Summary

- We haven’t dealt with the Euro crisis since 2012

- The picture in Europe has worsened as debt levels continue to rise

- European growth to slow into 2015, leading to another possible crisis

The most important aspect about the markets that one should never lose sight of is the involvement of millions and millions of human beings whose collective decisions of buying and selling move the markets. Their decisions are often based upon emotions, with the two biggest emotions that dominate our thinking being fear and greed. This is one reason why we experience huge swings in the market as investors and economists oscillate along the emotional spectrum from one extreme to the other.

For this reason it’s always important when things look great to ask, “What could go wrong?” And when things are gloomy to ask, “What could go right?” With the markets surging to new all-time highs, now is as good a time as ever to start asking “What could go wrong?”

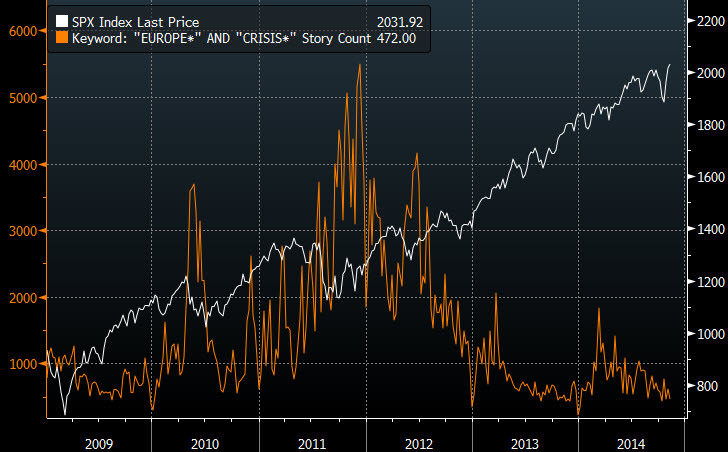

Chief among market risks in my mind stems from across the Atlantic over in the Eurozone. The financial crisis in Europe in 2010, 2011, and 2012 played a significant role in the declines of the stock market during those years as seen by the figure below, which shows the S&P 500 in white and a keyword search for “Europe” and “crisis” in orange. The peak of the Euro crisis occurred in 2011 and was quickly extinguished when the European Central Bank’s (ECB) balance sheet expanded from roughly two trillion Euros to three trillion. There was a smaller scare in 2012 but since 2011 fears of a European crisis have subsided.

Source: Bloomberg

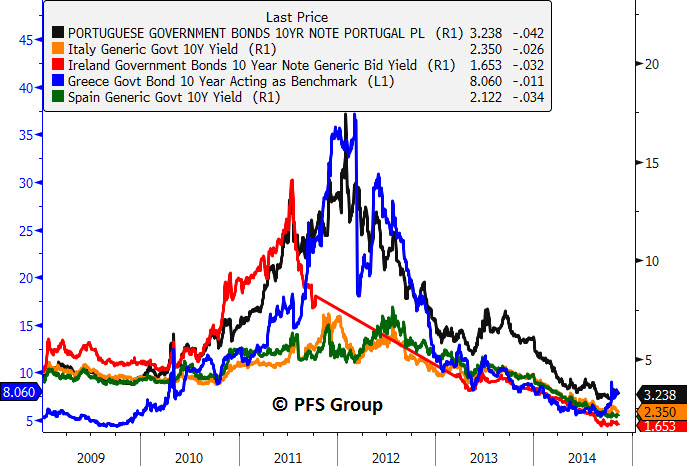

Not only have news references to a Eurozone crisis subsided but so too have 10-yr bond yields in the PIIGS countries (Portugal, Italy, Ireland, Greece, Spain), which peaked in 2011-2012 and have collapsed over the last few years.

Source: Bloomberg

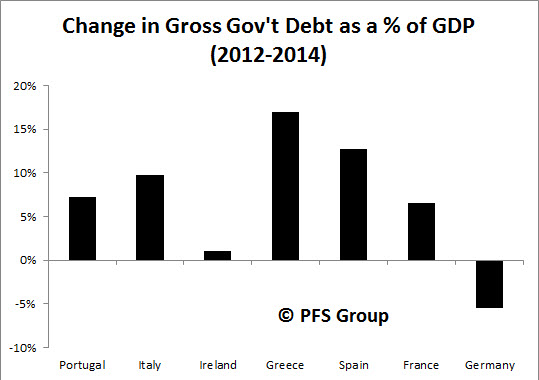

While bond investors may have been lulled into complacency since 2011 based on ECB actions, they would be wise to awaken from their slumber as risks from Europe are even larger today than several years ago. Government debt as a percentage of Gross Domestic Product (GDP) has grown since 2012 with only Germany showing a contraction.

Data Source: IMF

Both Greece and Spain have seen their debt to GDP levels rise the largest with Italy and Spain not too far behind.

Data Source: IMF

This increase in government debt relative to GDP occurred despite austerity measures as government expenditures have been declining over the last few years. Shown below are government expenditures for select European governments normalized to 100 in 2000. The debt growth also occurred even when sovereign bond yields collapsed and with it debt servicing costs.

Source: Bloomberg

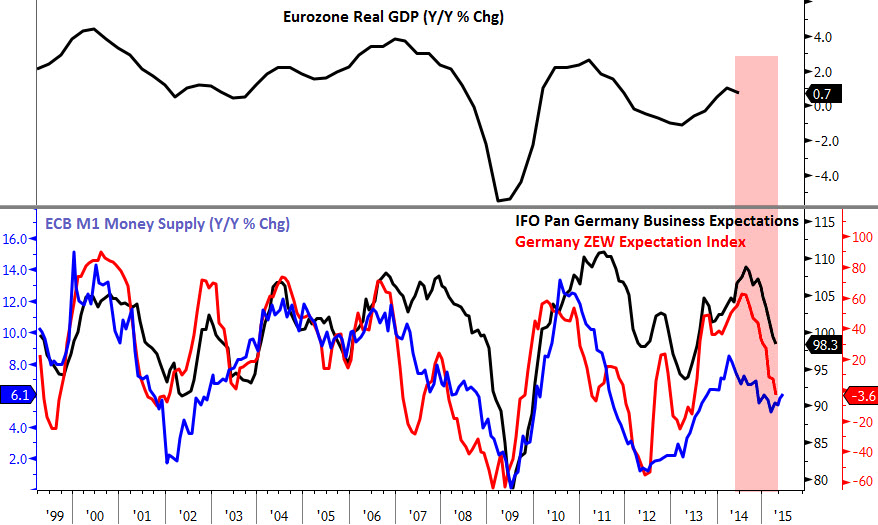

The reason for the continued erosion in the region's financial position despite a cutback in spending comes from a poor economy. When households in Europe cut back on spending, as does the government, there is no one left to pick up the growth baton and overall economic activity decelerates even faster than the cutback in spending. This is what has happened since Eurozone GDP growth peaked in 2011 at 2.6% and fell into negative territory in 2012 and 2013. While Eurozone GDP began to improve in 2014, it reached only a meager 1% growth rate and now looks to be rolling over as the leading economic indicators suggested and will likely continue to fall well into 2015 (red shaded region below).

Source: Bloomberg

This is the last thing Europe wants and is what the head of the world’s largest hedge fund, Ray Dalio of Bridgewater, calls an “ugly deflationary deleveraging” and stands in complete contrast to what Ray Dalio says the U.S. has been experiencing: a “beautiful deleveraging” (see Dalio’s, “An In-Depth Look at Deleveragings”).

In a beautiful deleveraging a country’s central bank prints enough money to offset the deflationary forces of debt reduction and austerity. Currently, GDP growth is well above nominal interest rates and we see a fall in debt to income ratios. In an ugly deflationary deleveraging there is not enough money printed to offset the deflationary forces and GDP growth is below nominal interest rates. Dalio shows two cases of the US undergoing a “beautiful deleveraging,” which was between 1933-1937 and March 2009 to the present.

Source: Bridgewater, An In-Depth Look at Deleveragings

Shown below is a look at nominal GDP growth rates and 10-yr government interest rates in both the US and Europe. You can see that for much of 2008 and 2009 the U.S. and Europe experienced an ugly deflationary deleveraging but both the Fed and the ECB significantly expanded their balance sheets to stimulate economic growth with GDP in both countries rising above long-term interest rates in 2010. However, economic growth in Europe slowed due to fiscal austerity and as the ECB began in 2012 to unwind the 50% increase in its balance sheet that occurred beginning in 2011, Europe fell back into an ugly deflationary deleveraging with GDP falling back below long-term interest rates. However, with Ben Bernanke at the helm and several rounds of money printing to offset deflationary forces, U.S. GDP has consistently stayed above nominal interest rates as the U.S. stayed on the beautiful deleveraging path.

Source: Bloomberg

Another dynamic Ray Dalio notes of beautiful deleveragings is that debt to income ratios fall. This is exactly what has occurred in the U.S. over the last few years while most of Europe has seen little to no progress on this front. Shown below are household debt to GDP ratios for the U.S. and parts of Europe normalized to 100 as of 2010. You can see that the U.S. has seen nearly a 15% decline in household debt to GDP levels while Greece has seen nearly a 30% growth rate and France is up by 7%.

Source: Bloomberg

What is of grave concern and why we could have another round of the ongoing Eurozone crisis saga is that leading economic indicators for Europe suggest Eurozone GDP has peaked and is likely to continue to fall heading into the middle of next year. Decelerating economic growth is the time you should worry about high debt levels as the ability to service the debt diminishes with lower government revenue. As such, default risk picks up. This can be seen below when looking at the leading economic indicator (LEI) for Europe along with my PIGS credit default swap (CDS) composite. Typically credit defaults swaps rise when economic growth slows and falls when growth picks up. If we are to see European economic growth slow heading into 2015 we are likely to see a pickup in default risk for European periphery countries and it appears European stock markets are already discounting this.

Source: Bloomberg

When the Eurozone crisis was full blown in 2011 the percentage of stocks in the Euro Stoxx 50 Index hitting 52-week lows surged to nearly 80% and kicked off a brutal bear market and a two-year trendline was broken. This was also a similar setup that occurred in 2007 when 52-week lows surged well north of 50% and a crucial trendline was broken. Fast forward to today and we see yet another crucial trendline was broken and 52-week lows exploded to north of 50%.

Source: Bloomberg

What investors need to pay critical attention to is how European equities act in the weeks ahead as it looks like a meaningful top was put in this summer and we are rallying up to the underside of the broken trendline that goes back to 2012. Should European equities fail and continue to head south, the U.S. market may get pulled down with it despite bullish seasonal tendencies into year-end. This has been the script since 2010 when European equities failed to confirm the move in the S&P 500 and eventually they pulled down U.S. stocks in 2010 and 2011. Currently the divergence between the two regions is the biggest divergence since 2011 and, as highlighted below, divergences between the two are times to focus on risk management.

Source: Bloomberg

Conclusion

Given the relative freedom the U.S. Fed has over the ECB it has been able to be more aggressive in combating deflationary forces that have been in place since the financial crisis of 2008. Former Fed Chairman Ben Bernanke was like the fable "Goldilocks and the Three Bears" in that he was able to print just enough money so that the economic porridge was not too hot nor too cold and navigated what Ray Dalio calls a beautiful deleveraging. Debt to income levels have come down and economic growth has stayed above long-term interest rates while inflation has stayed contained. Not so across the pond as the ECB has not stayed ahead of the deflationary curve, experiencing what Dalio calls an ugly deflationary deleveraging. When we’ve seen European growth falter we also tend to see sovereign default risk pickup, which has led to several rounds of the Eurozone sovereign debt crisis.

Given European growth is expected to decline well into 2015 we are likely to see another round of the Euro crisis occur which could derail strong bullish seasonal strength the U.S. market typically sees in the last two months of the year. It appears European equities may already be discounting this fear as European stocks hitting new 1-year lows have surged to levels associated with bear markets and credit default swaps on PIGS country debt are rising again. While things look rosy in the U.S. with our markets hitting new all-time highs, investors would be wise to keep a watchful eye on our friends across the Atlantic.