The global manufacturing purchasing manager index is comfortably above the 50 threshold signaling expansion. Importantly, the upturn is fairly synchronized, with improvement visible in the US, Europe, and Asia. This corroborates the upward adjustment in global bond yields we’ve seen in recent months.

Check out Jim O’Sullivan on US Economy, Fed Rate Hikes, Market Outlook

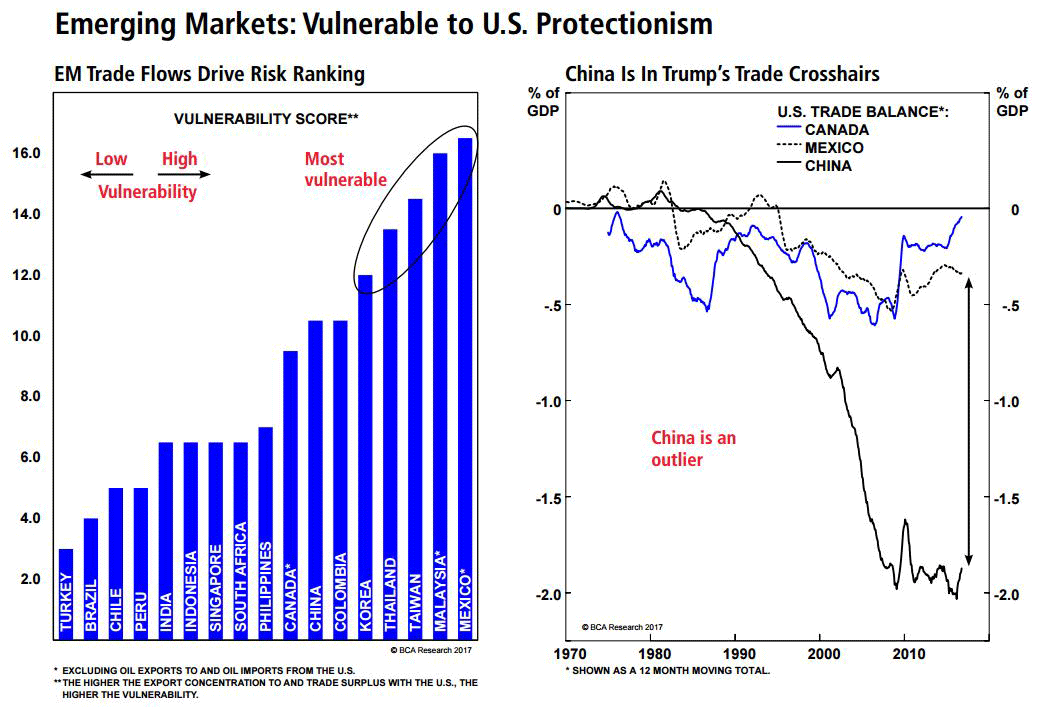

A big source of recovery in global industrial momentum in the past year has emanated from China. But growth tailwinds from real interest rate relief and fiscal expansion are set to wane in the second half of 2017, while protectionist elements of proposed US tax reform pose risks to EM growth prospects more generally. Those countries with the highest percentage of exports and trade surplus with the US as a share of GDP are most at risk of any combination of tariffs or border adjusted elements of US corporate tax reform.

Read Bianco: Trump Will Bring More Inflation Than Real Growth

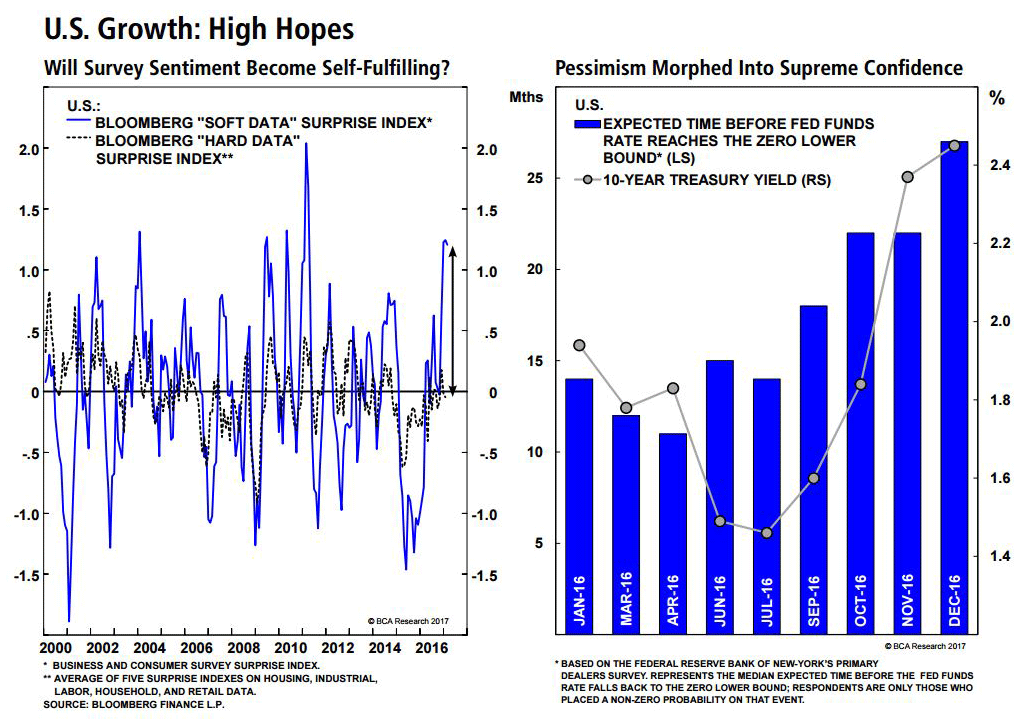

One of the primary axes of debate around the sustainability of US growth momentum revolves around how to interpret the surge in soft, survey measures of economic activity – namely consumer and business confidence – relative to expectations, running well ahead of the hard data – barometers of the health in the housing, industrial, labor, household, and retail sectors. We have some sympathy for the view that the survey data usually leads hard data, and that the pickup in confidence reflects a revival in long-dormant animal spirits which is feeding higher capacity expansion and hiring plans, particularly among small firms in the NFIB survey. But the large gap between the sentiment-oriented readings of the growth outlook and the mediocre pulse of coincident real time data underscores how great expectations for a sizeable upgrade in the plane of US economic growth are. Fears of secular stagnation have done an 180 degree turn to supreme confidence about the growth outlook in the last few months. The New York Fed’s primary dealers’ survey has extended expectations for the longevity of this business cycle, such that the median respondent now thinks the expansion will last twice as long as expected just a year ago.

We agree that US growth is likely to remain firm over the next 12 months because the economy has a lot of momentum behind it right now. But the reflationary window is likely to start to close as the economy reaches the upper limits of its potential from a supply perspective. Exuberant growth expectations and equity market momentum reflect expectations that tax and regulatory reform will reinvigorate the economy’s longer-term growth potential, via increased spending leading to higher productivity growth. We think the dysfunction in Washington portends a long, protracted debate on tax policy and infrastructure spending, such that the impact on growth is a story for 2018, not 2017. But once again, markets are forward looking. A positive shock to aggregate demand from looser fiscal policy applied to an economy already operating near capacity would translate into higher inflation rather than increased output. This dynamic would drive up real interest rates and reduce spending on rate-sensitive goods such as consumer durables, housing, and business equipment. In addition, higher interest rates will cause the dollar to strengthen, crowding out the pro-growth pulse of fiscal stimulus. Fiscal multipliers are much smaller when an economy is close to full employment.

But the global profit recovery is real, for the coming few quarters at least, supporting our cyclically bullish stance on global equities through the coming 12 months.

The dollar remains in a cyclical bull market. The recent pause in its advance has not keyed off a reversal in the 2 year real rate differential between the US and its trading partners, which continues to expand. More likely the ‘weak dollar’ rhetoric from the Trump administration, consolidation of crowded long dollar positioning, and the benign pulse of the average hourly earnings read in the latest US employment report have cooled sentiment, temporarily at least. We assign low odds to another Plaza-Accord type coordinated agreement. History suggests that currency intervention only works when it is consistent with underlying macroeconomic fundamentals. With the Fed signaling a tightening bias which America’s trading partners’ economies don’t currently justify, a globally coordinated pact to weaken the US dollar would lack market credibility. With respect to the value of the US dollar, President Trump cannot suck and whistle at the same time.

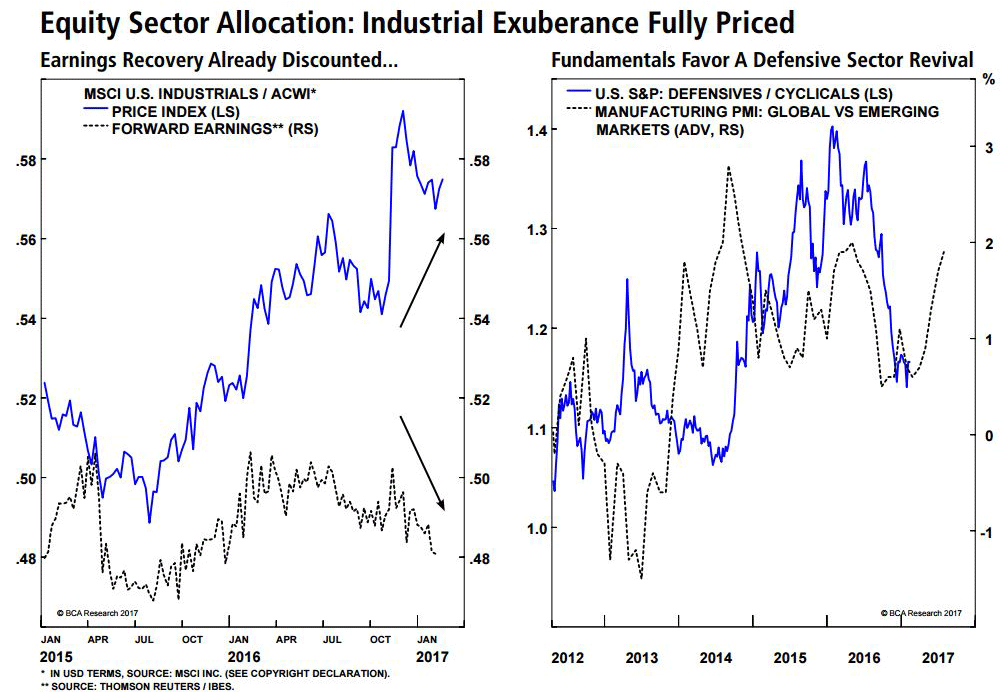

The risk-adjusted value proposition in US equities has deteriorated, but over a 12-month horizon, moderately above trend growth, benign inflation, and a still relatively accommodative Fed will prolong the cyclical equity bull market. One way to indemnify an equity portfolio against a near-term pullback would be to reduce exposure to the sectors that have overpaid for dividends from business-friendly policy changes, namely deep cyclicals, and industrials. Conversely, the outperformance of developed economy growth relative to emerging economies suggests that defensive sectors will enjoy a revival if EM growth remains relatively lackluster and the dollar remains well bid.

As for credit markets, we continue to expect the economy to track towards the Fed’s dual employment and price stability mandate over the course of 2017. There is still 30-40 bps of upside in breakeven inflation yields before that threshold is reached, leaving scope for TIPS to outperform nominal Treasuries, and the yield curve to steepen via a rise in longer-dated yields. There is no immediate urgency for the Fed to tighten in March, but we still see scope for three rate hikes in this calendar year, more than markets discount. We place high odds on the 10-year US Treasury yielding more than the current 12-month forward rate of 2.77% in a year’s time.

To find out more, click here to listen to BCA Global Strategist Caroline Miller’s February 16th Webcast.