“By a continuing process of inflation, government can confiscate, secretly and unobserved, an important part of the wealth of their citizens.” –John Maynard Keynes

“Inflation is not caused by the actions of private citizens, but by the government: by an artificial expansion of the money supply required to support deficit spending. No private embezzlers or bank robbers in history have ever plundered people’s savings on a scale comparable to the plunder perpetrated by the fiscal policies of statist governments.” –Ayn Rand

An Invisible Enemy

We are in a state of war and the economy is on a war-time footing. It is a different kind of war unlike others we have fought. No armies are lined up on opposing sides of the battlefield. There are no tanks, no soldiers wielding guns, no planes dropping bombs, nor missiles being fired. It is a war fought against an unseen opponent; an invisible virus that has killed thousands of Americans and citizens worldwide.

The frontlines are hospitals, the soldiers are doctors and nurses, and the casualties of war are ordinary citizens young and old alike. Instead of battlefields, there are hospitals; in place of fox holes, there are homes and apartments; the citizenry awaiting the “all clear” call from our leaders: “it is safe and you are free to go outside.”

Rather than war-time production, most industry is shut down. Many companies are unable to get needed supplies of intermediate goods, unfinished products, or in some cases raw materials. Instead of bullets, missiles, bombs and tanks, the nation’s industrial base has switched to making masks, respirators, and sanitizers. What is needed is not more armaments but hospital beds, respirators, drugs and vaccines (see America's Dangerous Reliance on China for Medicine).

Like all wars, this one will be costly as the government ramps up spending by guaranteeing wages to workers unemployed or furloughed, financing to companies to keep workers on payrolls, loans to businesses and industries shut down by government edict or the collapse of demand. This will be an expensive war to prosecute and it will cost in the tens of trillions before the war is won. Deficits will explode, and the national debt will rise to levels not seen since the last world war.

Emergency Powers

Governments are intervening in economies in ways considered unthinkable outside of wartime. They have pledged massive sums of money to support stricken companies and workers, coaxed or shut down industries or ordered others to switch production to essential goods, and in some cases seized control of supply lines in order to procure vital equipment. Key sectors of the economy such as airlines will be bailed out or supported by grants and loans (see Felix Zulauf on Why It'll Take 'Years' to Recover from Crisis).

Stay ahead of the news! Subscribe to our premium weekday podcast

Individual freedoms and rights are being trammeled as governors and mayors act as dictators limiting freedom and movement to what you can sell or buy. In March, the Democrat Governor of Michigan, Gretchen Whitmer, limited access of doctors from prescribing the lifesaving drugs hydroxychloroquine and Z-Paks to save senior citizens. In addition to attempting to control the prescription of drugs, the governor has banned the traveling between homes, seeing friends or family, calling on Home Depot and Lowes to shut down certain sections like flooring, paint, garden centers and plant nurseries, to prohibiting grocery stores from selling seeds. During WWII, victory gardens were encouraged; the Michigan governor now sees them as a threat.

Meanwhile, the government and the Fed take on new powers from propping up money markets, backstopping the currency markets through swaps with major central banks, propping up the commercial paper markets, unlimited purchases of government bonds and mortgages, to the recent unprecedented move to buy low-rated bonds and even exchange-traded funds of junk debt.

Casualties of War

We as a firm were active participants buying bonds at steeply discounted prices for clients from bond funds and ETFs who were selling at distressed prices to meet redemptions from panicky investors. Bond spreads were blown wide open and we had a brief opportunity to buy fallen angels at steeply discounted prices. Those spreads and discounted prices narrowed considerably as the Fed stepped in and bought heavily to prop up markets. Instead of freely functioning markets we now have controlled and propped up markets. Perhaps in a severe market downturn, stocks will be next on the Fed’s buy list.

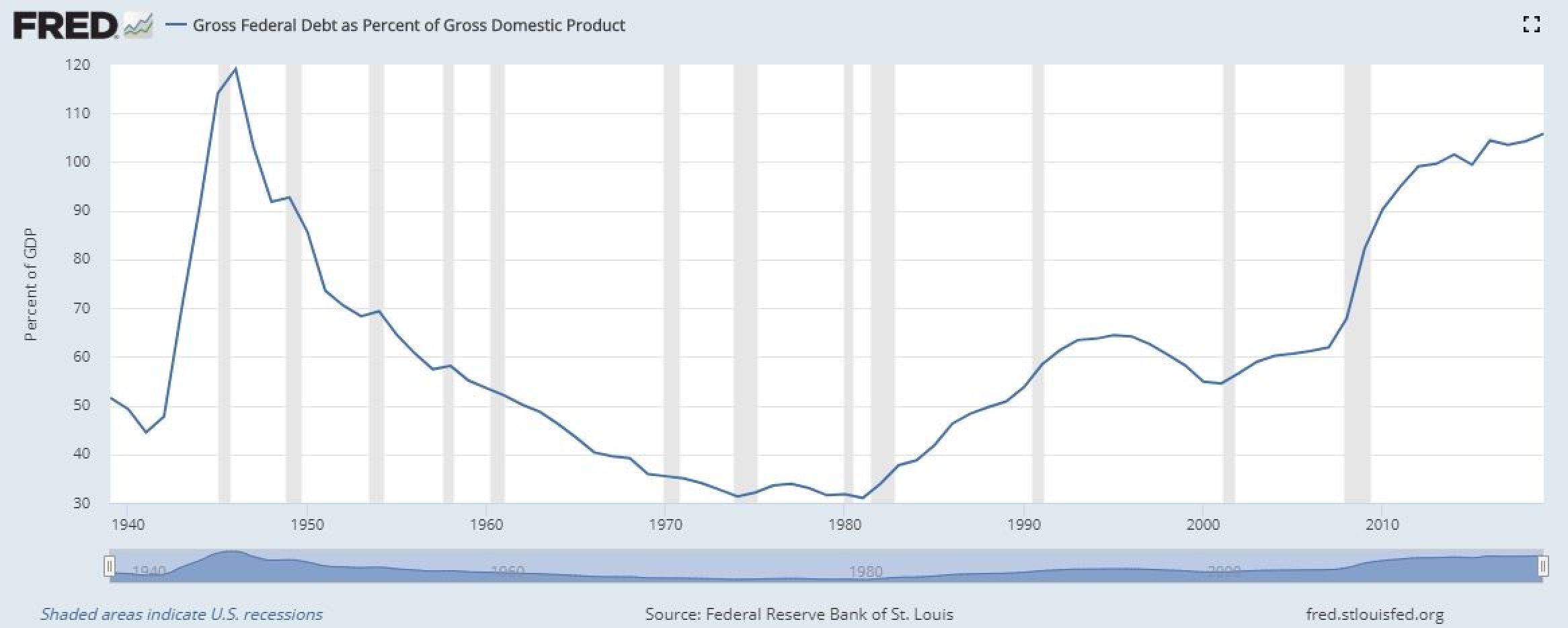

As government spending ramps up to prosecute the war and the longer the economy is quarantined or shut down, the larger the deficits and growth of our national debt. Government debt could soon rise to 130-140% of gross domestic product. Last year at this time the figure was close to 100% of GDP. Now we will be approaching debt levels last seen after World War II (see Jim Rickards on Runaway Debts and MMT).

Debt at these levels is only sustainable if interest rates remain low. In order to keep them low, central banks around the globe have engaged in open-ended bond-buying echoing back to WWII when the Fed committed to pegging long-term government debt to below 2.5%. As of April 15, 2020, Treasury yields range from 0.14 - 1.27% as shown in the table below.

While interest rates this low is great for debtors, especially the biggest debtor of all, the US government, it is wreaking havoc with institutions and individual investors. It is making it difficult for corporations to manage their cash, pension funds to fund their retirement liabilities, insurance companies to earn returns on their float, for retirees living on investment income, or investment managers to achieve total returns.

What makes this market even more precarious is the ultra-low returns on secure and safe money such as T-bills, CDs, to money market funds. The risk to today’s income investor is the return of inflation which market participants and experts don’t expect. I disagree with that view and will explain shortly as to why inflation rather than deflation is the longer-term outcome.

Everyone is scrambling to find yields from fund managers, corporate treasurers, to retirees. The markets have done a complete flip that I have not seen in a quarter of a century. The best yields can now be found in stocks from quality Dow companies, utilities, REITs to healthcare and energy if you know what to look for and understand. And, unlike bonds, those yields have a chance of rising each year keeping investors level with inflation. Who would have thought that less than 6 weeks ago the better yields would be found in stocks vs. bonds? We are seeing the yield spread between dividends on the Dow and 10-year treasury notes the highest we have seen in over a quarter of a century as shown below.

Creating Inflation from Thin Air

To obtain yields that protect an investor against inflation or against zero-to-nothing yields, will require going outside your comfort zone but the opportunities have never been greater. I will return to this subject in a moment but on to inflation.

How will this war be paid for? It will be paid for as all wars are paid for by rising taxes and inflation. The Fed will be doing most of the heavy lifting and it will not be long before the Fed’s balance sheet doubles again along with a doubling of the deficits and the national debt. Interest rates will be needed to be suppressed in order to keep debt payments manageable and inflation will need to rise in order to inflate away the debt. The US was able to grow its way out of debt through the suppression of interest rates by the Fed following WWII and by the growth in the economy and inflation.

In the last debt expansion accompanying the financial crisis, most of the Fed’s money creation remained at the Fed as banks accumulated reserves at interest rather than lend money into the economy. This time around, money is being injected directly into the economy through direct government stimulus of which the $2.2 trillion Coronavirus Aid, Relief, and Economic Security (CARES) Act is but the first of many installments to follow. Once direct payments become ingrained in the economy they are hard to get rid of, especially with politicians wishing to buy votes by handing out goodies in the form of subsidies.

On the other side of inflation is the supply of goods and services. Some goods are being restrained either by lack of availability as a result of supply-side disruptions from China as a result of the coronavirus, and in other cases by the shutdown and quarantine of business by government. There are also the new government controls that are being imposed on business from the federal, state, and local levels (see Martin Armstrong: Politicians Are Destroying the World Economy). I have already mentioned that some politicians are limiting what stores can sell or make available to consumers. Then there are the myriad environmental regulations to contend with that hamper and restrict the building of factories, the development of land, or to the mining of natural resources from oil to iron ore.

The trade wars and now the coronavirus are going to cause supply chains to be reoriented. There is hope and possible tax incentives for companies to relocate factories back home. But will that happen? Will environmental regulations and labor restrictions be waived or will we see companies bogged down in a sea of bureaucratic red tape as we have seen recently in efforts to get possible corona victims tested, or the release of needed drugs or medical equipment?

The US was able to grow its way out of debt through economic expansion, inflating away the debt, and the suppression of interest rates. Modern Monetary Theory (MMT) is the latest reiteration of that policy with a new “modern” twist, providing the economic justification for endless spending, deficits, and money printing. Government is at it again with longer-term implications for inflation. In any downturn in the economy or markets, the first impact is a deflationary wave as we are seeing now. It is the government response to that deflation that sets the stage for reflation, which is now unfolding through fiscal and monetary stimulus. It may take some time for this stimulus to kick in as the government blew a wide hole in the economy that will need large doses of stimulus to fill. But, eventually, with enough doses of stimulus we should see inflation begin to pick up, especially if the economy recovers, demand increases, and the price of energy begins to rise from its present lows.

As for my deflation friends who question the ability of the government to create inflation, I would reply by saying inflation has and has always been an issue with the supply of money. The government can by fiat create inflation when it is in its interests to do so. As an example, consider the graph of core price inflation (CPI) going back to 1914.

Notice the increase during the war years between 1914 and 1919, the deflation that followed the beginning of the Great Depression, the inflation that began after Roosevelt devalued gold in 1933, and when Nixon dropped gold backing in August of 1971.

It is my firm belief that debt levels are going to become too high to contain. As mentioned in my earlier article “The End of Money,” there are only three ways for a government to reduce its debt:

- Pay it back

- Default

- Inflate the debt away

Once we start seeing government debt levels approaching $30 trillion or more, suppressing interest rates will not be enough nor will taxation, which will suppress economic growth and revenues. At this point, there is no way out or turning back, the only answer will be what governments have done throughout human history which is to devalue the currency. I strongly believe with debt and deficits accumulating at breathtaking speed, a US dollar devaluation is in our future. I covered this topic in my “The End of Money” article so will not rehash that line of argument here other than to illustrate its effectiveness as shown by the graph of CPI above, including the devaluation and rise in inflation under Roosevelt.

Investment Implications

The question now is what to do as an investor? We prefer owning treasuries directly for corporations or individuals who want and need short-term liquidity. Many money market funds simply don’t earn enough for investors. We actually manage corporate cash for client companies in a special account. In a recent analysis of a corporate cash account held in a money market fund (MMF), the yield on the MMF was 0.07% with an expense ratio of 0.34%, meaning the client would earn 0% as long as the Fed keeps rates at zero which I believe they will do for a long time to come. In the last downturn following the Great Recession, they kept them at zero for seven years. Even worse was the examination of the fund’s holdings. Less than 45% of its assets were held in direct government securities with the balance coming from repurchase agreements with global banks. Half of the assets were invested outside the US.

In the new era of financial repression that we find ourselves in now, we favor direct ownership of securities or ETFs that can be purchased at a discount from net asset value. Other areas we think will do well are TIPS (Treasury Inflation-Protected Securities), high dividend-paying aristocrat stocks, preferred stocks, and gold. We have been absent the gold market for the last 7 years and returned beginning in 2018. We now own gold across all accounts. In my personal opinion, we are likely to see gold take out its old highs later this year or early next year.

Right now the markets are focused on deflation, falling energy prices, and a global recession as a result of a global pandemic. What is not seen or not expected is the return of inflation. That rogue wave is lurking out there and it is just a question of when it hits the economy and financial markets. It is not the present or what is known that one should be prepared for. It is what is unforeseen and unexpected that one should be prepared to navigate. Are you prepared for the coming storms? Caveat emptor!

To find out more about Financial Sense® Wealth Management or for a complimentary risk assessment of your portfolio, click here to contact us.

Advisory services offered through Financial Sense® Advisors, Inc., a registered investment adviser. Securities offered through Financial Sense® Securities, Inc., Member FINRA/SIPC. DBA Financial Sense® Wealth Management.

Copyright © 2020 Jim Puplava