At present, we have a Dow theory non-confirmation in place that began in mid-January. According to Dow theory, we must operate under the assumption that the previously established trend is still intact until it is reversed with a move above or below the previous secondary high or low point. In this case, a downside trend reversal would require a move below the previous secondary low point. Until such time, the primary trend change that occurred in conjunction with the March 2009 low still remains intact. Now, as for non-confirmations, they serve as warnings of a possible trend change. Non-confirmations do not mean that a trend change is inevitable, because it is possible that the non-confirmation can be corrected. It is also possible that the previous secondary high or low point will not be penetrated. The current non-confirmation can be seen on the chart below. If this non-confirmation is not corrected then I know from my trend quantification work that there are statistical guides that can be used to help us gauge the meaning of this non-confirmation as well as the expected outcome. I will cover that all in the research letters and updates if it continues to develop. For now, this is a warning that must simply be watched and measured against the statistical and other implications. Don’t confuse non-confirmations to automatically be a “sell signal” because in accordance with Dow theory, that is a misconception. There is much more to the story that just a non-confirmation. Rather, it is a process in which statistical and other structural evidence must be understood, weighed and considered.

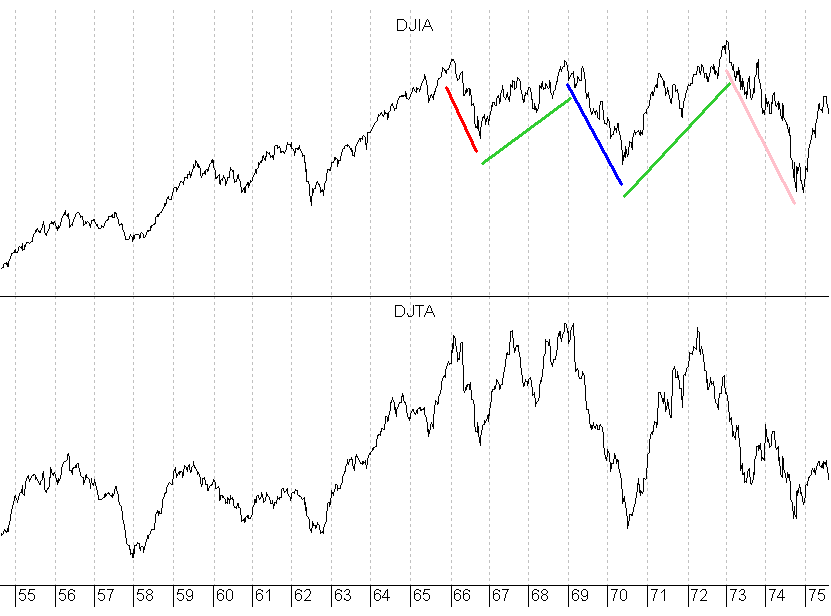

In the last post here on January 14th I talked about bull and bear market relationships. In that post I explained some of the big picture reasons that the rally out of the March 2009 low must still be viewed as a longer-term bear market rally. One of the items that I did not cover there was value. Value is another historical marker of secular bear markets. Historically, the dividend yield will be roughly equal to the price earnings ratio at secular bear market bottoms. I have used the S&P data here because I did not have this data as far back on the Industrials. At the 1932 bear market bottom the yield was 10.50% and the P/E was just under 10. At the 1942 bear market bottom the yield was 8.71% and the P/E was 7.3. At the next great bear market bottom in 1974 the yield was 5.9% and with a P/E of 7.24. If we take this same reading at the 1982 low the yield was 6.2% and the P/E was 6.9. For the record, these P/E ratios are based on Generally Accepted Accounting Principles and not the bogus George Orwellian methods of today. At the 2009 low, the P/E was 26 with a dividend yield of 3.2, which is hardly at par. Therefore, based on this historical measure, there is also no indication that the 2009 low marked the bear market bottom. It is for this reason along with the historical bull and bear market relationship issues covered in the last post here that I continue to believe the rally out of the March 2009 low is a longer-term bear market rally much like was seen between 1966 and 1974. I have also included a chart of that period below.

I told my subscribers before the anticipated rally out of the 2009 low even began that it would be a rally of a higher degree and that the longer it lasted the more dangerous it would become. What I meant was, the longer this rally lasts, the more convinced people will become that the bear market bottom has been seen. In looking at this chart of the 1966 to 1974 period above, don’t you think that it would have been pretty convincing that the worst was over as the market moved up during the 26 month rally into the 1968 high? As is the case now, it was the Dow theory phasing, bull and bear market relationships and values that warned of the pending phase II decline that finally did follow and that carried the market down to another new bear market low. But, then came the rally separating phase II from phase III. In this case it was a 32 month rally. Stop and think about it. After another leg down into the 1970 low don’t you think it would have been an even harder sell to convince people that the low had not been seen? Yet, Dow theory phasing, bull and bear market relationships and values warned that the bottom had not been seen and once again they proved correct. In January 1973 the Industrials turned back down and plunged to yet another new bear market low in December of 1974. It was then, only weeks after that low was made, that Richard Russell was able to identify the bear market bottom and he did so because he understood Dow theory. Based on the bull and bear market relationships, we should be operating within a little larger version of the 1966 to 1974 bear market period. I realize that this is probably a hard concept for most to understand. But, if we stand back and look at the historical relationships we see that this bear market has likely not run its course. I have found specific DNA Markers that have occurred at all major tops since 1896 and it is these markers that can be used to identify the top of this counter-trend bear market advance. I sincerely hope that people are listening and that they understand the context in which this rally is unfolding.