With interest rates having been at or near zero for close to three years, a deeper look at what historically drives interest rates is in order. Specifically, it invites the questions: Historically how are interest rates determined and what should bond yields [long term interest rates] really be?

Historically, it is said that the Federal Reserve has the power to “mandate” or set short term interest rates through their influence over the trend setting Fed Funds [sometime referred to as the Over-night or Inter-bank] Rate. At the same time it is widely accepted that longer term rates are set “in the bond market” by a group of professionals known as bond vigilantes.

From Wikipedia,

A bond vigilante is a bond market investor who protests monetary or fiscal policies they consider inflationary by selling bonds, thus increasing yields.

In the bond market, prices move inversely to yields. When investors perceive that inflation risk is rising they demand higher yields to compensate for the added risk. As a result, bond prices fall and yields rise, which increases the net cost of borrowing. The term references the ability of the bond market to serve as a restraint on the government's ability to over-spend and over-borrow.

As we can see from the definition above, inflation is the prime determinant in driving bond prices.

Or is it?

Alternate Measures for Determining Inflation

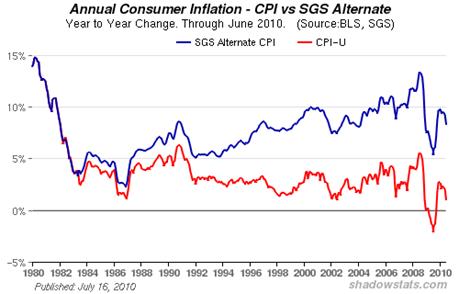

Anyone reading in this space should be more than aware of the work of John Williams of Shadowstats.com. Williams’ work has shown how officialdom has redefined the manner in which inflation is measured over the past 25 or so years:

The important thing to take away from the chart above is to remember–“if inflation were measured today, the same way it was back in 1986, today’s CPI rate would be roughly 8% instead of the RUSE–or roughly 1.5% CPI reported today by the Bureau of Labor Statistics”.

Traditionally, bond rates are determined by adding a “spread” or premium to the the inflation rate to give what is known as a “real return”–or compensation to the saver for foregoing consumption today to lend to someone who wants to consume today but does not have the capital. The premium over the inflation rate provides the saver with a return or consideration in addition to accepting repayment in debased [inflated] currency. Historically the spread over inflation for benchmark, risk-free money [like the 10 year U.S. Government Bond] is about 250 basis points.

So, if we assume that bond vigilantes are smart enough to spot this ruse, one could argue that 10 year U.S. Government bond rates should be 10.5% right now.

So What Happened?

What happened, ladies and gentlemen, is that an interest rate derivatives edifice was created that had stealth bond demand built into it.

How We Know This Is Indeed True

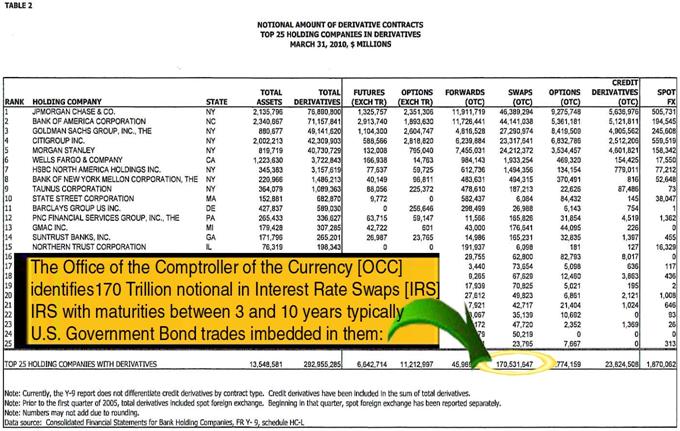

The explosion in growth in interest rate derivatives created so much stealth demand for U.S. Government Bonds, that despite record issuance, trades are customarily difficult to settle due to INADEQUATE SUPPLY:

Treasury Nominee Failed to Halt Bond Scam

...“The economist who has done the key work on this issue is Dr. Susanne Trimbath, who heads STP Advisory Services in Omaha, Nebraska. She previously worked for the Depository Trust Co, a subsidiary of Depository Trust and Clearing Corp, the U.S. clearing house for stocks and bonds.

Dr. Trimbath said, "In fall of 2008, about two trillion dollars in Treasury bonds were sold but undelivered for six weeks, more than 20 percent of the daily trading volume, up from 8.6 percent in the first five months of 2008." It was a spike from 1.2 percent in the first five months of 2007.

"There was excess demand for the Treasuries," she said. "Rather than allow this to push the price up, the Federal Reserve Bank of New York and the DTCC allowed failures to deliver to depress the price." This affects the value of bonds held by individuals, funds and major investors such as China.

The latest figures on failures to deliver are 600-800 billion dollars. Dr. Trimbath said, "The numbers look better now because the Fed threw two trillion at the market, which was used to cover these fails."…

What this all means folks is that the much ballyhooed “flight to quality” and rush to buy U.S. Government bonds is really an elaborate hoax–ENGINEERED in the bowels of the Federal Reserve and executed on the trading desks of their proxies; the likes of Goldman Sachs, J.P. Morgan, B of A, Citibank and Morgan Stanley by creating ARTIFICIAL SCARCITY for U.S. Government debt.

So, if any of you are left wondering where the bond vigilantes have gone:

They have all lost their jobs. Long ago, the last of the true bond vigilantes sold bonds YEARS AGO–intuitively correct I would argue–not realizing that Goldman’s, J.P. Morgan’s et al Interest Rate Swap Books were “black holes” of stealth artificial demand. They lost their shirts along with their jobs.

Nowadays bond traders who have chosen to remain employed resemble lap-dogs and play the game the way their masters intend them to.

Today’s Market

Overseas equity markets began the week on positive note with Japan’s Nikkei Index adding 33 points to 9,570. North American markets followed suit with the DOW ahead 208.4 to 10,674.4, the NASDAQ up 40.66 to 2,295.36 and S & P gained 24.25 to finish the day at 1,125.85. NYMEX crude oil futures added 2.51 to end the day at 81.46 per barrel.

On foreign exchange markets the U.S. Dollar Index fell .68 to 80.91.

Benchmark interest rates had the 5 yr. Government bond last seen at 1.64% while the 10 yr. bond was last at 2.96.

Precious metals ended the day mixed with COMEX gold futures adding .60 to 1,183 per ounce while COMEX silver futures gained .39 to 18.41 per ounce. The XAU Index added .55 to 170.27 while the HUI Index was off by 2.61 to 440.03.

On tap for tomorrow, at 8:30 a.m. June Personal Income data is due–expected +.1% vs. prior +.4%. Also at 8:30 a.m. June Personal spending data is due–expected -.1% vs. prior +.2%. Also at 8:30 a.m., June Personal Consumption Expenditure Core Price data is due–expected +.1% vs. prior +.2%. At 10:00 a.m. June Factory Orders data is due–expected -1.0% vs. prior -1.4%. Also at 10:00 a.m. June Pending Home Sales data is due–expected -5.0% vs. prior -.30.0 %. Then at 2:00 p.m. July Auto sales data is due–expected 4.0M vs. prior 3.7M and July Truck sales data is also due–expected 5.0M vs. prior 4.8M.

Wishing you all a pleasant evening.