I’ve written many a time over the past year about the directional dichotomy between the equity market and real economy. To be honest, this is old news. I’m personally convinced that what is most important to financial assets in the current moment is the weight and movement of global capital and the immediate “needs” of various pools of global capital. Strict fundamentals, for now, are not in the driver’s seat. You know the drumbeats have gotten a bit louder in recent weeks concerning a wealth and/or deposit “tax” to support the Euro banking system. And that’s not a catalyst for Euro capital to seek a safe(r) global haven? C’mon, this is exactly the kind of thing that sets global capital in motion. We know the pension fund community really globally is in serious need of reconciliation, but that’s not politically palatable near term so the hunt for rate of return intensifies and drives asset allocation behavior. It’s not so much where capital would like to go based on valuation metrics and fundamental investment opportunities, but rather where global capital has to go facing a reduced set of asset allocation choices (to achieve rate or return) and/or avoid confiscation/debasement possibilities. The set of circumstances that characterizes global capital will ultimately change, but for now this is where we are as we enter 2014. As always, we play the hand we are dealt as opposed to lamenting the hand we wish we had.

As we move into the New Year, I personally have a number of key watch points I believe will influence investment outcomes. A number of weeks back I wrote about interest rates. Obvious, but for now the doubling of 10 year Treasury yields over the last seven months have caused little to no blinking among equity investors. Surely the institutional crowd did not want to show their clients they were stupid enough to have been heavily long bonds in 2013, so yearend pressure was almost a guarantee. Yet so far into the New Year that pressure has not subsided, and this is with the Fed still conjuring up $75B (now) Yellen bucks each month. For now, someone is fighting the Fed — the US Treasury market!

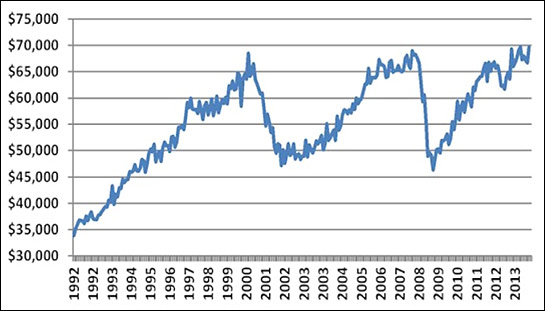

A second watch point I believe is important lies in the chart directly below. For the fun of it, have a look and ask yourself this question. Would you buy a breakout?

Although not a one for one match by any means, this chart looks a heck of a lot like the headline equity indices that are the Dow and S&P. Only difference being, for now there is barely a breakout in the above at all to the upside relative to the peaks of late 1999 and 2007.

Importantly, what we are looking at above is nondefense and nonaircraft new manufacturing orders. In other words, a key measure of corporate capital spending. And much like the headline equity indices, it is priced in nominal dollars. Although I will not drag you through another chart, on an inflation adjusted basis the 2007 and current peaks are successively lower than what was seen 14 years ago.

As a fingerprint character point of the current cycle, corporations have found more value in short term debt financed stock buyback arbitrage as opposed to expending corporate resources on capital/business expansion. And who could blame them? It has been great for earnings per share growth, but not so great for long term investment in plant and equipment (the investment quite necessary to truly increase longer term earnings capabilities).

You know that it’s now consensus thinking that US GDP will move higher into 2014 (it was also consensus thinking at YE 2011 and 2012). If there is even a modicum of efficiency in equity markets, values have moved ahead of this expected macro improvement, so in one sense this very much becomes a show me economy this year. I can think of no greater show of confidence by the corporate/business community in casting their vote as to whether we’ll achieve a better tone to the economy or not than an increase in capital spending. So I’d suggest to you that much like breakouts in stock charts so many folks are fixated upon these days, there are two chart breakouts to watch out for in 2014. The first is the one above. Will macro nominal dollar corporate capital spending break out to new highs or otherwise? A meaningful breakout would imply that at least in part equities were correct in 2013 to anticipate a higher level of economic activity this year.

Another important set of data to watch is small business capital spending. We all know that smaller businesses have had a much tougher time of it in the current cycle relative to their larger global brethren who have more easily partaken in global central bank(s) and government stimulus. Below we are looking at the NFIB survey of small business with data specific to their capital spending plans over the next three to six months. I’ve smoothed the data using a quarterly moving average to eliminate the very short term wiggles and jiggles in the numbers. What caught my eye in this data is that we are now close to, but not yet at, levels seen as the great recession began in late 2007/early 2008. So, the question becomes, will a break out to pre recessionary territory occur in 2014 for the small business community? An important question on many fronts as small business has lived through an extended dearth of capital investment throughout this entire cycle. We also need to remember that the small business community is the largest new jobs creator in the US. An increase in small biz capital spending would imply a better tone to hiring. A “breakout”, or otherwise, lays dead ahead. Keep an eye on this.

Why will corporate capital spending be important in 2014? As I’ve discussed in prior missives, I’m convinced residential real estate is in the midst of an investment cycle (again, capital seeking rate of return in a reduced set of asset class choices), not a normal economically driven housing cycle. As such, residential real estate construction is not going to meaningfully impact 2014 GDP outcomes. We’ll have a bit less of a drag fiscally as sequestration issues in 2014 are subdued relative to early 2013, but longer term we all know reconciliation in government spending has not yet even begun. Fiscal headwinds have been forestalled, not eliminated. And finally domestic consumption remains tepid. Not horrible, but tepid. The year over year change in real final sales to domestic purchasers (this is GDP excluding exports and inventories) looks recessionary compared to historical data, so it’s tough to expect a huge increase in discretionary personal consumption. That leaves corporate capital spending as a keynote potential incremental driver of near term GDP acceleration. I think it’s fair to say this is acceleration the equity markets have already priced in. And therein lays the risk management issue for equities ahead, again assuming fundamentals ultimately or even sporadically come into the equation.

Two more quick data sets to watch as we move forward. And wouldn’t you know it, yet another potential “breakout” possibility lies at our feet. Although we all know the US economy has become more service sector oriented over the prior half century, the level of capacity utilization throughout the economy is still an important watch point. Why? Look at the chart and think back to the first chart show in this discussion. Corporate capital spending in 2007 never surpassed what was seen in 1999. As you can see below, capacity utilization in the 2003-2007 economic cycle never went above the long term average for US capacity utilization. At least to me, it implies a meaningful question. Does corporate America not have an incentive to expand spending/investment if economy wide capacity utilization does not rise above roughly 80%? I suggest to you that question is again important right now as we approach that 80% level. In other words, why spend and expand if corporate America has 20% idle capacity? Does a “breakout” to prior levels of utilization that have been accompanied by much higher highs in capital spending relative to historical experience lay ahead?

Although we are not there by any means, another relationship of value over time has been watching the annual rate of change in capacity utilization. As you can see below, every recession over the recorded history of the capacity utilization data has occurred when the year over year change in this number dropped below zero. Importantly there are also four instances out of eleven where a recession did not occur, so a drop below zero is no guarantee of recession, but rather a warning shot.

If we are to experience better macroeconomic acceleration in the New Year, I cannot see how improved corporate capital spending will not be a meaningful part of the overall equation. At least as far as the real economy is concerned, would this be one of the most important “breakouts” of the New Year? In possibly aligning directionality between financial assets and the real economy, I believe this is exactly the case.