Obviously, whenever you have conflicting market messages regarding the same situation someone is right and someone is wrong. When the discrepancy gets resolved the markets often then trend in a more or less straight fashion, whether up or down. The markets have been in a trading range as bearish and bullish messages duked it out and a winner has finally emerged. The big conflicting messages that I’ve had my eye on for some time are the credit markets and equity markets, and, whether you believe it or not, right now they're singing a bullish harmony.

The Equity Markets Had It Right

After the US received its first credit downgrade by a ratings agency in August, the S&P 500 essentially traded sideways and put in a final low in October 2011. Using a 20% move to define bull and bear markets, the S&P 500 has entered a new cyclical bull market by rallying more than 20% off the October lows. Since October the stock market has rallied sharply and yet the credit markets were not giving the all-clear signal, which made the equity rally suspect and it could have easily been a strong bear market bounce. It was this conflicting message of a strong stock market rally and yet worsening credit spreads that had me cautious in the last two months of 2011 as seen in the following articles:

- Could Credit Markets Kill a Fledgling US Economic Recovery? (11/18/2011)

- Message from the Credit Markets, “We Ain’t Buying It!” (11/23/2011)

- Credit Spreads Cast Doubt on Sustained Market Rally (12/15/2011)

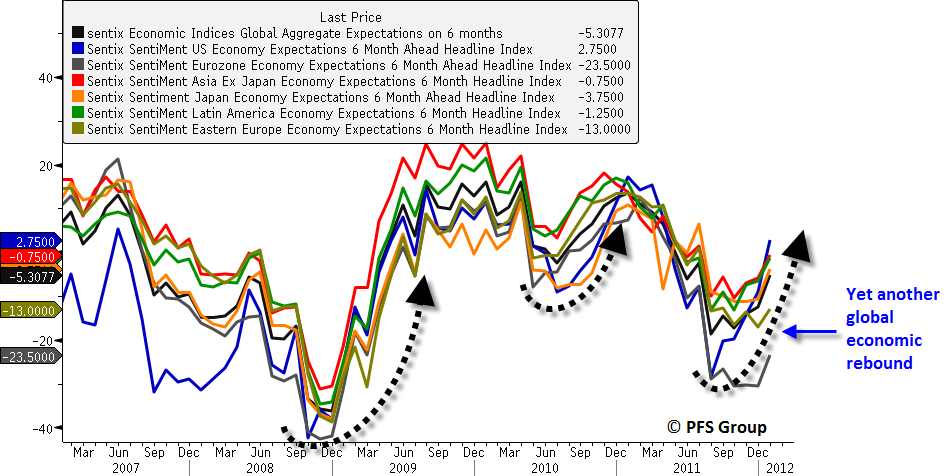

Over the last month financial market stress has begun to ease due to an improving US and global economic backdrop. Easing financial stress has led to a drop in various credit spreads that measure liquidity risk, counter-party risk, and overall market stress. While many can recognize clear improvement in the U.S., it is not the only economy experiencing recovery. As seen below in the Sentix Sentiment Economy Expectations Indices, every single economic region across the globe is seeing improvement after bottoming late in the summer to early fall 2011. This global recovery is similar to what we saw in late 2008 and mid 2010, and in both circumstances we witnessed strong equity markets.

It is perplexing to many investors as to how the markets can be rallying while the debt situation in Europe and the US remains unaddressed. These investors are entirely correct: the debt issues have largely been unaddressed but that is only half the equation. While debt levels remain constant, what is more in flux are revenues that are used to service the debt.

The great periods of market and credit weakness over the last few years have always coincided with economic downturns. When economies roll over tax revenues dry up, which makes it more difficult to service their debts. Ultimately, this leads to credit market stress and, as we're seeing now, fears of default. Conversely, when economies recover tax receipts increase which makes it easier to service public debt and default risk declines. Thus, with the current economic bounce globally since the late 2011 trough we’ve seen credit spreads begin to decline as incoming tax receipts begin to rise.

Disinflationary Stimulus Being Felt

Francois Trahan, voted top Wall Street Institutional Investment Analyst in four of the last six years, has noted that with zero-bound interest rates, inflation has become the new Fed Funds rate.

Recommended listening: Francois Trahan, Co-author of “The Era of Uncertainty: Global Investment Strategies for Inflation, Deflation, and the Middle Ground”

What that means is that rising inflation is akin to rising interest rates, with both dampening economic activity. Conversely, falling inflation levels is similar to a decline in interest rates that often leads to an economic recovery. The lead time between inflationary levels and economic activity is roughly six months.

It was the peak in inflation indicators back in Q1 and Q2 that led Francois Trahan to call for an economic contraction and to make a defensive portfolio call as he expected economic activity would decline for the following six months. While rising inflationary pressures heading into 2011 signaled economic activity was set to weaken six months down the road, likewise a decline in inflationary pressures since the spring of 2011 suggested a rebound beginning late in 2012. This concept was shown visually in an article back in October (A Window of Opportunity) with the image shown below.

This function of inflation acting to cool an economy and disinflation acting as an economic stimulant has not only been witnessed in the U.S. but also globally. Below is the Sentix Economic Global Expectations Index and the US ISM Prices Paid Index (red line) to serve as a proxy for global prices paid and shown inverted for directional similarity. The peak in inflation as seen by a falling Prices Paid Index (again, shown inverted below) predicts a global economic recovery into mid 2012. As the Prices Paid Index has begun to rise again (fall in chart), we may see another round of economic weakness and rising credit stress mid 2012 just as we did in 2010 and 2011.

Equity Markets May Accelerate Higher as Credit Markets Ease

Since 2008 we have witnessed three periods of rising financial stress and economic weakness. The first was in 2008, the second episode was in 2010, and the third came in 2011. Notice the three spikes in U.S. credit markets (top panel) and European (lower panel) below.

As you can see, on average the equity and credit markets act in sync—when tensions rise, stocks fall; when tensions ease, stocks rise. It doesn't get any more basic than this. Currently, tensions appear to be easing up again both in the U.S. and in Europe, which, if sustained, will give stocks room to breathe moving forward.

It’s Not the News but the Market’s REACTION to The News that Matters

Investors get paid on the margin, meaning markets react to surprises and not widely accepted information. For example, if a company was expected to see earnings rise 10% from the prior quarter and the actual growth comes in at 10%, the stock is not likely to move.

A perfect example of the market only moving due to surprises comes from the top article on Yahoo Finance (highlighted below). France lost its AAA credit rating and yet the markets yawned today, not what you would expect based on the headline, but again, it’s only new news that the market responds to as the market already expected France to lose its AAA credit rating by one notch. However, if France’s rating was cut TWO notches that would likely have moved the markets significantly.

Market Resiliency Shines Through French Rating Cut

Stocks closed out this Friday the 13th modestly lower despite some significant downside events. The Dow Jones Industrial Average fell 0.39% to 12,422, the S&P 500 fell 0.49% to 1,289, and the Nasdaq fell 0.51% to 2,710.

"To move the market, you must surprise the market" a wise Wall Street veteran once told me. To his credit, that simple adage stands the test of time and today was no exception.

Not long after the market opened lower this morning and was trying to quantify the disappointment of JP Morgan's (JPM) fourth quarter earning results, a swirl of headlines began to circulate about possible credit rating cuts across the Euro Zone that briefly spooked the market. Briefly, until traders recalled that they had already seen this movie, because once they did it was on to other things

Bravo, Wall Street. How rational you have become.

Don't get me wrong, I am not trying to minimize the impact and ramification that the downgrades will have on the citizens and institution of the effected countries, I am simply saying that it was well telegraphed and therefore, not a surprise, and thus, not a market-moving event.

Had Germany been unexpectedly stripped of it's AAA-rating however, that would have been an entirely different matter. But for S&P to take aim at the credit worthiness of France, Italy, Spain or Portugal, the only question being asked is ''what took so long?"

Instead, we have been allowed to stick with our existing narrative which is the presumption that Europe's problems are, at the least, not worsening. As a result, traders can continue to bid up stocks, just as they have been for the past three weeks.

The equity markets already discounted a great deal of bad news as seen by today’s tepid reaction, and with easing in the credit markets and continued economic improvement seen globally, we are likely to be treated to a favorable period for equities over the next several months as the prior disinflationary stimulus from 2011 is being felt. When inflationary levels begin to accelerate once more the clock will begin ticking its 6-month window for when the next economic downturn will occur, and with it the next big market selloff.

To gain a better understanding of how trends in inflation have now become one of the biggest economic and market moving factors, I would highly recommend you read Francois Trahan’s book, “The Era of Uncertainty: Global Investment Strategies for Inflation, Deflation, and the Middle Ground.” For a Cliff Notes version you can listen to Francois recent interview on FSN with a link provided below.