Bernanke and others have used artificially low interest rates and Quantitative Easing to try to cover up our current problems, but this is not a long-term solution. At some point, the underlying problems will become evident, and some type of discontinuity will take place. The economic situation will change from one of growth to decline.

Our system of benefits and taxes to pay for those benefits is based on the cost structure that was possible with cheap energy, and the growth that was possible with cheap energy. Very major changes will be needed, if government outgo is to made to match income. Basic programs such as unemployment, Medicare, and Social Security will either have to be reduced, or taxes raised substantially. Maintenance of huge amounts of infrastructure (such as roads, water and sewer pipelines, electricity transmission lines, and schools) can be expected to be increasingly expensive as well.

It is not clear exactly how the current situation will play out, but a return to cheap energy and robust economic growth seems very unlikely. A more likely outcome is a serious discontinuity, with affected countries much poorer afterward.

References:

Bernanke, B. S., The Subprime Mortgage Market, Speech at the Federal Reserve Bank of Chicago’s 43rd Annual Conference on Bank Structure and Competition, May 17, 2007. Available at https://www.federalreserve.gov/newsevents/speech/bernanke20070517a.htm

Hamilton JH. Causes and consequences of the oil shock of 2007-08. Brook-

ings Papers on Economic Activity:215e61. Accessible at https://www.brookings.edu/~/media/Files/Programs/ES/BPEA/2009_spring_bpe... Spring 2009.

Lagi M., Bertrand, K., and Bar-Yam, Y. The Food Crises and Political Instability in North Africa and the Middle East, Complex Systems Institute, 2012 Available at https://arxiv.org/pdf/1108.2455v1.pdf

Ludlum, S. Further Evidence of the Influence of Energy on the US Economy – Part 2, The Oil Drum, April 23, 2009. Available at https://www.theoildrum.com/node/5326

Tverberg, G. Oil Supply Limits and the Continuing Financial Crisis, Energy, 2012, 37 (27-34).

Voss S. and Patel, T. Total, Shell Executives Say ‘Easy Oil’ Is Gone (Update 1), Bloomberg, April 5, 2007 Available at https://www.bloomberg.com/apps/news?pid=newsarchive&sid=aH57.uZe.sAI

Source: Our Finite World