There is absolutely no question that corporate profits in the current cycle have been stunningly spectacular. I have the feeling that if you’d have suggested to the investment community back in 2009 that corporate profits were getting ready to vault to all-time records, they would have thought you’d lost your mind. And, yet, here we are.

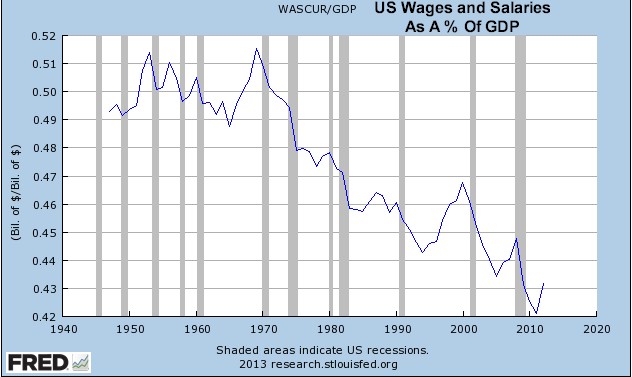

There are many reasons. Certainly corporations have gotten very lean and mean in the current cycle. They’ve found they can thrive with a lot less human bodies on board. The lackluster job market in the current cycle also means upward pressure on wages in the macro has been virtually non-existent. And this is necessarily reflected in the chart below where we’re looking at US wages and salaries as a percentage of GDP. Helping the corporate bottom line? You bet, and in a big way. In part, this is a reflection of the loss of manufacturing jobs (heavily unionized) and the rise of the service sector (largely union-less) really over a multi-decade time span. Each recession since 1970 has witnessed new lows in this relationship.

This circumstance of labor and wage dynamics in the current cycle is also clearly reflected in the chart of real median household income seen below. We’re now back to where we stood 17 years ago. Great for heightened corporate profits. Not so great for broad consumer demand longer term.

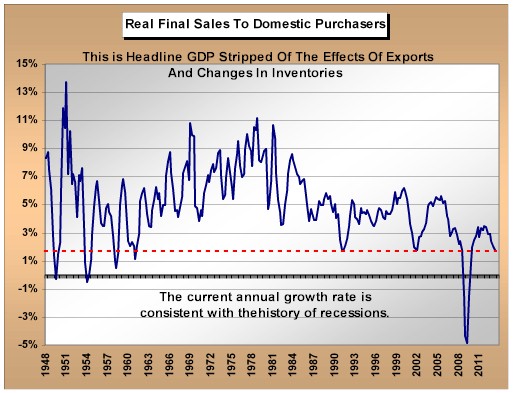

In fact, probably the most astounding accomplishment for growth in corporate profits in this cycle is that records have been set against the backdrop of one of the slowest macro domestic economic recoveries on record. Below is a quick look at the historical year over year rate of change in real final sales to domestic purchasers. Real final sales is simply GDP stripped of the influence of both exports and inventories. As you know, inventories heavily influenced the GDP number reported last week to the upside. The current one is the weakest cycle on record for domestic demand acceleration in a post-recessionary period.

Real final sales reflect more the corporate top line as opposed to bottom. Think revenues as opposed to earnings. I think it’s pretty darn safe to say that vibrant domestic revenue growth has been less the catalyst for corporate earnings growth in this cycle than has the combination of cost containment, reduced cost of debt capital, and the influence of monetary and fiscal stimulus. Corporations have been treated to once in a lifetime reduction in the cost of debt capital. The ability to refinance existing debt and knock substantial interest costs off of the P&L has been incredible, with results falling directly to the bottom line. Tangentially, we also know debt financed stock buybacks have propelled reported earnings per share, especially in 2013. Lastly, we need to think about just how much demand has been “brought forward” due to unprecedented stimulus in the current cycle. Federal debt has doubled since the fourth quarter of 2008 and we all know what has happened with the Fed’s explosive balance sheet. Without question these factors have likewise acted to support and propel earnings growth. We also know these unprecedented drivers are unsustainable in any longer term perspective.

We’re now coming into the end of what has been a spectacular year for the US equity markets. Yearend is filled with projections for what lies ahead. Double digit earnings growth expectations for 2014 fill prognosticator commentary. As you’ll remember, we also saw forward double-digit earnings growth expectations in each of the prior two years (late 2011 and 2012). But interestingly, the S&P has not recorded a double-digit year over year gain in operating earnings since the first quarter of 2011! In the seven quarters since, the rhythm of annual growth has been very subdued.

Below I’ve put together a chart that looks at the year over year change in S&P operating earnings numbers for this and the prior cycle (directly from S&P data). More than noticeable is that in the prior cycle leading up to the 2007 earnings peak, double digit gains were indeed the norm. Not so over close to the last two years of the current cycle. Growth rate rhythms are distinctly different. We’re still awaiting “escape velocity” as we have been for the prior few years.

Why bring all of this up? I think we need to intently focus on the character and quality of corporate earnings as we look into the new year. The equity market in 2013 has very much been a rising tide that has lifted many a boat in the macro. This is the fingerprint character of markets driven by valuation expansion as opposed to earnings expansion. Will it be the same in 2014 if current hopes of double digit earnings growth are again dashed, as has been the case in the prior two years? Analysts and individual companies play "beat the earnings expectations game" each quarter. They were playing exactly the same game as earnings peaked in 2007 and in the cycle prior to that. The market sure didn’t seem meaningfully overvalued in 2007 at the peak, of course under the assumption that double digit forward earnings gains would continue (which they did not).

While the world is focusing on the Fed, tapering, timing, etc., my suggestion to you looking into 2014 is to focus intently on macro and company-specific earnings characteristics. It’s really the following chart that compels me to suggest this, while POMO’s and volatility in cross currency relationships dominate shorter term market attention and behavior of the moment. I am not suggesting that a recession is in the offing at all, but what I believe important to keep in mind is that over the last six decades, US corporate profits as a percentage of GDP have consistently bottomed in the 4.5-5.5% range in each inevitable recession. There are no exceptions – nine out of nine. We now stand near 11%. Will the next recession cycle, whenever it arrives, be different? Will we break the 100% consistent rhythm of the last six decades and avoid the dreaded gravitational pull of reversion of the mean?

I do not mean this discussion to sound either pessimistic or predictive of an imminent corporate earnings downturn. Personally, I have no idea when earnings will peak in the current cycle. Rather, I hope it’s helpful to keep in mind and weight in our decision making the special circumstances of the current cycle driving earnings (cost containment, cost of debt capital, extraordinary and unsustainable domestic and global stimulus) and how the rhythm of earnings as a percentage of GDP can and has cycled consistently over time. In the first quarter of 2013, S&P operating earnings increased 6.3%, in 2Q the number was 3.7%. The final tally is not yet in, but we may be looking at a 2-3% number for 3Q. We’ll see. The markets got a bit of a free pass in 2013 as valuation expansion driven in good part by a narrow and almost obsessive perceptual focus on Fed balance sheet expansion was the key driver of price. But the Fed balance sheet expansion story is getting tired and equity valuations have moved back into historically rarified territory. Will the equity price drivers of 2013 again support price expansion in 2014 if double digit earnings growth expectations are dashed against the rocks of downward revisions for the third year in a row? I think it’s one of the most important questions looking into the new year.