October was a rough month for the market. As of 10/29/2018:

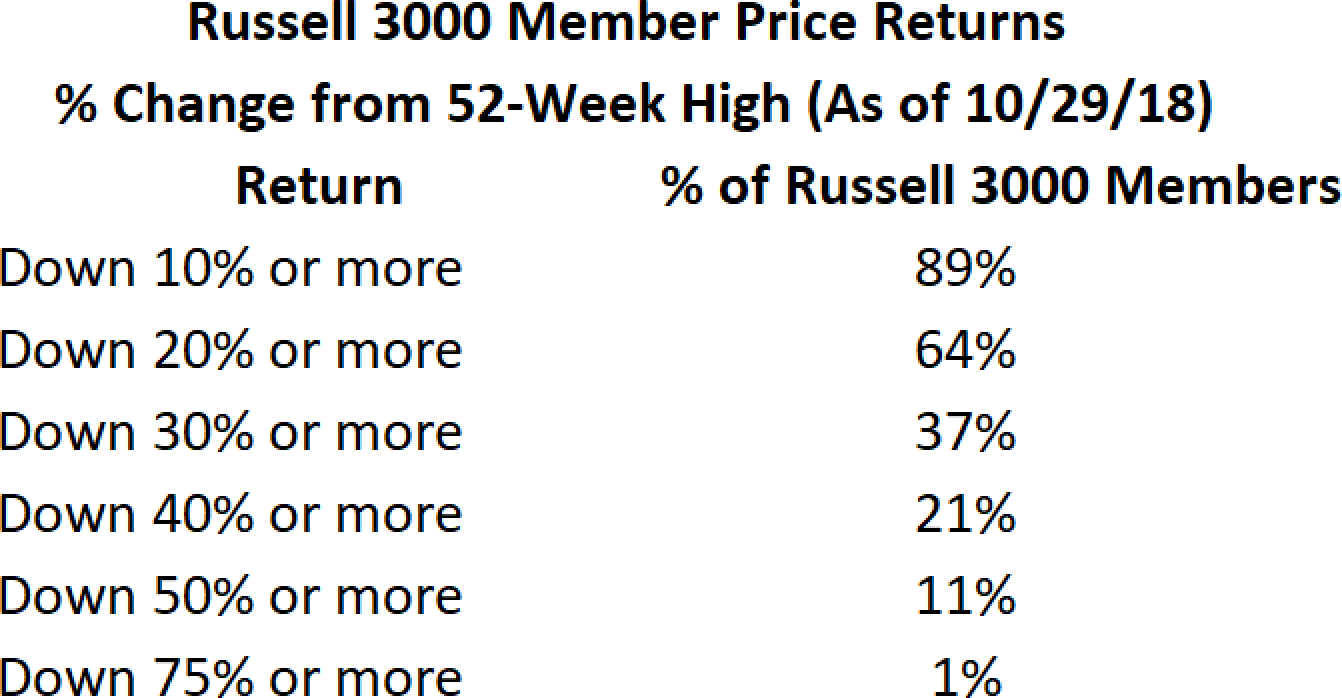

- 64 percent of the Russell 3000’s members were in bear markets (down by 20 percent or more)

- Nine out of 11 Russell 3000 sectors were in bear markets

- 20 out of 22 commodities in the Bloomberg Commodity Index were down by more than 10 percent from their 52-week highs

- 18 out of 20 global Bloomberg Barclays Fixed Income Indices were down for the year

- Global bonds lost $1.95T in value from the January 2018 highs through the end of October

- 16 out of 17 US Aggregate Bond fixed-income categories were down for the year

- 123 out of 146 world currencies were down relative to the USD

Well, that sure wasn’t fun! The S&P 500 fell 6.9 percent last month, making it the third worst month since the bull market began nearly 10 years ago. The decline was sharp and swift with some U.S. companies losing over $10B in market capitalization. The table below highlights some of the carnage that took place with a few S&P 500 members that fell 40-60 percent from their one-year highs.

When we broaden our view to look at small-cap and mid-cap companies, the declines are even more severe. The Russell 3000 adequately represents 98 percent of the entire U.S. market capitalization. When we look at the details of how extensive the decline was last month the numbers are astounding. Of the 11 market sectors, only the defensive utility and real estate sectors, on average, did not witness a bear market. That was a tough feat to accomplish when the average U.S. stock fell 27.5 percent from its highs. Sixty-four percent of U.S. stocks went through a bear market, meaning they fell by at least 20 percent, and more than 11 percent of companies lost half their market value.

To give you a sense of what a difficult year it has been to be a stock picker, look at the table below showing various major index year-to-date (YTD) returns as of Nov. 2 compared to the index’s median member’s YTD return. The greatest variation was seen in the NASDAQ which was up 6.18 percent YTD (largely due to Apple’s outsized influence) compared to its average member which was down nearly seven percent for roughly a 13 percent performance differential.

Index & Member Returns as of 11/02/2018

In a clear change from the prior sell-offs during this bull market, we haven’t seen a flight to safety where investors run to bonds (bond returns are typically positive during market routes). Instead, at the market lows on Oct. 29, only one out of 17 U.S. fixed income bond categories were up for the year. Even bonds have suffered with rising interest rates.

The following table from JP Morgan shows this year’s losses in fixed income were not isolated to U.S. bond markets—most bond markets across the globe were down as well.

In October, the U.S. stock market could no longer ignore the carnage occurring all over the world in virtually every asset class except for U.S. stocks. We believe the record amount of stock buybacks was a large reason for this. U.S. companies are expected to retire roughly one trillion in market capitalization this year, with a significant portion of this coming from repatriated cash brought back to U.S. shores from the 2018 tax cuts. Interestingly, with all the fear and anxiety regarding trade wars, the impact of rising global tariffs pales in comparison to the amount of repatriated cash as shown in the following table.

Before they announce earnings, companies are prohibited from buying back their stock until 48 hours later. According to estimates from Goldman Sachs, 86 percent of the S&P 500 companies were restricted from buying their stock by Oct. 5. Not surprisingly the S&P 500 put in a meaningful top just two days prior. However, companies will be exiting their blackout period en masse and the market could be gearing up for some welcome support.

As CNBC reported two weeks ago Companies buy up their shares, just in time for the market

It's going to be a record year for buybacks. DataTrek estimates that in the last 12 months, the companies in the S&P 500 have purchased $646 billion of their stock, 29 percent more than the previous 12 months. Most estimates believe total announced buybacks will hit $1 trillion this year.

Here's the key. A big chunk of that money has not been spent yet. One firm estimates there could be as much as $350 billion in "dry powder" from unspent buybacks available.

So the money is there, and it's pretty clear that the drop in stock prices will be very enticing for company financial chiefs.

Deutsche Bank's Parag Thatte, in a recent note to clients, noted that "As the blackout period rolls off for more companies, especially those with large buyback programs, the pace of buybacks will ramp up sharply."

Goldman Sachs agrees. It notes that November has historically been the most active month of the year for buybacks.

We believe the record buyback programs announced should lift stocks higher into the end of the year and allow the market to recoup a significant portion of its October decline. It's likely market returns will improve as we close out the year and, based on our expectations for a difficult 2019, we will be using the market rally to raise cash and position accounts defensively for 2019.

Markets Will Have to Grapple With Three Major Developments in 2019

We see three major developments that will likely weigh on financial markets heading into next year. The first is a slowing global economy. Last month we were treated to China’s third quarter GDP which came in at 6.5 percent annual growth, lower than the expected 6.6 percent rate. It was the weakest since the global financial crisis of 2009 where first quarter GDP growth rate fell to 6.4 percent. The International Monetary Fund (IMF) estimates China’s GDP growth for 2019 will be 6.2 percent, which would mark the slowest pace of growth for the Chinese economy in a quarter century. Given China is the world’s marginal growth engine, their continued slowdown will be felt throughout the globe and will weigh on global growth estimates for next year. The IMF cut its estimates for world GDP growth from 3.9 percent to 3.7 percent for this year and next. Given that roughly 40 percent of S&P 500 company revenues comes from abroad, the growth slowdown will have an impact on foreign sales for 2019.

The second headwind markets will have to contend with is reduced liquidity in global financial markets. Next year we are likely to witness the largest annual contraction in the big four central bank balance sheets since the great global financial crisis a decade ago with the U.S. Fed seen as the greatest culprit. The U.S. Fed began to shrink its balance sheet this year and will continue to do so heading into 2019, while the European Central Bank (ECB) is slated to end its quantitative easing program this year. The Bank of Japan (BOJ) is expected to continue expanding its balance sheet next year, however, they have already been undergoing a stealth tapering of their monthly purchases as the annual growth rate of their balance sheet has decelerated from peak annual growth of 47 percent in 2014 to 6.5 percent currently. As shown in the figure below, balance sheet growth for the big four central banks will turn negative in first quarter 2019.

In addition to reducing global USD liquidity by shrinking its balance sheet, the Fed is also expected to continue its tightening policy, raising interest rates next year as the U.S. labor market continues tightening. Recent nonfarm payrolls data showed job gains of 250,000 for October with the unemployment rate holding steady at 3.7 percent. One of the most notable developments in the job’s report was the pickup in annual wage inflation to 3.1 percent. It’s the highest growth in wage inflation since April 2009 which is likely to put continued pressure on the Fed to push forward with its rate-raising program. An aggressive Fed compared to global central banks will likely put upward pressure on the USD, further restraining global USD liquidity which is severely punishing emerging markets this year.

Stocks will have to contend with a third development in 2019: rising margin pressures from various fronts. As mentioned above, annual wage inflation for October hit 3.1 percent, the highest reading in nine years. With the cost of labor equal to the largest cost of goods sold for many companies, rising wage inflation does not bode well for profit margins. In addition to rising labor costs, we are also seeing a general rise in material costs. The Producer Price Index (PPI) core inflation gauge (removing food and energy) rose to an annual inflation rate of 2.7 percent in September, the highest reading seen in six years. Core consumer inflation, as measured by the Consumer Price Index (CPI), rests near the upper annual inflation range of the last decade. An ongoing trade war with China is impacting manufacturing as we saw in the October’s Institute for Supply Management’s (ISM) Purchasing Managers Index (PMI). Comments from some of the businesses surveyed are provided below.

October 2018 Manufacturing ISM Report on Business

“Tariffs are causing inflation: increased costs of imports, increased cost of freight and increased domestic costs from suppliers who import.” (Chemical Products)

“Protein prices continue under pressure from heavy U.S. supplies and export concerns related to trade tariffs. Higher costs related to trade tariffs are starting to be passed on to the cost of goods sold.” (Food, Beverage & Tobacco Products)

“We continue to run at full capacity. I continue to see pricing pressures and longer lead times in most commodities.” (Primary Metals)

“Mounting pressure due to pending tariffs. Bracing for delays in material from China — a rush of orders trying to race tariff implementation is flooding shipping and customs.” (Miscellaneous Manufacturing)

“Steel tariffs continue to negatively affect our cost, even though we utilize U.S. sources for steel. Oil prices put meaningful upward pressure on cost. Continued tightness with truck drivers is expected.” (Petroleum & Coal Products)

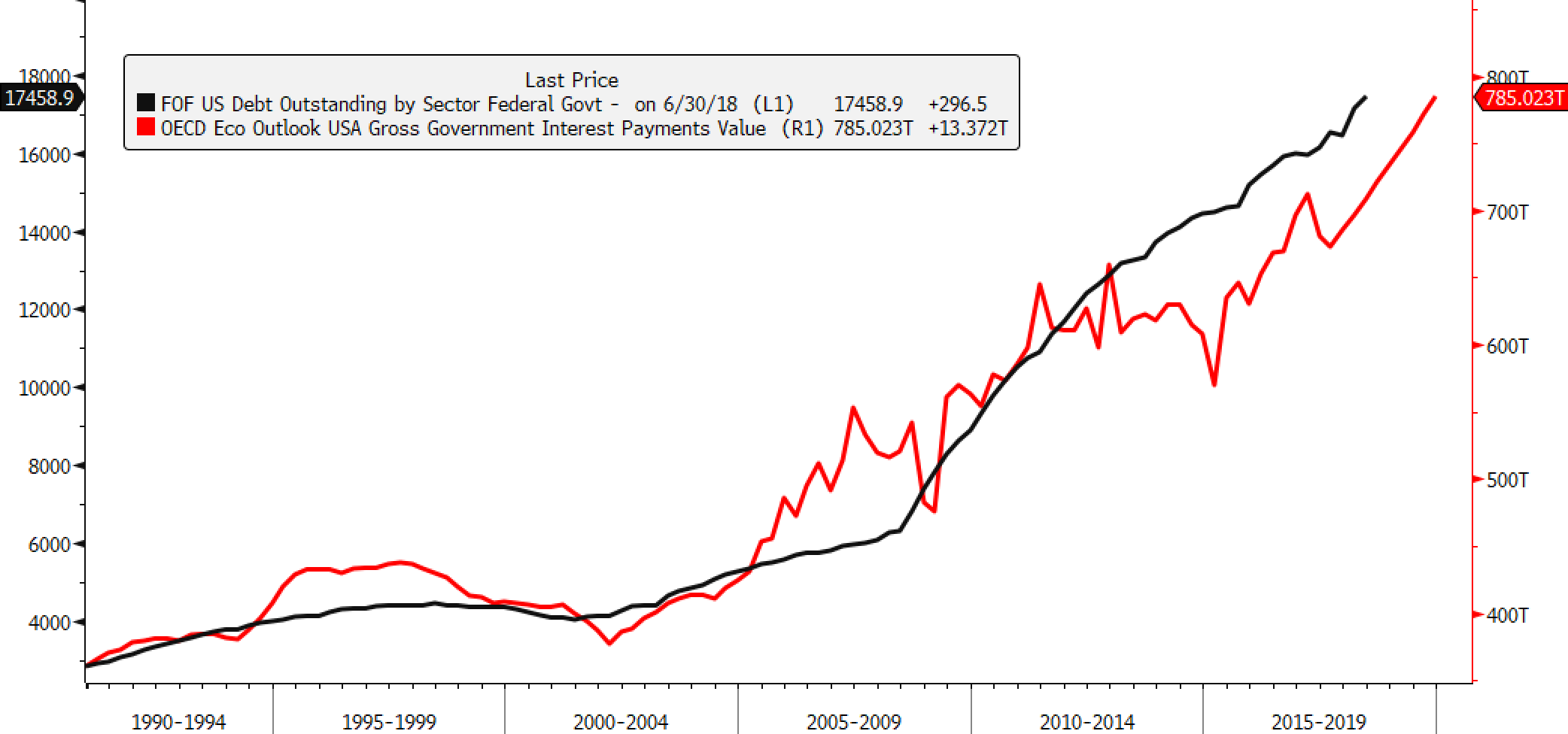

Another expected source of margin pressure in 2019 is a continued march higher in interest rates, which increases financing costs for corporate America. The U.S. Fed is expected to raise interest rates several times next year which impacts short-term interest rates. It’s the U.S. Treasury that’s likely to influence long-term interest rates next year much as it did this year as it issues increasing amounts of debt to cover Trump’s tax stimulus.

Treasury Expects to Issue Over $1 Trillion in Debt in 2018

The Treasury said Monday it expects net marketable debt to total $425 billion in the fourth quarter, which would bring total debt issuance in 2018 to $1.338 trillion, compared with $546 billion in 2017. That would be the highest annual debt issuance since $1.586 trillion in 2010, when the U.S. economy was still crawling out of a recession…

Rising federal budget deficits are boosting the Treasury’s borrowing and could restrain economic growth as the cost of credit also rises…

The deficit is headed toward $1 trillion in the current fiscal year, the White House and Congressional Budget Office said. The Office of Management and Budget projects the government is likely to run trillion-dollar deficits for the next four years.

In addition to trillion-dollar deficits, we’re likely to start seeing trillion dollar interest payments. The Organization for Economic Cooperation and Development (OECD) projects U.S. government interest payments to exceed three-quarters of a trillion dollars next year. They’re expected to reach an all-time high as rising interest rates on record amounts of U.S. government debt will increase this country’s financing costs going forward.

Relief Will Likely Come When the Fed or China Cry “Uncle”

The developments highlighted above: slowing global growth, reduced USD global liquidity, and rising margin pressures are likely to produce a choppy ride for financial markets heading into 2019. Therefore our plan will be to use market strength between now and the end of the year to raise cash and cut losses in losing positions. We believe that the completion of 2018 stock buybacks are likely to push stocks higher into year-end, providing us an opportunity to position defensively heading into next year.

Markets are likely to remain choppy until one of two catalysts emerge: Either global growth stabilizes as China launches fiscal and monetary stimulus to turn around their slowing economy or the U.S. Fed hints they’re near the end of their rate raising cycle. Already, the Fed’s rise in interest rates appears to be putting in a peak for two major areas of the economy: housing and auto production. Any further rate increases in the coming months will continue pressuring these cyclical areas. While auto production and housing are already rolling over, we’ve yet to see the economy roll over due to Trump’s tax stimulus. However, as the tax stimulus begins to fade and as the Fed’s tightening cycle continues, we should see growth begin to cool going into next year which may give the Fed some cover to halt their rate raising program.

On the global growth front, China’s manufacturing Purchasing Managers Index (PMI) for October came in at 50.2, the lowest reading since July 2016, and shows no sign of stabilizing. China’s slowdown is weighing on global growth where the global manufacturing PMI came in at 52.1 for October—the lowest reading since November 2016. China has only marginally eased financial conditions this year but not to the degree of their easing cycle back in 2016 which spurred a 2-year global growth upturn, and they haven’t undertaken significant fiscal stimulus yet. It appears for Chinese government authorities and the U.S. Fed there needs to be more economic and financial pain before they alter their course. This is why our plan going forward is to have a defensive stance until circumstances change.

To find out more about Financial Sense® Wealth Management or for a complimentary risk assessment of your portfolio, click here to contact us.

Advisory services offered through Financial Sense® Advisors, Inc., a registered investment adviser. Securities offered through Financial Sense® Securities, Inc., Member FINRA/SIPC. DBA Financial Sense® Wealth Management.