2011 was a volatile transitory year for most markets as the primary monetary concern shifted from asset inflation to asset deflation. Sentiment in gold and silver trended lower throughout the year as speculative positions were liquidated and money managers poured money into US government treasuries yielding record low interest rates both nominal and real. This trend can easily be seen in the underperformance of platinum, whose price has fallen below the price of gold despite the fact that it is 30 times more rare.

Gold has been up every year since its bull market began in 2001. Gold is the most stable of the precious metals. Takedowns are limited as central banks compete in bidding to accumulate it.

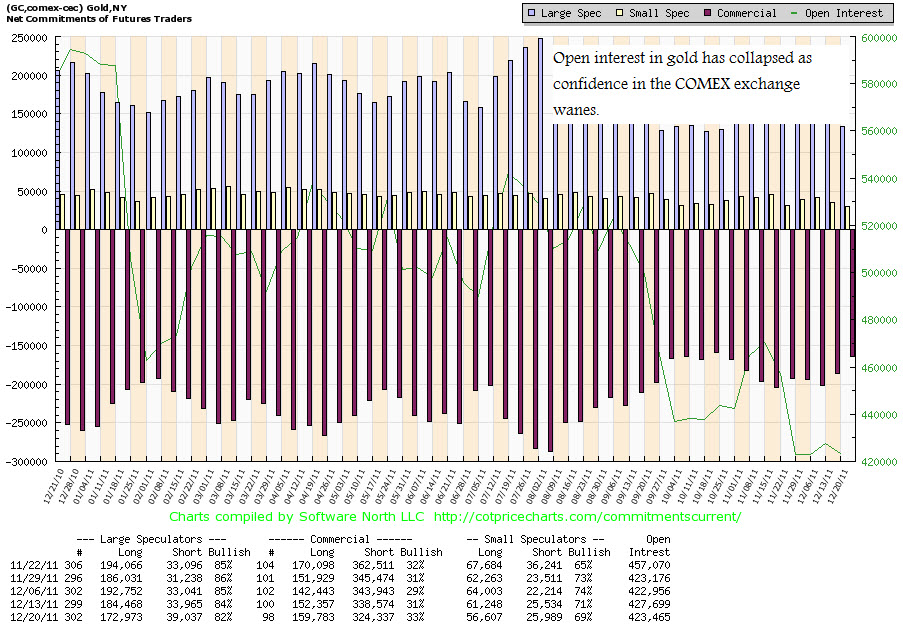

Silver had an intermediate top in the end up April, and suffered from several massive engineered hits. In addition, nearly 600,000 ounces of silver was stolen from small investors by MF Global, and transferred to JP Morgan. The result has been a collapse in open interest, as investors abandon the idea that paper silver can protect them from pending global hyperinflation. The default by the COMEX to protect investors using the exchange has proven that money invested in futures and even exchange allocated gold and silver is not safe.

As of last December 20th, the well documented net commercial short silver position was a mere 14,825. As we anticipated earlier this year, the commercial short banks have covered nearly all of their short position in the -32 range. They will soon convert to net long in anticipation of the next round of dollar devaluation.

Silver is not the only market that commercial traders have dominated. The commercial banks were massively short the Euro this spring prior to its collapse. Now that the collapse has occurred, commercial traders are now massively long the Euro as dumb money piles into the US dollar and treasuries that pay zero or even negative interest rates. The prevailing belief is that a further collapse of the Euro will lead to a deflationary crisis in which the US dollar trumps all assets. Commercial banks, which almost always win, are strongly betting against this belief as they pile into the Euro and precious metals.

While physically owned precious metals have held their value, leveraged speculators in futures and options have been demolished. If three-day takedowns and volatile price movements didn’t ruin them, outright theft of their assets from MF Global and the COMEX did. Silver and junior mining stocks suffered a similar fate and are now swinging in the desert wind. If mining itself wasn’t risky enough, 2011 proved that everything from government confiscation of mining assets, illegal shorting selling attacks, naked shorting, to outright theft qualify as categorical risks. Producing silver miners such as PAAS, SSRI, and SVM lost roughly half their value during the trading year. PAAS and SSRI were plagued by socialist policies of Argentina including new capital controls, and an illegal short selling scheme lead by an anonymous trader known Alfred Little attacked SVM. In the meanwhile actual earnings and cash flow for these companies grew at double and triple digits. The result has been a massive PE compression in which companies growing at double and triple digit rates now have PE ratios of less than 10 – which are based on the current low metals prices. Many of the miners are also using part of their cash flow to increase dividends and stock buy backs in addition to their operational expansion programs.

| PAAS | SSRI | SLW | SVM | AUY | |

| EPS | 2.68 | 0.03 | 1.63 | 0.56 | 0.98 |

| Revenue Est | 894M | 181M | 767M | 271M | 2.2B |

| Year Ago Revenue | 632M | 112M | 423M | 167M | 1.7B |

| 2012 Est | 3.11 | 1.06 | 2.43 | 0.72 | 1.27 |

| Price | 22.33 | 13.46 | 29.58 | 6.42 | 15.08 |

| PE | 8.33 | 448.67 | 18.15 | 11.46 | 15.39 |

| PE 2012 | 7.18 | 12.70 | 12.17 | 8.92 | 11.87 |

| YOY Earnings Growth | 16.04% | 3433.33% | 49.08% | 28.57% | 29.59% |

| PEG | 0.52 | 0.13 | 0.37 | 0.40 | 0.52 |

While the timing can’t be predicted, confidence in the global financial system continues to wane. Guaranteed negative interest rates for at least the next two years, also guarantees positive fundamentals for precious metals. Gold and silver are clearly in multi-month consolidations, which is natural given that they were the best performing assets of 2010. The inevitable further devaluation of global currencies will continue to facilitate a bullish environment for the metals. Investors with a long-term outlook have an excellent opportunity to accumulate gold, silver, and especially profitable dividend paying gold and silver producers that must increase by multiples to fulfill their potential value.