Around this time each year the theme of the Great Rotation is dusted off and taken for a spin around the track by financial market pundits far and wide. Of course they are referring to the anticipated movement of capital from the bond market to the stock market. I’d like to briefly discuss an alternative version of the great rotation that is just a bit different than the mainstream theme, although clearly still involving the bond market. I believe one of the key issues facing the investment community looking into 2014 is the possibility for the further rotation upward of interest rates. In fact it just so happens that we find ourselves at quite the important juncture right now. Let’s face it, over our investment lifetimes the general level of interest rates has moved in generational fashion or cycles. Peak to trough and back again in interest rate cycles has been a journey of decades, not months or years. If that’s not a “great rotation” then I don’t know what is.

So, the tension has finally been broken, no? After hand wringing, voluminous Wall Street punditry, Fed sponsored guessing games, and another 200+ points upward on the S&P over the last six months, the heavens surrounding the Mariner S. Eccles building have parted and monetary tapering has finally begun. So now what? With diminished Fed support, are Treasury bonds destined for the investment dust heap and has the generational great rotation in interest rates upward begun?

The reason I’m asking these questions now is based on the reality of the current financial and economic cycle to date. Let me explain. First, we watched the equity market zoom skyward with the tapering announcement. We know this is a divergence in that the only equity market corrections of substance since 2009 have come when the Fed has stopped an interim QE program. Of course QE3 has not stopped, but we know financial markets anticipate. So for now, the equity market moving higher in what will be a decelerating QE environment is a divergence relative to what we’ve experienced over the past five years. This needs to be watched. What is hopefully different this time is that the Fed has now assured us the economy is getting better. The initial reaction is that the markets believe this, despite the dismal historical forecasting track record of the Fed. We know post each QE end in both 2010 and 2011, the economy did not subsequently attain “escape velocity”. Maybe this time will be different. We need to watch the character of the numbers. The 4.1% GDP revision last week was perhaps surprising to some, we just need to remember that when we strip out the influence of inventory accumulation and the recent revised upward increase in consumption 80+% due to energy and healthcare spending, adjusted GDP looks something more like 2+%. By the way, if I’m not incorrect, the total 3Q GDP revision from bottom to top was one of the largest on record. Sequestration headwinds will blow less violently in early 2014 so we do have the chance to put better GDP numbers on the scoreboard. We’ll just have to see what happens. So perhaps the first issue of note is an equity market moving higher in a decelerating QE environment. That’s not what has occurred 2009 to date.

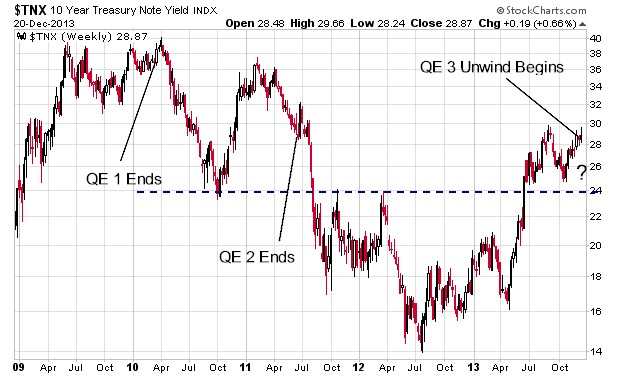

I’m convinced that interest rates are a key watch point as we move into the New Year. It’s here where we also need to watch for perhaps meaningful divergences relative to total cycle to date experience for a number of reasons. Let’s start with a very simple chart. Although it may sound counterintuitive, the reality of the current cycle is that interest rates have risen during each QE interlude and have fallen during QE cessation. The chart below could not be clearer.

So quite simplistically, where 10 year Treasury yields travel from here in the context of the total cycle to date experience will be important. Will interest rates move yet higher in a decelerating QE environment, in direct contrast with 2010 and 2011 experience? If so, it will be a very important divergence sure to influence investment outcomes in the year ahead. It will also suggest that we’ve begun the great rotation upward in the multi-decade movement of interest rate cycles. Alternatively, if interest rates were to decline from here, especially given the negative sentiment regarding bonds as of late, what would that suggest about the Fed seeing a better economy ahead? You know the numbers. A break above 3% for 10 year rates would be a multi-year higher high, suggesting yet further upward pressure. A break back below the approximate 2.4% level would probably cause investors to rethink the economic escape velocity theme. It will not be long until we know in which direction we are headed.

Maybe punctuating the importance of the juncture we’ve reached is a larger time frame window for the important benchmark that is the ten year yield seen below. We’ve once again come to the top of a declining series of yield level highs stretching back to the infamous peak of the financial markets in 2007. Both relative strength and MACD monthly numbers have also reached levels not seen since that time. Finally, from a longer term technical standpoint, ten year Treasury yields have spent very little time above their 50 month (200 week) moving average over the last two decades plus. This has been the very definition of the bond bull market. Moreover, this is the first trip above that important demarcation line over the entirety of QE so far.

The 50 month MA now becomes an additional demarcation line of importance. The monthly charts are very much about long term trends, so this one is important.

One last comment before concluding. The last time we saw current yields on the ten year as we see today, the US had about $2+ trillion less in total debt outstanding. Given what has happened to the US balance sheet since the dawn of 2009 coupled with complete lack of political will in terms of reconciling forward entitlement and broader Government spending, I’m personally convinced that when the generational cycle in interest rates turns, (and that may be right now), it will be as much about discounting the deterioration in the Government balance sheet as it will be about a better economy, rising inflationary pressures, etc. Watching rate movement short term is certainly a key exercise as we walk into 2014, but do not forget to keep tabs on longer term trends.

My very best wishes to you and your families for the Holiday Season, and here’s wishing you the best for health, happiness and prosperity (necessarily in that order) in the New Year.