We are starting to see signs that inflation is taking hold. Debate is raging among financial professionals and strategists as to whether it will prove to be transitory or end up more persistent and long-lasting.

Chris Puplava, CIO of Financial Sense Wealth Management, recently discussed why we are positioned for a more persistent, higher-than-average level of inflation in our latest weekly investment video.

To check out all our video webinars where we provide our macro view on the markets and the economy, go to our Video page or check out our latest at Weekly Update: Should Investors Turn Bearish as Inflation and Taper Talk Heat Up?

In this most recent update, Chris argues that economic growth will continue to surprise to the upside in the face of supply chain issues and low inventories, likely keeping inflation higher for longer. As well, this is not a bearish development for the overall stock market so long as commercial bank lending increases and we see consumers continue to drive the economy.

Here's a quick overview of the indicators and trends we believe investors need to keep on their radar...

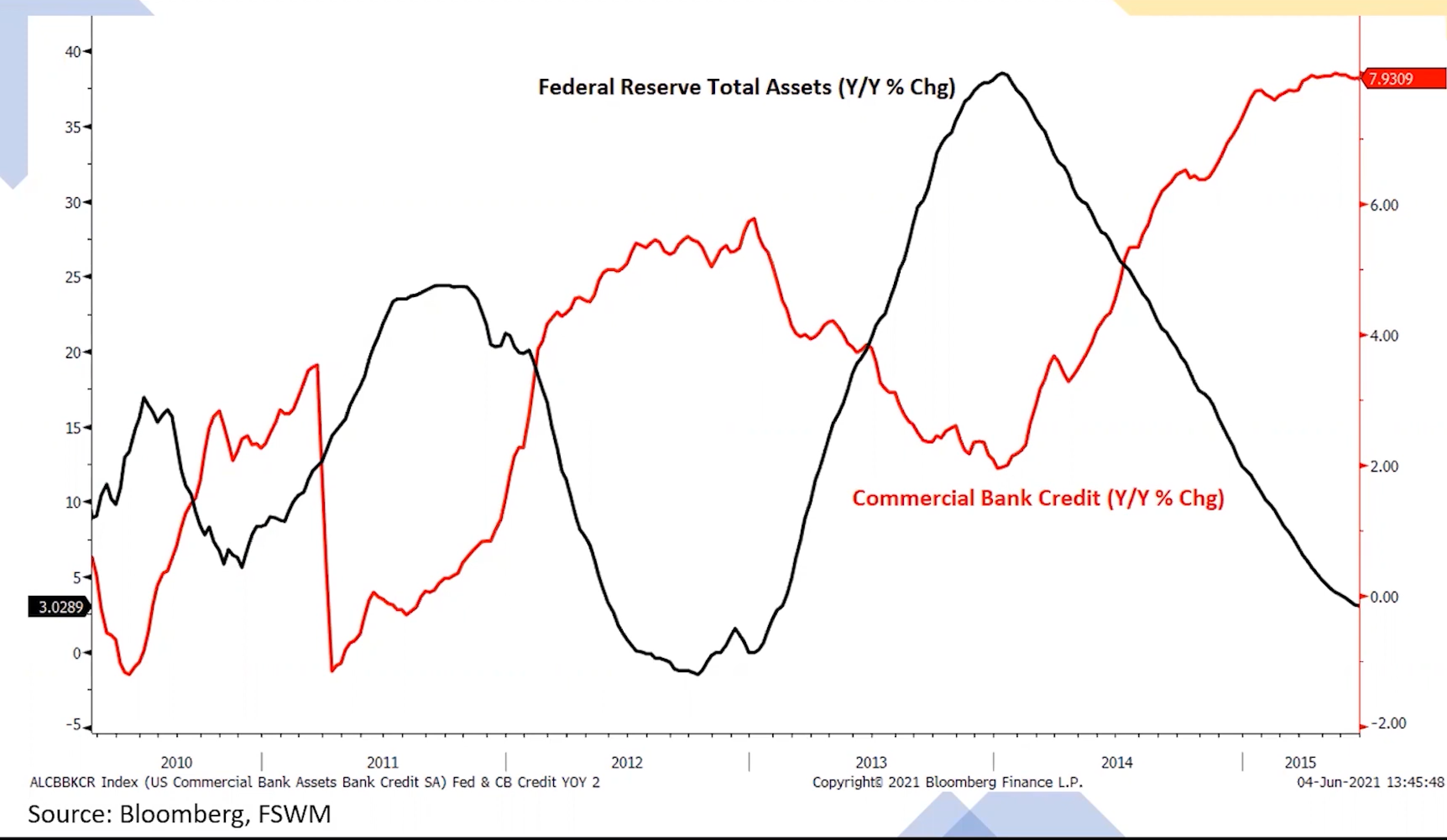

Fed and Commercial Banks

For the sustained economic growth forecast, Chris is keeping a close eye on the handoff in liquidity from the Federal Reserve via quantitative easing (QE) to commercial banks in the form of lending to businesses and consumers.

You can see the yin-yang relationship between the US central bank and commercial banks during the last economic cycle, particularly during the last tapering of their balance sheet in 2014. During that time, we saw a commensurate pickup in commercial bank lending, which helped to propel economic growth and the overall bull market forward.

“This chart highlights the Yin-Yang effect with the Fed and central banks... What we see is that as we were leaving 2013, going into 2014, peak Federal Reserve balance sheet growth was nearly 40 percent. Just before the Fed balance sheet growth peaked, we saw commercial bank credit growth start to accelerate. That really defined 2014, where we had falling central bank balance sheet growth, then a pickup by commercial banks. Because there was a successful handoff, 2014 was largely bullish for investors.”

“Thin Air” Credit

It is also necessary to consider the combined impact of the Federal Reserve and commercial bank lending, Puplava stated.

“This is what Paul Kasriel, former head of economics at Northern Trust, calls, ‘Thin Air Credit.’” Puplava said. “This is essentially money created out of thin air, which includes central bank plus fractional reserve lending by commercial banks.”

As credit growth increases, it tends to push interest rates higher. The opposite is also true; as growth decelerates, interest rates tend to head lower.

However, even though we see a deceleration of the Fed’s balance sheet, combined with commercial banks, thin air credit still remains elevated at nearly 15 percent year-over-year growth.

Stay ahead of the news! Subscribe to our premium weekday podcast

Compare that to what we saw during the period of quantitative tightening in 2018 and you'll notice the environment was quite different.

“Thin Air Credit” was declining from a growth rate of 5.5 percent in early 2016. Going into 2018, it was in the low single digits, Puplava added, corresponding to a flattening yield curve, which removed the incentive for banks to lend.

“When you think of the backdrop to this environment, this is very bullish for equities,” Puplava said. “We have very aggressive credit creation. We have a steepened yield curve, which incentivized banks to lend, and we have anchored short-term interest rates. This is a very bullish environment, not unlike the transition from 2013 to 2014. This as an environment that warrants an overweight position in stocks over bonds.”

Credit Growth Hand-off

If the Fed is going to start to taper, which most people believe will occur in early 2022, we want to see banks pick up the slack.

“It’s encouraging that when we look at commercial bank lending data over the last several weeks to months, it appears that we’re near a bottom in credit growth, and we're starting to see that pick up,” Puplava said. “I'm going to be watching that in the weeks and months ahead to see if we observe an acceleration in bank credit growth.”

The reason Puplava expects to see an acceleration in bank credit is in part due to the fact that the 2020 recession and bear market was unlike anything we've seen before.

Usually, recessions coincide with impairment of consumer balance sheets, impairment of corporate balance sheets, increasing rates of default, and higher levels of charge-off rates at banks. This time around, things are quite different, as shown below.

The chart above shows net charge off rates (the percentage of a lender's debt outstanding that is delinquent or bad debt) for credit cards by commercial banks going back to the mid 1980s. Currently, we see the lowest levels of charge offs on record.

Usually, banks experience higher rates of charge offs for credit cards during economic downturns, but that was not the case during this last recession. This time around, consumers used stimulus payments to pay down credit card balances and other debt.

We can see this same trend looking at credit card delinquency rates. Currently, we see some of the lowest credit card delinquency rates on record, Puplava noted.

There was a massive surge in commercial bank deposits in 2020 as the Fed began to flood the system with liquidity, and at the same time stimulus checks went out. Deposits have continued to grow from that point.

This indicates that a lot of money is available in the form of deposits for consumers to spend, whether to take out new loans or spend at retail. Prior to the pandemic, the consumer savings rate was in the low single digits, roughly around 3 percent.

“Even in the current scenario, consumers have roughly a 15 percent savings rate, which is why we were continuing to see deposits grow each week,” Puplava said. “There is a lot of scope in terms of consumers beginning to flex their muscles, and beginning to spend, pushing retail sales higher, drawing down the savings rate, and drawing down their deposits. This is why (we believe) there will be an incentive for banks to have a successful handoff from the Fed and see a surge in consumer bank credit.”

Inventories at All-Time Lows

The chart below shows current inventory-to-sales ratios for retail in blue with durable inventories relative to sales in red. Currently, the inventory-to-sales ratio is at 1.1, the lowest level we have ever seen since this data started getting collected. Also, looking at wholesale durable inventories to sales, we see a ratio of 1.5, one of the lowest levels we have observed in the last 8 years.

What this chart is telling us is that inventories have been severely depleted and will need to be replenished.

We have a long way to go just to get back to normal inventory levels, Puplava added. If this proves to be true, we will likely see persistent demand for commodities that go into making durable goods, textiles and other products.

This is likely to compound with persistent demand for components and commodities that go into motor vehicle parts. While some argue that commodity demand may have peaked, these charts argue for the opposite.

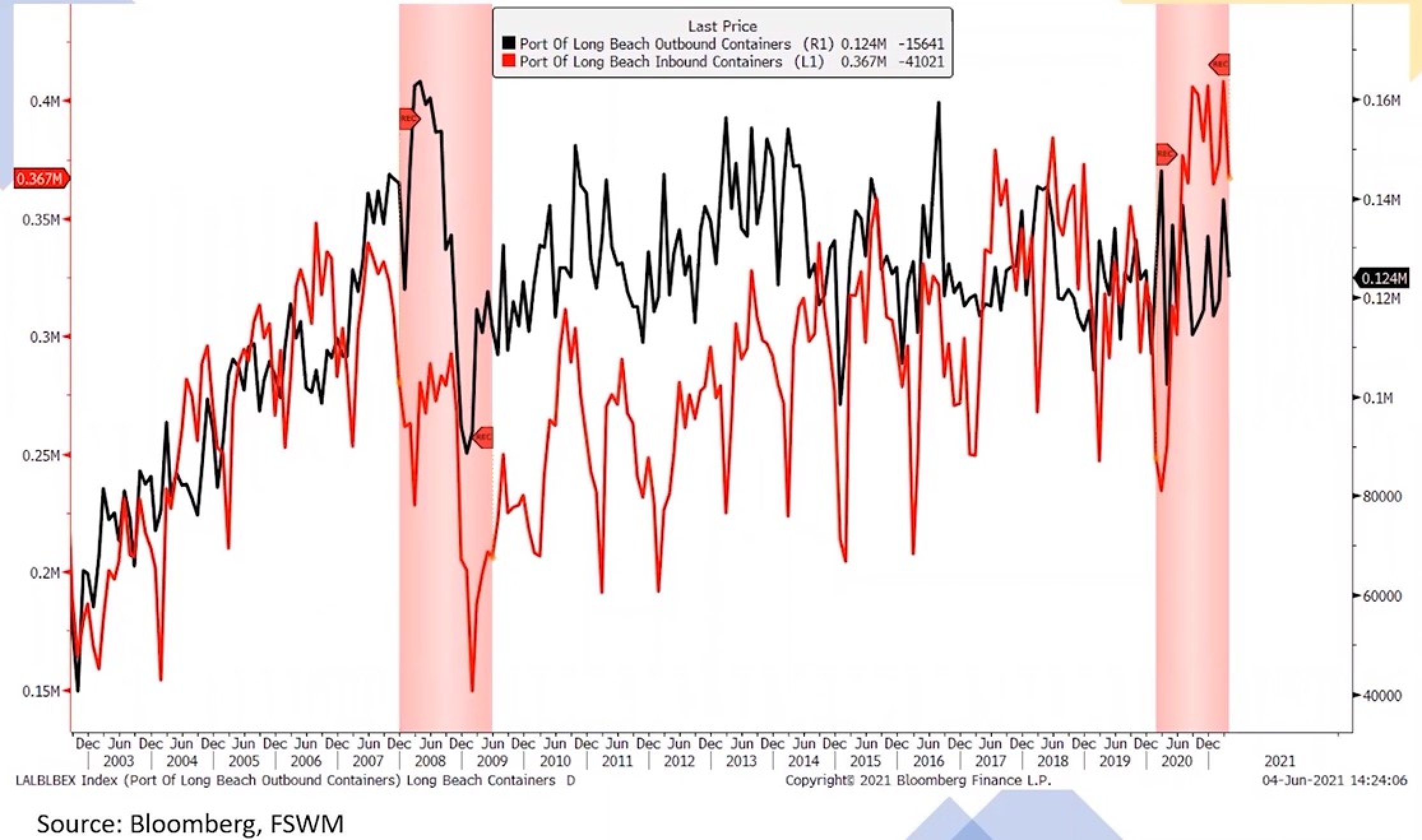

Shipping Data

Activity at U.S. ports bolsters this argument. Looking at the Port of Long Beach, one of the busiest ports in the country, the number of inbound containers is increasing.

During the last recession in 2008, we saw a collapse in inbound containers right as the U.S. economy began to slip into recession. We were not importing goods from abroad at that time.

“Now, the opposite is true,” Puplava said. “When stimulus checks went out, demand for goods surged. We also see that inboard containers continued to remain at record levels. It is absolute gridlock at the Port of Long Beach right now. I've heard of manufacturers not being able to get parts because they're stuck on ships.”

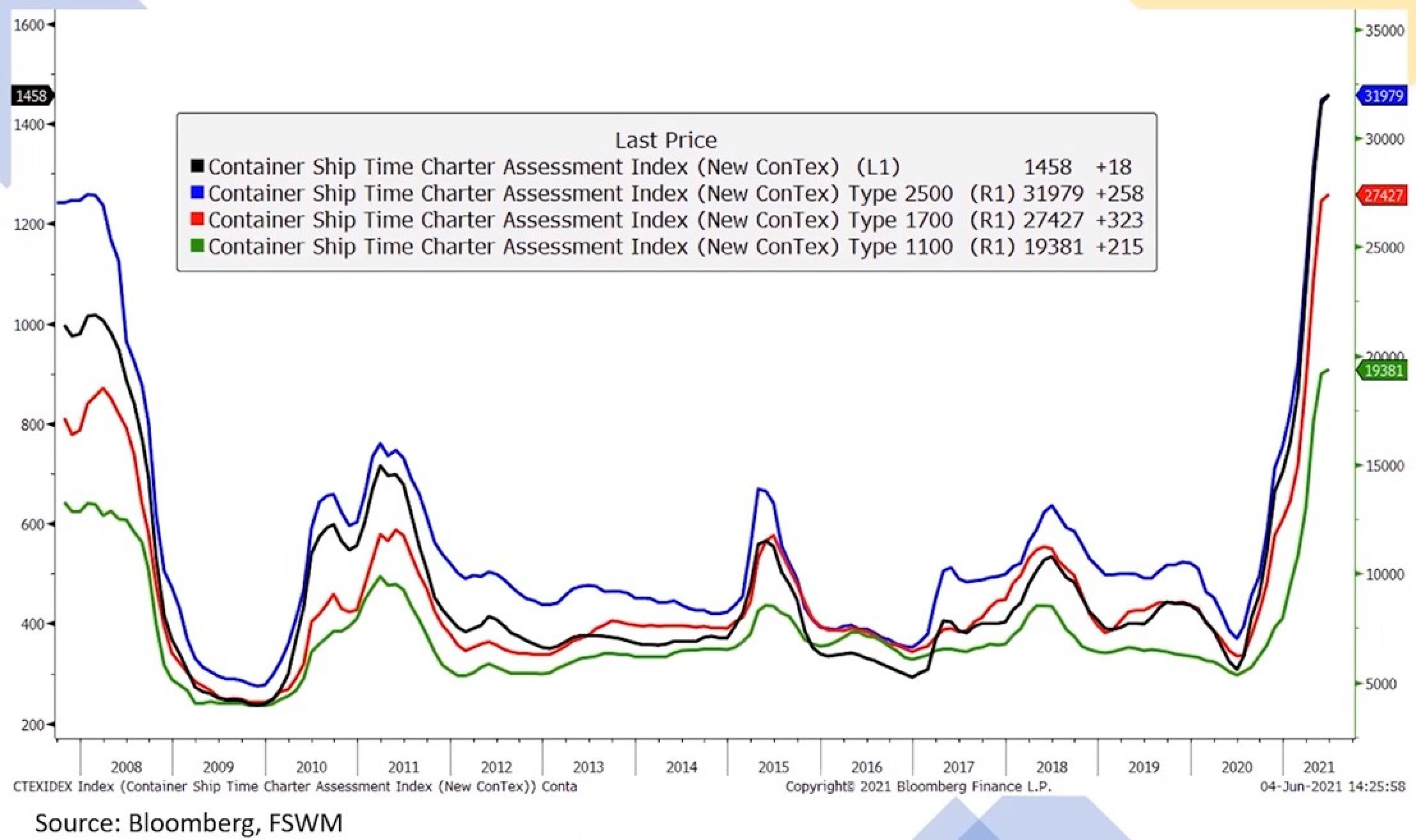

This same bottleneck appears in the container ship rate data. We have seen some of the highest prices for container shipments, Puplava stated, at least over the last decade or so.

“These will be persistently high as we continue to work through this massive backlog to get inventories back to where they need to be,” Puplava said. “The pressure for purchasing commodities by manufacturers to produce goods and as well as the cost of shipping will remain high, which is why my view is that inflation will not be temporary in terms of the surge we're seeing. Actually, it will be persistent.”

U.S. Exports Set to Surge

Considering the recovery in Europe and Asia, we can expect further upward pressure on commodities and inflation in the U.S. as well.

Europe is seeing a surge in vaccinations, and is starting to open back up. The same is true for Japan.

As Europe opens up, it creates more market pressure on the U.S. manufacturing sector, because Europe is the third largest destination for U.S. exports.

The year-over-year rate of change of U.S. exports to Europe is still negative right now, Puplava noted, compared to a year ago. It is about 8 percent lower than last year, indicating low levels of exports to Europe.

We are likely to see a surge in exports in the months ahead as Europe opens up. Compounded with massive demand pressure from U.S. consumers for manufacturing goods, we're also going to see demand pressure from Europe spike at the same time.

Commercial bank lending growth will accelerate, giving the Fed room to step aside from emergency lending. Manufacturing companies have a massive backlog of orders, which they can show to banks to help secure loans.

Consumers are operating from a place of incredible strength in terms of their balance sheet and capacity to spend. This means we will likely see more banks lending to the consumer sector.

“The big takeaway here is that I wouldn't worry about the Fed reducing its balance sheet next year, which I think is highly likely because the banks will have a successful handoff taking over from the Fed,” Puplava said. “We’re still at record low levels of inventories. This will continue well into 2022 before we even come close to normal levels of inventories relative to sales. That will put continued pressure on manufacturing to produce durable and non-durable goods for the U.S. consumer as well as the world, which means there will be persistent demand for commodities to produce those goods. With that persistent demand for commodities, inflation will not be temporary. It will be persistent.”

For more information about this content or to find out more about our financial planning and asset management services, Contact Us or give us a call at (888) 486-3939.

Disclosures: Advisory services offered through Financial Sense® Advisors, Inc., a registered investment adviser. Securities offered through Financial Sense® Securities, Inc., Member FINRA/SIPC. DBA Financial Sense® Wealth Management. Indexes are not managed, and one cannot invest directly into an index. Past performance does not guarantee future results. The value of investments, as well any investment income, is not guaranteed and can fluctuate based on market conditions. Diversification does not assure a profit or protect against loss. Projections are for illustration purposes only and are not predictions of the performance of any investment or investment strategy. Investments in foreign securities involve certain risks that differ from the risks of investing in domestic securities. Adverse political, economic, social or other conditions in a foreign country may make the stocks of that country difficult or impossible to sell. It is more difficult to obtain reliable information about some foreign securities. The costs of investing in some foreign markets may be higher than investing in domestic markets. Investments in foreign securities also are subject to currency fluctuations. Investing in ETFs is subject to risk and potential loss of principal. There is no assurance or certainty that any investment or strategy will be successful in meeting its objectives. Before investing in an ETF, please consider the investment objectives, risks, charges and expenses.

Written by Ethan D. Mizer