Originally published at The Boock Report.

This is not a survey I had seen before but it adds to the mixed messages we are getting from the data. The WSJ survey of small businesses index fell to the lowest level since the presidential election. "Just 14 percent of firms expect the economy to improve this year, while 36 percent expect it to get worse." The lone caveat is that this survey was done right before the government reopened but I don't think businesses expected the closure to last that long anyway. Reflecting the conflicting signals, one CEO said "I'd rather play it safe at this point. I'm divided right down the middle. Half of me is very positive. Half of me is very nervous."

What confidence data leads to we'll of course have to see but at the minimum if CEOs are more cautious, it naturally leads to a hesitancy on hiring and investment until they become more confident again. Please view Friday's payroll data as lagging… those decisions to hire likely took place over the months prior.

The slowdown in Europe is reflected in the Sentix investor confidence index in the Eurozone. It fell to -3.7 from -1.5 and that's the lowest since November 2014. Sentix said "Even in February, the bad news for the economy in Euroland is not abating."

SENTIX ECONOMIC CONFIDENCE INDEX

I'm going to highlight again the weakness in European bank stocks. The Euro STOXX bank index is down for the sixth straight day to a one month, lower by 1.4 percent today. This is a 30-year chart. I certainly attribute much of the weakness over the past few years to NIRP and what was done to the yield curves in the region. The ECB unfortunately has completely deflected criticism. How is Europe going to have any, healthy growth when the lifeline of so many companies and households has such challenges?

EURO STOXX BANK INDEX

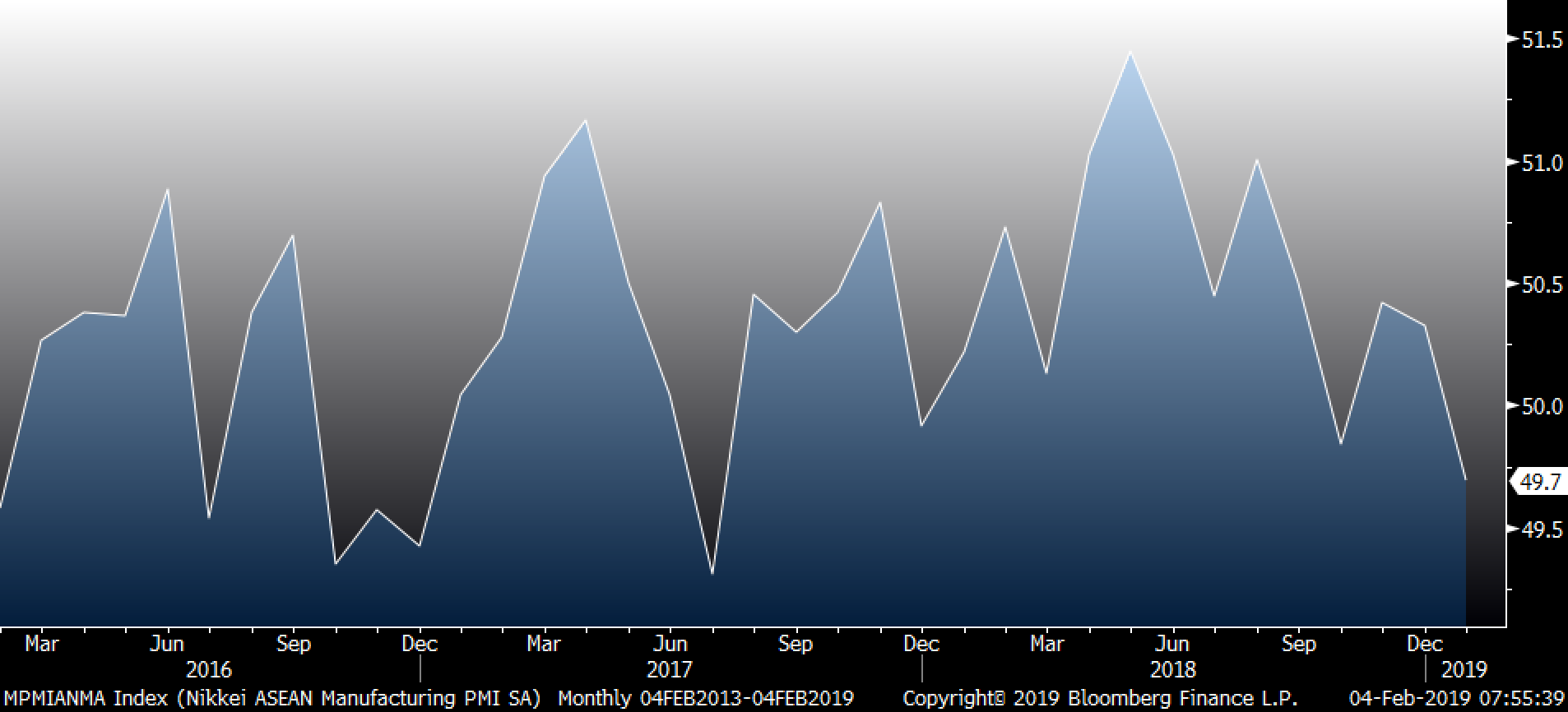

Aggregating the manufacturing PMI's from Singapore, Malaysia, Indonesia, Thailand, Myanmar, Vietnam and the Philippines, all very reliant on China, now looks like this:

ASEAN MFR'G PMI

It's back below 50 and Markit said, "Export demand was still a key factor weighing on the sector's performance, as trade tensions around the world caused export orders to fall for the sixth month running." A deal between the U.S. and China will go a long way in easing worries but China's growth is slowing regardless.

The pace of the expansion of the Bank of Japan's balance sheet continues to slow on a year-over-year basis. Their monetary base was up 4.7 percent year-over-year in January vs 4.8 percent in December. That marks the lowest increase since early 2012, before Abenomics and the three arrows took hold. Bond yields, kept low now by yield curve control, has been mostly influenced of late by worries about global growth. The 10-year JGB yield is yielding (if you can call it that) -.009 percent. With the BoJ giving license to a +.20 percent yield, it is saying something about growth expectations. So is a German 10 year yield at .16 percent or a U.S. one at 2.70 percent, 45 basis points below where it was at the end of October.

For daily macroeconomic analysis and asset class positioning, visit boockreport.com.