Various employment data shows continued improvement in the U.S., helping to support higher stock prices with the perception of economic recovery. As long as the employment situation continues to improve and recession risk remains low, US stock prices are likely heading higher.

Employment Data Confirming New Highs

Perhaps one of the best leading indicators for the economy out there is the jobless claims data. It is reported every week so we are continually treated with a real-time leading indicator for the economy. It is well known that the stock market itself is a leading indicator and so both jobless claims and the stock market tend to track each other. Watching for divergences in both series can help one navigate when we may be reaching an economic turning point.

Shown below is the 1-month moving average for jobless claims (red line, inverted) with the S&P 500 (black line). As you can see, in the middle of 2007 jobless claims stopped falling and began rising and actually failed to confirm the stock market’s October 2007 new high indicating the market was on weak footing. Conversely, both the S&P 500 and jobless claims signaled the end of the 2007 recession when they changed course in early 2009. It is encouraging that the new high in the S&P 500 is being confirmed by a new low in jobless claims (blue box).

Source: Bloomberg

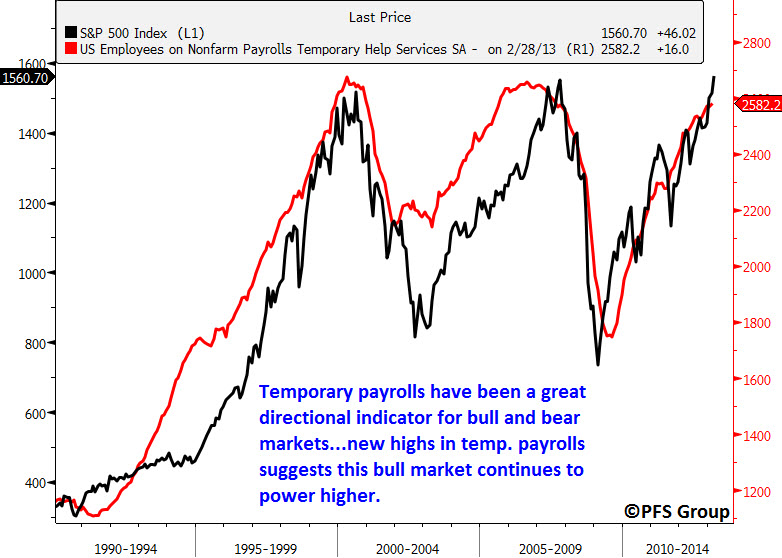

Another employment indicator that has had a great track record of catching bull and bear market swings is temporary payroll levels. Peaks in temporary payrolls often coincide with bull market tops while troughs in payrolls coincide with bear market bottoms. Like jobless claims, the new high in the S&P 500 is being currently confirmed by temporary payrolls and has yet to show signs of a major reversal.

Source: Bloomberg

Leading Employment Indicators Suggest New Highs Ahead

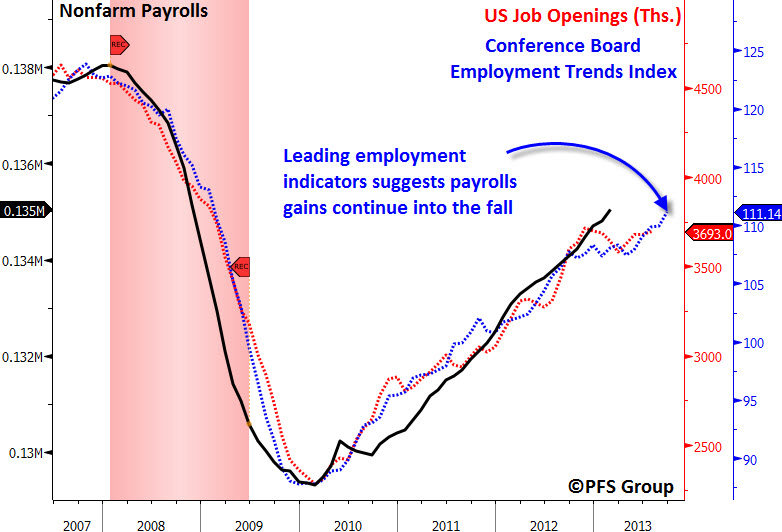

While general employment indicators are confirming the markets move higher, leading employment indicators suggest continued payroll gains ahead and, thus, higher stock prices. Shown below are two indicators, US Job Openings and the Conference Board Employment Trends Index, that both suggest payrolls continue to climb heading into early October.

Source: Bloomberg

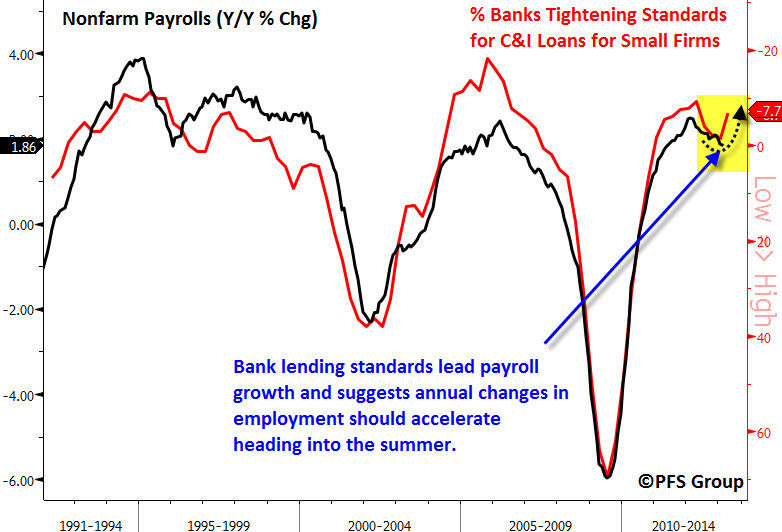

Another leading employment indicator is the Fed’s Senior Loan Officer Survey in which it measures the percentage of banks tightening lending standards for Commercial and Industrial (C&I) loans to small firms. The survey leads employment growth by one quarter and suggests that payroll growth accelerates from present levels heading into the summer.

Source: Bloomberg

Low Recession Risks Imply Low Probability of Bull Market Top

Another useful way of analyzing jobless claims is to take the smoothed annualized growth rate in which readings north of 15% have often been associated with recessions (shaded red regions). As long as recession risks remain low and central bank policy remains accommodative, the path of least resistance for the stock market appears higher.

Source: Bloomberg