Originally posted at Briefing.com

Have you checked the forecast lately? It calls for a continuation of gray skies and cool temperatures across the country. What a bummer... and what a misdirection.

We're not alluding to the weather forecast. Rather, we are alluding to the first quarter real GDP growth forecast, which unfortunately at this juncture calls for little growth.

There are various firms employing their own GDP growth models, but for our purposes here, we are talking about the Atlanta Fed's GDPNow model.

It's a model anyone can access and it's a model that has seen its fair share of downward revisions since the initial "nowcast" was provided on January 30. It is also a model that could be shedding some light on the vicissitudes of the stock market.

Hard-Boiled Data

What readers need to be aware of is that the GDPNow model is driven predominately by "hard" data, which is quantifiable and a product of the actual economic activity, versus "soft data," which is qualitative in nature and driven by opinions.

For example, the advance report on durable manufacturing orders is "hard" data, whereas the ISM Manufacturing report is "soft" data.

The former is tabulated based on actual statistics reported by approximately 3,000 manufacturing companies covering 92 industry categories. The latter is tabulated based on respondents' view of whether activity for various fields is increasing, decreasing, or unchanged. One such field is customers' inventories, where respondents are asked to estimate what their customers' inventory levels are.

To be clear, soft data can still provide some very useful information, which is why the ISM Manufacturing Survey has been around since 1931. It is also why the GDPNow model incorporates the ISM Manufacturing and ISM Non-Manufacturing data into its forecast. Those are the only two pieces of "soft" data, however, that are part of the GDPNow tracking model.

The rest of the tracking model is driven by "hard" data and the hard truth for some right now is that the "hard" data just aren't confirming the upbeat economic view of matters showing up in the "soft" data.

The main point of order in that respect is the understanding that the GDPNow model forecast for real GDP growth in the first quarter is a lowly 0.9% (seasonally adjusted annual rate).

The initial "nowcast" was 2.3% on January 30. That forecast popped as high as 3.4% on February 1 following the ISM Manufacturing and Construction Spending reports, but it has been pretty much downhill ever since.

Getting Disconnected

A 0.9% growth rate would tie the fourth quarter of 2015 as the weakest growth rate since the 1.2% decline registered in the first quarter of 2014.

That 1.2% decline followed a strong 4.0% growth rate in the fourth quarter of 2013 and it was consistent with the finding that first quarter economic activity often slows from the fourth quarter.

The 0.9% growth rate projected for the first quarter of 2017, then, would fit the aforementioned pattern based on the understanding that the second estimate for fourth-quarter GDP in 2016 is 1.9%.

A slowdown in consumer spending, a decline in government spending, a bigger drag from net exports, and a smaller change in private inventories have driven the downward revision for the first quarter forecast. Things would have been even weaker if not for the increase in business investment.

The next update to the GDPNow tracking model will take place on March 24 following the release of the Durable Goods Orders Report for February. It's possible the GDPNow model forecast for first quarter GDP will have a one-handle on it after that release and it's also possible that it could move closer to zero.

In either case, there is no mistaking the fact that there is a real disconnect right now between the hard data and the soft data, and what remains to be seen is whether high levels of confidence pull the economy up or weak economic activity ultimately pulls confidence levels down.

Noise

In her recent press conference to discuss the Federal Reserve's decision to raise the target range for the fed funds rate, Fed Chair Yellen was asked to explain why the Federal Reserve did so when GDP growth continues to be weak. She defended the move by explaining that relevant data on employment and inflation show things tracking toward the Federal Reserve's policy objectives.

It was a defensible position with the unemployment rate at 4.7% and the PCE Price Index up 1.9% year-over-year. The Federal Reserve's median longer-run projections for those variables are 4.7% and 2.0%, respectively.

Ms. Yellen went on to add in a rather stark admission that GDP is a "pretty noisy indicator." She clarified her remark with the observation that, if one averages GDP over several quarters, it would show an economy growing around 2.0% per year and that such a growth rate is consistent with the Federal Reserve's growth projections for the next several years.

Such growth doesn't warrant a fed funds rate as close to the zero bound as the fed funds rate has been. At the same time, though, it isn't such robust growth to warrant rapid and repeated tightening, which is why Ms. Yellen also highlighted the Federal Reserve's standing belief that the path to normalization is likely to be a gradual one.

First quarter GDP growth isn't going to alter that perspective.

Another Gradual Path

If anything, the lowly first quarter GDP growth rate could serve as a sobering reminder that the stock market has gotten ahead of itself with its growth expectations.

That might not mean much admittedly if the health care reform plan passes and the market takes the high road of believing the passage of tax reform is around the corner. Still, it is hard not to notice that the stock market already seems to be dialing back its growth expectations.

At the least, the squabbling among Congressional GOP members over the House GOP's health care reform plan has prompted some market participants to consider the notion that the path to a sustained 3%+ GDP growth rate is going to be a gradual one as well, assuming that path can ever be found again.

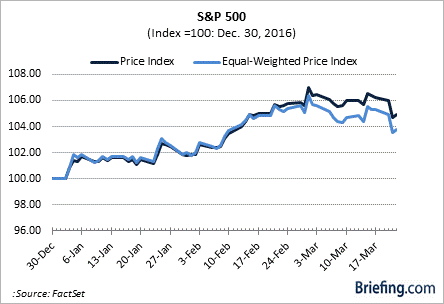

It might be hard to notice that looking at the standing of the S&P 500 alone. It's up 5.3% year-to-date, having been helped in no small part by a 22% gain in Apple (AAPL). The S&P 500 Equal Weighted Price Index, though, is up 3.8% year-to-date.

Given the run the market made following the election, few people would be disappointed with the additional gains seen so far this year, whether they are market-cap weighted or equal weighted.

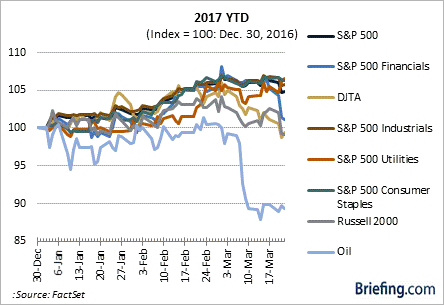

The market's bullish engine is clearly still running, yet there have been some interesting developments under the hood leading some to think the market, and its affinity for the pro-growth narrative, could be poised for a pit stop.

- The financial sector has underperformed with a 1.7% year-to-date gain

- The Dow Jones Transportation Average has underperformed with a decline of 0.8%

- The industrials sector is trailing the market with a 3.6% year-to-date gain

- The countercyclical utilities and consumer staples sectors are both outperforming the market with year-to-date gains of 6.3% and 6.2%, respectively

- The Russell 2000 has underperformed with a year-to-date gain of 0.2%

- Oil prices have declined 11.1% year-to-date and have weighed heavily on the energy sector, which is down 8.7% year-to-date; and

- The yield curve has flattened, with the 2-10 spread narrowing to 116 basis points from 124 basis points at the start of the year

What It All Means

One has to allow for the possibility that market participants are electing to take some money off the table following such a huge run since the election, which has stretched valuations for many stocks and/or sectors.

That is, the underperformance of the stock-related areas noted above could simply be due to profit taking and may not be tied so directly to prominent growth concerns. If so, then there will be a continued willingness to buy on pullbacks.

For the time being, the eagerness to buy on pullbacks has been stifled by the uncertainty surrounding health care reform, which is feeding into concerns about the timing, and viability, of tax reform.

Alas, the stock market has entered a holding pattern of sorts waiting for the legislative process to play out, knowing that it has gotten ahead of itself with its growth expectations and knowing it could be subjected to a meaningful pullback if the legislative process doesn't unfold in the fashion the market has ideally envisioned.

The lowly first quarter GDP growth projected by the Atlanta Fed's GDPNow model forecast is based predominately on "hard" data and that forecast is reminding everyone that strong economic growth isn't in the cards yet -- even though a suit of strong growth is the hand the stock market hopes to keep playing.