Anyone who has taken a cruise knows that the seas, though often calm, can quickly turn treacherous. Those, like myself, who are prone to bouts of seasickness appreciate the inclusion of stabilizers on each side of a ship’s hull.

These stabilizers (see image below) act like flaps on an airplane, deflecting water as needed to minimize the rocking and rolling motion of the vessel. The end result is a steadier voyage, with fewer passengers needing to unload the contents of their stomach orally.

Once back on shore, however, passengers may still get queasy from the rocking and rolling in both our financial markets and economy. As we all felt this past Christmas Eve, these bouts of market sickness can be just as bad, if not worse, than being out in stormy seas.

But thankfully, our economy and financial markets have their own set of stabilizers. Most of these are behaviorally driven and operate in feedback loops, while others (such as changes to monetary and fiscal policy) tend to act more like a ship’s captain changing course.

Today I’d like to discuss a few of these stabilizers because it’s important to understand the opposing forces that are constantly at play. It’s the net effect of all these forces that dictate the ultimate direction of our economy, so it helps to understand these offsetting effects.

Let’s begin with one of the largest and most fluid stabilizers – currency exchange rates. When an economy is growing strongly, it tends to attract investment from outside its borders. This outside investment results in increased demand for the domestic currency, often pushing the exchange rate higher.

A stronger currency may sound good in theory, but it often acts as a penalty, increasing the cost of a country’s exports and dampening that component of economic growth. At the same time, those countries who see their currencies weaken obtain a relative advantage, as their exports become more desirable.

In a very real sense, fluctuating exchange rates therefore share and redistribute economic growth by changing the relative attractiveness of each country’s exports and imports.

Here in the U.S., we’re already seeing this dynamic at play as concerns of an economic deceleration are reducing demand for the dollar. In the chart below we can see the dollar index heading lower; it’s already collapsed beneath the 50-day moving average and is approaching the 200-day.

The magnitude of this move so far is minimal, but nevertheless it’s evidence of one type of economic stabilizer kicking in. If the U.S. economy continues to slow, the dollar should continue to decline, and that will act as a partial buffer against further slowing.

Another area where we see similar behavior is with interest rates, both at the long and short end of the yield curve.

At the short end, which is controlled by the Fed, the feedback loop involves the Fed “getting it.” Once the Fed recognizes that conditions are deteriorating, they tend to adjust their forward guidance, thereby reducing the likelihood of future rate hikes and the resulting strain on the economy. As things get worse, rate cuts will actually take place, which act to stimulate demand.

One of the interesting dynamics we’ve seen recently is the market shifting to a belief that moving forward, rate cuts are actually more probable than rate hikes. We can see this in the chart below, which looks at fed funds futures data for the December meeting at the end of this year.

As you can see, the highest probability outcome is for the federal funds rate to remain at the same level it is now (2.25 percent – 2.50 percent). But perhaps more interesting is that market participants are placing a higher probability on a rate cut (15.2 percent) than on another rate hike (12.1 percent). In effect, this is the market telling the Fed, “enough is enough.”

We see a similar dynamic play out at the long end of the yield curve, but this one doesn’t require the Fed’s intervention. As you can see in the chart below, the yield on the bellwether 10-year note has fallen considerably over the past two months.

As bond investors become more and more worried about a recession, they tend to shift their investments toward longer dated bonds. The idea is twofold: Locking money away for longer periods of time negates the possibility of having to reinvest that money during a downturn, when rates could be much lower (bond prices higher), and longer-dated bonds have a higher duration, meaning their prices will rise proportionally more if and when rates do move lower as a result of the recession.

This is why we tend to see flat and inverted yield curves as conditions deteriorate. Our next chart highlights this, as we can see the slope of the current yield curve in red, with the curve’s recent shadow in black. Other than the very front of the curve, which again is controlled by the Fed, interest rates have fallen quite literally across the board.

I don’t think I need to explain the stimulatory effects of lower interest rates, but hopefully this chart provides clear evidence of another “stabilizer” that’s acting to keep the economy upright. Lower rates should breathe some renewed life into both the housing and auto sectors, which are strongly affected by borrowing costs.

These two factors – lower interest rates and a cheaper dollar, are major drivers within the economy and it’s fair to say they’re already helping us out. But as always, the question is whether it’s enough.

There’s another stabilizer I want to touch on briefly and this one is a little more abstract – the labor force participation rate. I’m not sure we can say that this effect is always present, but it seems to be now.

As the economy continues to expand, it draws people back into the labor force who otherwise may not look for work. The reason I consider this to be a stabilizer is because the addition of entrants to the work force helps keep the unemployment rate from falling too low. That subsequently has the dual effect of suppressing wage inflation (and in turn actual inflation), thereby eliminating the need for additional rate hikes. Without these new entrants, it’s possible that both inflation and interest rates would both be higher.

And just to come full circle, we have stabilizers that act in the opposite direction as well. When the economy does roll over, and Americans begin losing their jobs, unemployment insurance kicks in to offset the drop in spending from these individuals.

But while this information is interesting (at least to me), it still remains very difficult to aggregate all the forces in the economy to determine what outcome is most likely, and therefore what asset prices will do. Is there anywhere we can look to try and find the sum of all these forces?

The answer is yes, and we tend to refer to them as leading indicators. Generally speaking, these opposing forces will act upon the leading economic indicators in the economy first, providing a (semi-opaque) window into what’s to come.

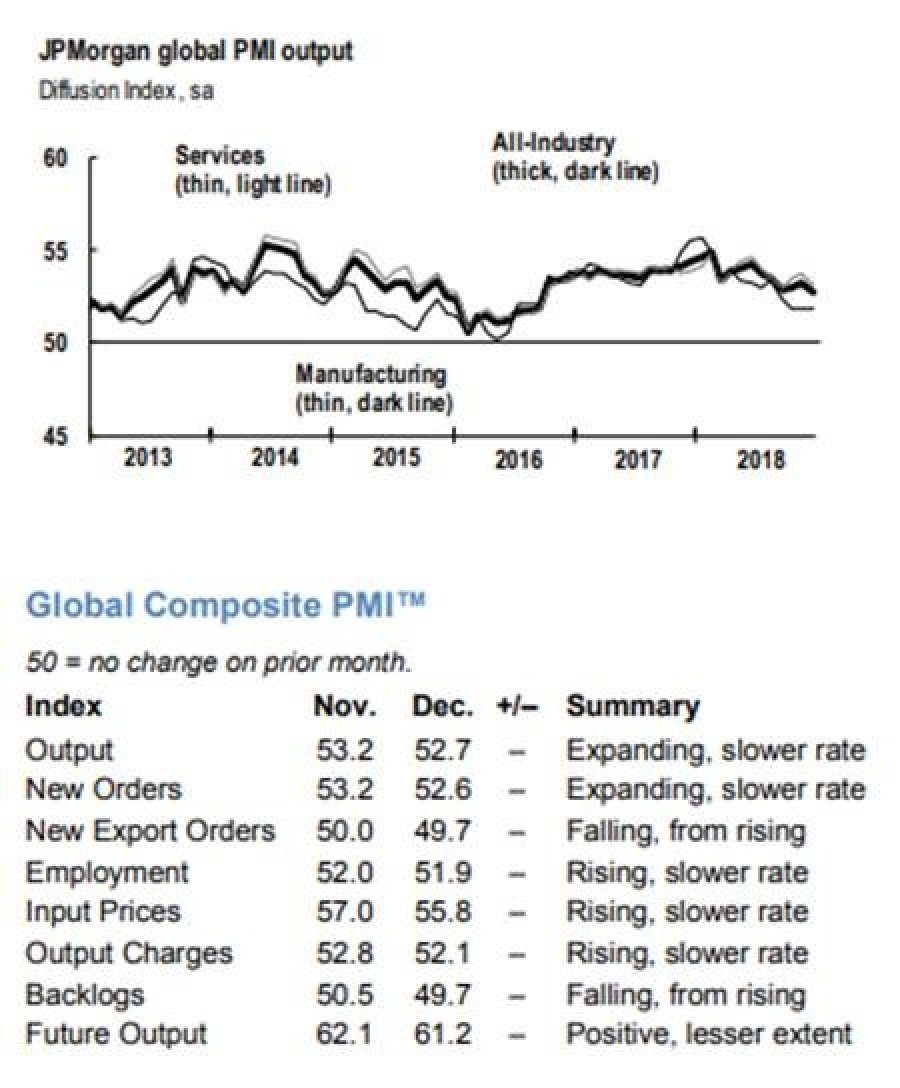

As we’ve discussed recently, some leading indicators are flashing yellow (such as the yield curve) while others remain fine. I’d like to end today’s note with a brief look at global PMIs, courtesy of J.P. Morgan.

In this chart we can see the global services PMI (thin gray line), the global manufacturing PMI (thin black line), as well as the composite PMI (thick black line). All three measures remain in a sustained downtrend, with the composite PMI tracking at a 27-month low. If there’s a silver lining here, it’s that all three indicators remain above the 50 line, which denotes expansion.

One thing worth pointing out is how well the composite PMI shown above correlates with moves in the stock market. Notice that the composite PMI bottomed in early 2016, at about the exact time global equity markets hit their bottom following a rocky 2015.

The composite PMI then topped out in early 2018, right at the time when we saw our January blow off top. U.S. equity markets did reach a new high in September (see top panel below), but interestingly, global markets, as represented by ACWI – the All Country World Index (lower panel), did not.

So at least from an anecdotal perspective, it would seem that the global composite PMI is providing a good analog for global equity markets. If that relationship continues to hold, then the continued downward trend in the global composite PMI may indicate further weakness ahead for equities.

I mentioned a few weeks ago I would try and point out when the market rebounded enough for those who wished to take some chips off the table to do so. Considering the voracity with which the market has rebounded from the Dec. 24 low, now may be a good time to initiate that process.

As you can see below, the S&P 500 has risen back up to near the previous support level (now resistance) that the market collapsed through in early December. That resistance could prove formidable and may end up sending the index lower in the near term.

Of course that outcome is by no means guaranteed, but at least now investors have an opportunity to reduce exposure at about 11 percent below the S&P’s high water mark (if this fourth quarter’s action happened to provide a wake-up call).

The preceding content was an excerpt from Sigma Point Capital. To receive their weekly updates and research, click here to subscribe. Matt is also the Chief Investment Strategist at Model Investing. For more information about algorithmic based portfolio management, click here.