Fundamental analysis of "buy and hold" companies is a quaint, Warren Buffetish notion that probably works in the long term. But as Keynes said, in the long term we're all dead. The big risk in today's über-correlated markets is systemic shock. One can practice due diligence on a company and buy at a reasonable valuation, but if global markets collapse the next day and don't recover for years, one has paid a lot in opportunity cost. In other words, tail risk is not reflected in fundamental analysis.

Fundamental analysis is valuable so long as the basic fabric of capital markets remains intact. In an insane world (where U.S. Treasuries and German Bunds are considered "risk-free", of infinite rehypothecation, where MF Global's John Corzine walks off with 0M segregated assets, of the London Whale, LIBOR, Goldman's muppets, regulatory capture of SEC and Fed, U.S. / China animosity and the dollar's loss of world reserve status) it's unlikely that business-as-usual will continue without a disruptive bout of creative destruction.

Precisely when and how it will occur is anyone's guess, but, unfortunately, old school techniques like cross-asset class and regional diversification have lost their glimmer. Just as socioeconomic disparity is partitioning the globe into lords and serfs, so too has the market been divided into polarized castes of highly correlated risk-on assets and (scarce few) risk-off havens.

Risk on-assets include equities, commodities, Emerging Market/commodity currencies, and high-yield credit. Risk-off is limited to the USD, JPY, "safe" sovereigns and gold.

The Correlation Bubble

Regional and sectoral equity correlations are on the rise.

Emerging Market / Developed Market equities are increasingly correlated, as are various asset classes.

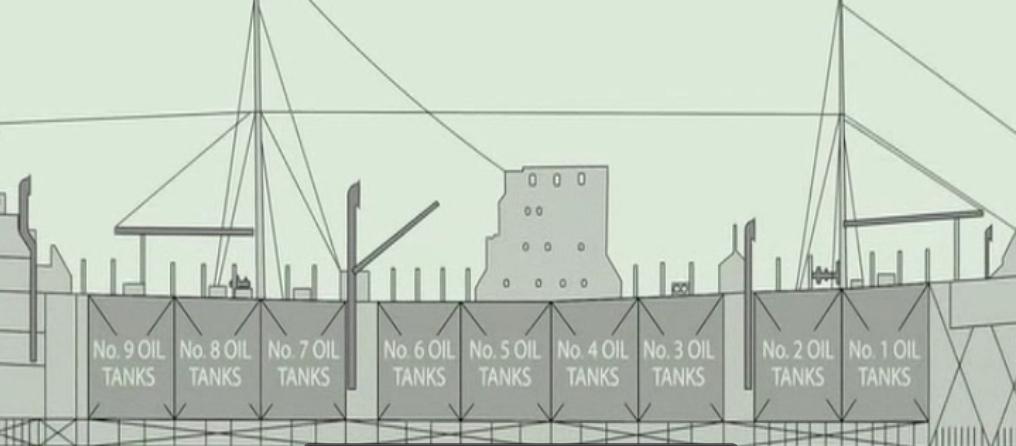

There is a useful analogy that describes the de-compartmentalization of risk:

Oil tankers used to have one, big compartment in their hull. In choppy waters, that oil would slosh back and forth, the momentum of which threatening to capsize the vessel.

A new method was adopted: separate the oil into smaller compartments, which would diminish the momentum of the swaying liquid and increase stability.

Image courtesy of Inside Job (A highly recommended film, the original analogy was about Glass-Steagall and Gramm-Leach-Bliley Act.)

Global markets used to be divided, where risks in one part of the world would not affect others.

Today, valuations are driven by monetary policy expectations; globalization of supply chains, capital and labor flows; ETFs and trading techniques (algorithmic) that bundle "risk assets" into a homogeneous category regardless of fundamentals.

The difficulty for long-term investors is diversification. Short-term traders act like lemmings, pilling into one asset and then another, rocking the boat with ever greater force - destabilizing the entire craft.

There is so much money sloshing around and few places to hide. Markets today are a game of musical chairs played by sumo-wrestlers; when the music stops, we've got a lot of mass looking for a place to sit and the chair is already fragile (negative real bond yields = bubble).

Causes of Rising Correlation

From a report by JP Morgan's Global Equity Derivatives crew:

While the increase of correlations over the past three years is largely driven by macro volatility, secular market changes are causing a rising trend in cross-asset correlations. These changes include the integration of global economies and capital markets, and innovations in the financial industry. Advancement of risk-management techniques, such as hedging and dynamic asset allocation, use of US Treasuries as 'risk-free' storage, as well as more intensive extraction of alpha, have likely contributed to a secular increase in cross-asset correlations.

JP Morgue doesn't mention its patron saints Ben Bernanke and Mario Draghi, who have been busy marrying all price action to the prospects of more cash injection (which will be more than enough to paper over the trillions of dollars of upcoming sovereign debt with no recourse to currency devaluation).

And by financial innovation JPM means high-frequency trading algorithms that trade headlines, with buy commands like "QE" + "Draghi" + "Print" + "Bernanke" + "Dovish" + "Low Inflation Expectations" + "- Stands Ready" + "- Contained" + "Balance Sheet Expansion.

Sell commands likely contain the terms: "Angela Merkel" + "Bank Failure" + "Capital Flight" + "Inflation Concern" + "Moral Hazard" + "Insolvency" + "Austrian" + "Unconstitutional" + "Diminishing Returns" + "Downgrade."

High-frequency trading algorithms are designed to sniff out stop losses, trade momentum, and steal pennies from other traders (under the guise of market-making, when in reality the algos are turned off when they're most needed, like during the May 6 flash crash).

More on how HFT is homogenizing the markets:

Cross-asset statistical arbitrage involves simultaneous trading of currencies, equities, and commodities. A computer model establishes and forecasts covariance between these assets, then algorithmically trades based on discrepancies between the expected relative moves of assets and observed moves. This type of statistical trading can provide liquidity and sap the market impact from trades in each asset class. However, the result is an increase of cross-asset correlation.

Example of HFT increasing short-term correlations:

The politically connected bank insiders and politicians get the first whiff of major policy changes and announcements. This puts mom-and-pop traders and retail investors at a serious disadvantage.

Fundamental analysis was the last stronghold of retail, but the animal spirits have been replaced with central bank-watching. Assets that should be sold to value investors and vultures at a deep discount are riding high (MBS, CDS, Eurobank equities) on the prospect that some sycophantic central banker will hook up Blankfein, Dimon, and Moynihan with 100 cents on the dollar (courtesy of Euro/Dollar savers).

JPM goes on:

This [correlation] trend has been caused by the globalization of economies and financial markets. We believe this globalization, and hence the high cross-regional correlation trend, is not reversible. While region-specific events such as the recent earthquake in Japan may soften cross-regional correlations, markets are not likely to revert to the levels observed in the mid-1990s, when the average correlation between EM benchmarks was close to zero and EM/DM correlation was only ~25%.

This trend of rising cross-regional correlation significantly diminished the once important diversification benefit of investing across emerging and developed markets. It appears that in the case of cross- regional investing, 'the only free lunch in finance' (a common reference to diversification) has been eaten.

The recent increase of equity correlation has largely been driven by the increased macro volatility since 2007. However, other structural reasons contributed to increased levels of equity correlation. The widespread use of index products (e.g., futures) and high-frequency trading strategies, such as statistical arbitrage and index arbitrage, are likely contributing to increased levels of correlation.

While the levels of correlation should decrease with reduced macro volatility, the new normal for equity correlation will likely be higher due to the aforementioned structural developments. The historical average level of correlation was 28%, and our estimate for the future long-term average is ~35% (significantly lower than correlation during the peak of market crisis, but higher than the historical average).

Welcome to the New Normal.

The Great Divergence

The markets today are defined by a see-saw between risk assets and Treasuries. When treasuries are no longer recognized as safe and this yin-yang relationship ends, there will be trouble.

More from the Morgue:

[T]he occurrence of Stagflation or even full-fledged US bond/equity contagion could reverse the equity/rate correlation.

In the case of Stagflation, treasury yields are expected to increase as a result of increased inflation expectations. A low or negative growth outlook and increased inflation expectations could cause an equity selloff. In this way, the occurrence of Stagflation could cause equity/rate correlations to drop or even turn negative.

The most dramatic reversal of equity/rate correlations could happen in the event of full-fledged US bond/equity contagion. This could occur as a result of a US fiscal crisis, prompting foreign investors to abandon US Treasuries as the 'risk-free' asset of choice.

A sharp increase in rates would be followed by a broad selloff of all dollar assets. This type of tail event could result in equity/rate correlation dropping towards -100%. In addition, this event would likely trigger a dramatic reversal of equity/currency and equity/commodity correlations, likely weakening cross-regional equity correlations (e.g., US equities underperforming).

This is not a tail risk. This is the likeliest outcome. Right now, everyone sees treasuries as "riskless." But this financial repression cannot go on forever, and U.S. trading partners (BRICS) don't like seeing their treasury holdings eroded.

The Fed is in trouble; Treasury rates can't rise or else banks will be rendered insolvent, U.S. growth will decline, and the U.S. government will be unable to finance its debt. Not to mention that a decline in the principal of .1T Chinese treasury holdings would add insult to injury and would drive the PBoC to dump faster.

Endgame

The days of dollar dominance are waning, and the rest of the world stands to benefit.

Timothy Mitchell wrote about the petrodollar global taxation system in Carbon Democracy:

Europe and other regions had to accumulate dollars, hold them, and then return them to the U.S. in payment for oil. Inflation in the U.S. slowly eroded the value of the dollar, so that when these countries purchased U.S. oil, the dollars they used were worth less than their value when they acquired them.

These seigniorage privileges enabled Washington to extract a tax from every other country in the world, keeping its economy prosperous and thus its democracy popular.

Investors might hope for a slow, orderly, cordial transition away from the dollar (into renminbi, gold, SDRs, or some combination) -- but given the belligerence of U.S. rulers toward rival powers (China, Russia, Iran, Brazil, India) such an outcome is unlikely.

To hedge the de-coupling of equities from treasury rates, the guys and gals at JPM suggest a hybrid put strategy betting against the S&P with a profit contingency of higher treasury rates (which is cheaper than a simple equity put because equities and treasury rates are still highly correlated).

Investors wary of a potential U.S. fiscal crisis and the tail-risk scenario described above could use an equity/rate correlation view in order to inexpensively hedge their equity exposure. An example trade would be to buy an out-of-the-money put option on the S&P 500 index, with a payoff that is contingent on treasury yields rising above a certain level.

Given the current positive correlation between rates and equities, the cost of this type of hybrid would be significantly cheaper (as compared to the simple S&P 500 put option). For more details on this trade, see the last section of this report (Hybrid Derivative Trades).

Not everyone can use this strategy, it would become too crowded (nor should they, because counter-party risk in a liquidity crunch renders it akin to picking up dimes in front of a steamroller). When the SHTF, you want to be in liquid assets, the ownership of which you can document (or better yet, tangible assets that have zero counter-party risk). The JPM report goes on:

Compared to 20 years ago, markets are currently more correlated and there is more pronounced "Alpha/Beta" separation. General market risk or 'beta' is managed more efficiently and at significantly lower cost (e.g., liquid derivative instruments and electronic trading), while large pools of assets are seeking 'alpha' via relative-value and arbitrage trading necessary for the proper functioning of capital markets.

JP Morgue is a bit sanguine about the prospect of using derivatives to stabilize a global debt overhang that is itself due to misuse of derivatives. Everyone is feeding at the same Central Bank liquidity trough, and if that golden goose dies, can JP Morgan count on Goldman to make good on its obligations? Or will we see (another) default cascade and Minsky Moment? Then it's ECB and Fed to the rescue, devaluation and a double serving of moral hazard.

Breakdown of the shadow banking system:

"Insanity: doing the same thing over and over and expecting different results."

- Albert Einstein

Source: Seeking Alpha