- The 18-nation euro-zone is the largest economy in the world, eclipsing that of the U.S.

- The euro-zone is the largest trading partner of the U.S. (the largest importer of U.S. goods, the largest exporter of goods to the U.S.).

- The euro-zone is in an economic crisis.

Its recovery from the 2008 global financial collapse has been as anemic as that of the U.S., in fact more so. The euro-zone already slid back into recession once. And its economy was barely positive in the first quarter of this year, growing only 0.2%. It slowed further to 0.0% quarter-over-quarter in the second quarter.

Worse, Germany, the euro-zone’s largest and previously strongest economy, unexpectedly saw its economy contract to negative -0.2% in the second quarter. France, the second largest euro-zone economy, saw its growth slow to 0.0% for the quarter. Italy, Europe’s fourth largest economy, slid back into recession, its GDP at negative 0.8% in the second quarter, its second straight quarterly contraction.

Reports this week indicate the problems are worsening in the third quarter.

Retail sales in Germany plunged 1.4% in July, after declining 0.4% in the second quarter.

Germany’s Ifo business confidence index fell in August for the fourth straight month, to its lowest level since July 2013. Market research group GfK reported its German consumer expectations index “collapsed” in August to its most pessimistic level since 1980. Perhaps for good reason, since the overall euro-zone’s unemployment rate remained in double-digits at 11.5% in July, just 0.5% lower than its peak of 12% in 2013.

Meanwhile, European central banks, which have been hoping to see signs of rising inflation to give their economies a lift, were hit instead with deflationary indications. Overall euro-zone inflation fell to an annualized rate of just 0.3% in August, a five-year low.

[Read: Central Banks Buying Stocks - The Beginning of a Major Trend?]

In the U.S., consumers did not seem to get the message that they need to buy more, to pick up the slack of slowing U.S. exports to the eurozone. Friday’s report was that U.S. consumer spending, which had been at least somewhat positive this year, declined 0.2% in July, negative for the first time in six months.

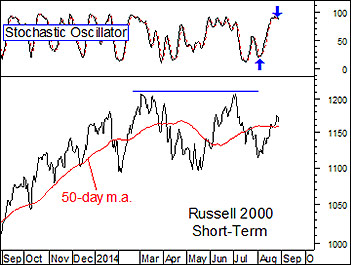

European stock markets have reacted negatively to the situation, topping out in June into corrections. They became short-term oversold beneath their 50-day moving averages, and rallied off that oversold condition in August. But those rallies have not been impressive so far, having only recovered 50% of their decline, and already potentially running out of steam at a lower high.

U.S. markets recovered more impressively off their short-term oversold conditions, the DJIA back at its previous peak, the S&P 500 at a fractional new high.

But is the U.S. market beginning to feel the pinch of the euro-zone’s crisis, and also running out of steam?

It wouldn’t be too surprising given the other conditions usually seen at market tops; high valuation levels, high level of bullish investor sentiment and participation, heavy insider selling, and so on.

It has also been more than three years since the market experienced even a normal 10% to 15% correction, while on average it does so every 12 months. And of the 25 bull markets of the last 100 years, this is the fourth longest running since 1929.

You do have to at least ask yourself if that is justified, especially given the still anemic economic recovery. The market is higher than in 2000 and 2007. Even in those years of booming economic conditions, the market was not able to drive even higher, the S&P 500 instead losing 50% of its value in those apparently forgotten bear markets.

I know, it’s all about the Fed’s easy money policies and near-zero interest rates. But still, at those market tops, and indeed all market tops, there were also reasonable explanations of why ‘this time is different’.