Consumers Are Feeling Ho-Ho-Hopeful

Consumer spending was up in October, signaling two-thirds of the economy is still showing optimism with their wallets, despite recent weakness abroad and a rough quarter for the stock market.

There is soft data suggesting sluggish sales due to slower mall traffic in physical stores and shopping malls over the Black Friday weekend. Yet other data suggests online holiday shopping is leading the charge in consumer spending; internet sales for the Wednesday before Thanksgiving through the Friday after surged 26.4 percent year-over-year according to a recent report by Adobe Systems who tracks online sales data.

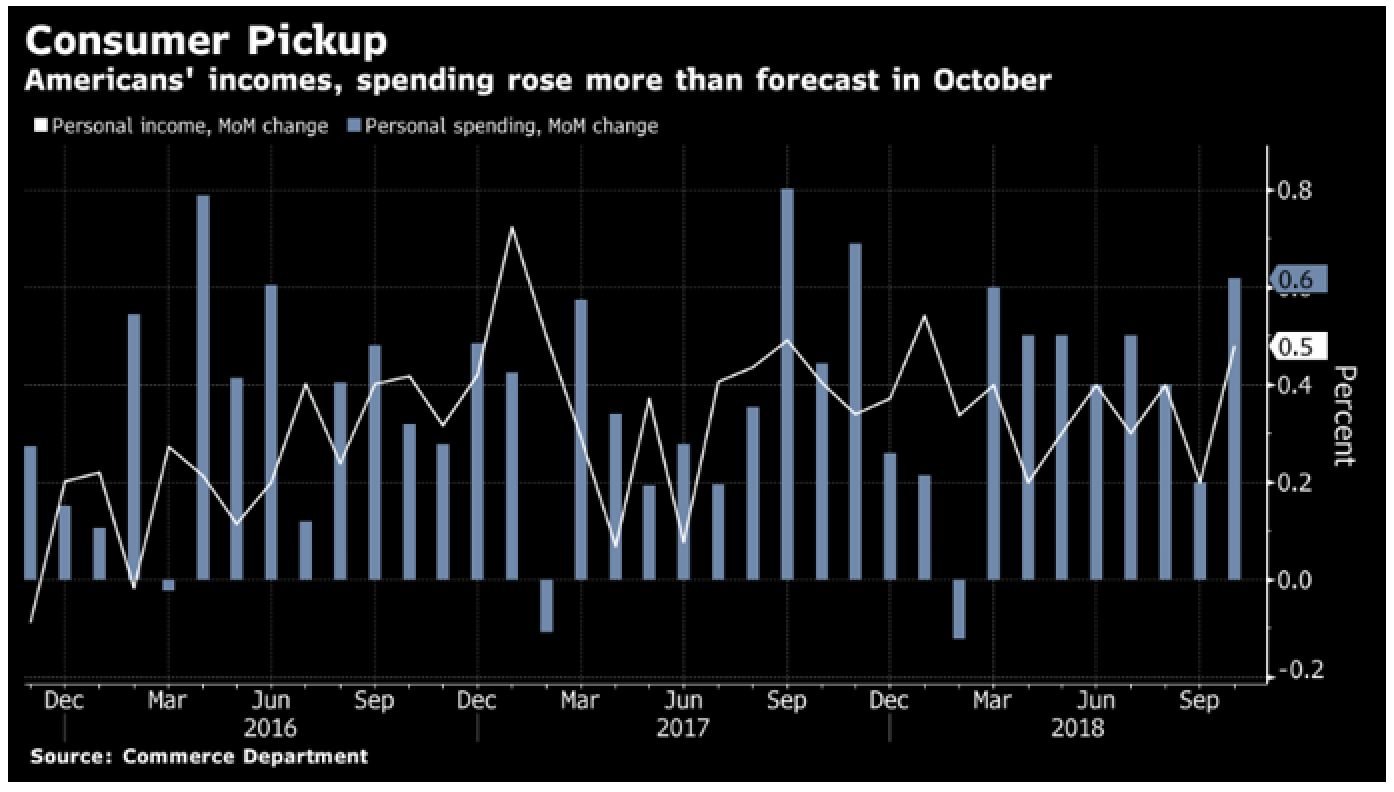

Other data releases from last week suggest that consumers are full of holiday cheer. Last Thursday, the Department of Commerce reported an increase in consumer spending for the month of October. Spending rose 0.6 percent after beating expectations of 0.2 percent from the month prior. Consumer spending accounts for nearly 70 percent of the economy and was projected to moderate following a strong summer for consumers, according to Bloomberg. The October’s PCE reading (Personal Consumption Expenditure price index excluding food and energy – the Fed’s favored gauge for measuring inflation) was up 1.8 percent year-over-year but down from 1.9 percent from the previous month – which supports recent comments from several Fed members that inflation is near their two percent target.

Despite exuberant numbers in October’s consumer spending report, weakness in rate sensitive industries continues to be a concern and will likely worsen as rates move up. Demand in the auto sector continued to deteriorate in October. “The flat reading on real spending on autos in October suggests the situation is not going to improve in the fourth quarter,” according to Carl Riccadonna, Chief Economist at Bloomberg.

Other rate-sensitive areas like housing are showing continued weakness and Core Logic's Ralph McLaughlin gave an excellent breakdown of the short and long-term outlook for housing last week on FS Insider (see U.S. Housing Market Update with Core Logic’s Ralph McLaughlin). With factors such as decreasing affordability and faltering demand, October’s new home sales reading was down 8.9 percent month-over-month, missing estimates of 4.0 percent growth from the previous month. Pending home sales were also down for the month of October, contracting by -2.6 percent from the month prior and missing estimates of 0.5% percent according to Bloomberg.

What Came Out of the G-20 Summit?

Friday kicked off the G-20 summit in Argentina. However, most of the anticipation this weekend focused on the outcome from President Trump’s meeting with Chinese President Xi Jinping. On Saturday evening, both leaders met over dinner and agreed to a “cease-fire” and to move forward with negotiations to ease trade tensions. By the end of the meeting, the Trump Administration agreed to not tack on additional tariffs as well as postpone a scheduled increased in tariffs on $200B in Chinese goods which were set to increase from 10 to 25 percent on Jan. 1 according to sources at the Wall Street Journal (soft pay-wall).

China also agreed to play a more proactive role purchasing more agricultural, energy and industrial goods from the U.S. and to give American businesses greater access to their trade markets.

According to people familiar with the matter, officials have already set plans in motion to work out the details of the negotiations in Washington later this month. However, even though both countries came to an initial agreement over the weekend, a lot still needs to happen for changes to take form. For now, we’ll concentrate on the positive element in this recent development: An important first step was made toward a trade agreement between the two of the world’s largest economies.

Emerging Opportunities Abroad – Driven By Softer USD

In my article from last week, I gave anecdotal evidence from numerous Federal Reserve members suggesting that they are quite near their destination on the road to a neutral policy rate. In an Oct. 3 interview with CNBC, Jerome Powell indicated continued rate hikes going forward: “We may go past neutral, but we’re a long way from neutral at this point, probably.”

Last week was significant for the Fed and expectations for monetary policy heading into 2019 given current economic and market conditions. On Nov. 29, Fed Chairman Powell gave a speech at the Economic Club of New York signaling a subtle shift in his policy rhetoric from several weeks ago. “Interest rates are still low by historical standards, and they remain just below the broad range of estimates of the level that would be neutral for the economy,” Powell said.

The markets took note of Powell’s comments as a dovish shift from more recent hawkish rhetoric supporting the Fed’s raising interest rates two to three times next year; signaling the Fed may be more accommodative heading into 2019. Powell’s comments put downward pressure on an elevated USD which has crippled world currencies this year. The USD was down nearly 50bps with most world currencies up after the comments.

In the past week, world currencies including the yuan, Mexican peso and euro have clawed back some gains against the dollar as shown above. With recent normalization of an already elevated USD, emerging markets as measured by the MSCI emerging markets index (a market cap weighted stock market index of 1,649 stocks from companies throughout the world), shown below in orange overlaid by the dollar in black (inverted), has improved in the short-term but have not confirmed a bottom in their downward trend. One thing we are watching for is a continued break down in the USD since further softening could position emerging markets for a short- to intermediate-term rally.

A run up in gold (shown in black) from its current levels could also confirm a break-down of the greenback in the short term (shown inverted below in blue). However, gold’s recent move up has not been followed by a significant pull-back in the USD so the recent divergence highlighted below begs the question: who has it wrong?