Heading into August the US stock market appeared to be holding up well and simply moving in a trading range. However, all was not well on the global scene. Back in June I wrote, “Global Monetary Tightening Taking Its Toll, Risks Mount.” A few of the things I highlighted were that several countries were experiencing inverted yield curves (short term interest rates above long term interest rates), which are often associated with bear markets and recessions. Those countries that did not have an inverted yield curve still had one that was sharply flattening out and at risk of inverting. I highlighted several global stock market leaders such as a few of the BRIC nations and commodity and economically-sensitive markets like Australia and Canada. While things were looking quite poor in June, they have only worsened as bear markets are springing up across the globe. Given the significant deterioration in market breadth in various national exchanges, it appears there will be more bear markets ahead, and here in the U.S. a bear market shot across the bow has occurred.

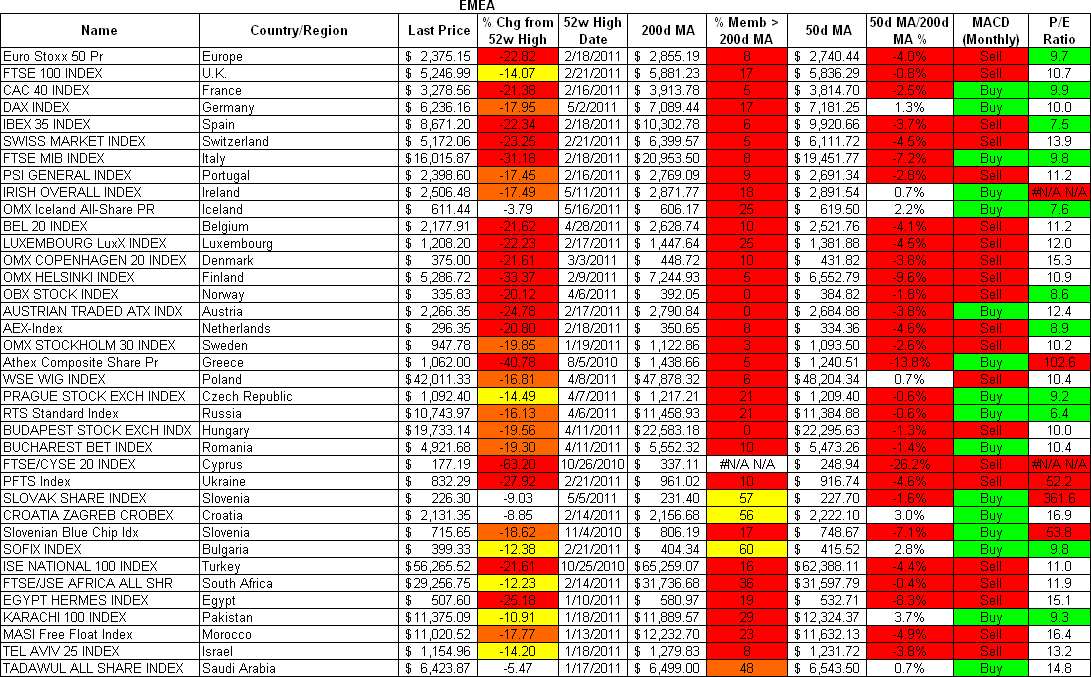

Nearly Half of Europe, Middle East, and Africa Have Had a Bear Market

Of the 37 national indexes I track in the EMEA region (Europe, Middle East, and Africa), nearly half have had a bear market decline of 20% or more. Those that have not are witnessing the percentage of their members above their key 200 day moving average (200d MA) at readings below 40%, which typically marks the lower threshold of a bull market. Readings below 40% for lows suggests bear market momentum is in effect as breadth has deteriorated to a significant degree. Thus, the other half of the EMEA region that is still in the “correction” category (> 10% sell off) are likely to witness a bear market after an oversold bounce. The good news is that these bear markets are producing single-digit price-to-earnings ratios (P/E Ratios) and allowing some value to creep back into the market. There are some opportunities, however, some stabilization is warranted first as it is never wise to try and catch a falling knife.

Source: Bloomberg

Click here for larger image

Looking at the Americas, we have had only one official bear market, which is Brazil, with the Bovespa declining nearly 28%. Looking at other markets in North and South America shows most are in correction status, though looking at the percentage of members above the 200d MA shows nearly all are in bear market territory (readings < 40%) and suggests Brazil will not be alone in experiencing a bear market this year.

Source: Bloomberg

Click here for larger image

Looking at the Asia Pacific region, there too is only one bear market, which is Vietnam, with the Ho Chi Minh Stock Index has fallen nearly 25%. While Asia has held up the best of all global regions, it too shows major deterioration in breadth as the vast majority of national stock index members are below their 200d MAs, and suggests more Asian bear markets to follow.

Source: Bloomberg

Click here for larger image

Bear Market Shot Across the Bow for the U.S.

Back in early July I mentioned we were still missing the key tip off to a bear market beginning in an article, “Bull or Bear Market? A Test of Character.” One aspect I mentioned was a lack of new 52-week lows on the U.S. exchanges and that we needed to see a spike in new lows exceed the prior spikes in new highs, with the 10% level a key threshold. We now have that as new lows have spiked on the NYSE to over 13% which also exceeds the recent spike in new highs seen in July. It now appears that the bears are in control and the chart damage is unmistakable as the 2009-2011 trend in the NYSE has been firmly broken.

While the July article highlighted that bear market warning signs weren’t flashing in the 52-week high/lows data, the article also mentioned the following:

“While the technical picture does not suggest a bull market peak is in, there are still many headwinds that pose risk to the market and economy and may eventually prove too much for the bulls to contend with, which is why I remain cautious at this time…

These risks are being overshadowed today as the bulls argue the current weakness in the economy was only temporary as seen by a rising ISM Manufacturing Index for June. However, a temporary uptick in the ISM Manufacturing Index was to be expected as both our Monetary Flow Indicator and sector relative performance numbers were suggesting. The key is what comes next as both indicators suggest the ISM Manufacturing Index declines for the remainder of the year, falling below the key 50 level which would indicate a contracting economy.”

According to the indicators above, the economy is going to continue to decline into year end, which is why an oversold bounce ahead in the markets from deeply oversold conditions is likely to be a dead cat bounce. The bears are now in control, and it will have to take monetary and governmental authorities to steer things around as the economy continues to decelerate into year end.