We are in a precarious position with the current credit crisis precipitated by the subprime mess. To see how the tentacles of the housing recession are spreading into the economy and financial markets and how serious things are, take a look at some of the headlines from this week alone.

Lowe's Lowers Outlook (08/20/07)

Despite the housing crunch, Lowe's smashed Wall Street's expectations in the second quarter. Bracing for tough times ahead, America's second-largest home improvement chain also lowered its full-year outlook on Monday.

Despite the strong quarter, management slashed its forecast for 2007, citing weakness in the housing market. Lowe's said it expects to earn $1.97 to $2.01 a share, down 2 cents from its previous range of $1.99 to $2.03.

Capital One to Close Wholesale Mortgage Unit; Charges Will Total $860M (08/20/07)

The company, which said about 1,900 positions will be eliminated due to the closing of the unit, added that it will "cease residential mortgage origination" at the unit, called GreenPoint Mortgage, effective immediately.

Countrywide Cuts 500 Mortgage Jobs (08/20/07)

Countrywide Financial Corp., the nation's largest mortgage lender, said Monday it has eliminated about 500 jobs as it tries to ride out problems from a credit crunch that has rocked the home loan industry.

Bank warning intensifies German disquiet (08/21/07)

The uncertainty gripping Germany's banks intensified Tuesday after the chief executive of one of its leading lenders issued an unusually frank warning about the troubled state of the country's banking industry.

"We sense in the markets that the readiness of foreign banks to extend credit lines to German banks has become difficult," said Alexander Stuhlmann, chief executive of WestLB, the state-backed Dusseldorf-based Landesbank.

The country's lenders were in a "not uncritical situation", he added.

The comments came only days after a second German bank, Sachsen LB, had to be rescued after falling victim to exposure to the turmoil in the global credit markets.

The remarks added to perceptions that banks in Germany were particularly vulnerable.

July Foreclosures Up 93% From July 2006 (08/21/07)

The number of foreclosure filings reported in the US last month jumped 93 percent from July of 2006 and rose 9 percent from June, the latest sign that homeowners are having trouble making payments and finding buyers during the national housing downturn.

There were 179,599 foreclosure filings reported during July, up from 92,845 during the same period a year ago, Irvine-based RealtyTrac Inc. said Tuesday. There were 164,644 foreclosure filings reported in June.

The national foreclosure rate in July was one filing for every 693 households, the company said.

Loan types seeing higher delinquencies and defaults in general are home equity loans or second mortgages used to cover a down payment, subprime loans to people with shaky credit histories, and Alt-A loans, which can include interest-only and adjustable rate mortgages sold with little or no documentation.

ABC News/Washington Post Consumer Comfort Index (08/21/07)

The turmoil in global financial markets and concerns of a credit crunch are infecting consumer sentiment. Consumer confidence fell nine points to -20 in the week ending August 19, according to the ABC News/Washington Post consumer comfort index. The latest decline is the largest week-to-week drop on record and puts the index at its lowest level since the aftermath of Hurricane Katrina.

Accredited Home Lenders Shuts Down Much of Its Business Amid Mortgage Turmoil (08/22/07)

Accredited Home Lenders Holding Co. plans to shut down most of its business to survive the troubles in the home lending industry, the company said Wednesday.

Accredited Home Lenders said it will cut its work force to 1,000 people -- from 2,600 at the end of June -- and close 65 branches. The company will immediately stop accepting applications for home loans in the US, though it will honor the loans it has already committed to finance.

Stung by decaying credit quality and a newfound fear of risk on Wall Street, mortgage lenders across the industry have struggled to raise cash this year.

More than 50 lenders have gone bankrupt this year, including two of the nation's 10 biggest.

Toll Bros. Third-Quarter Profit Drops on Hefty Writedowns, Cancellations (08/22/07)

Luxury homebuilder Toll Brothers Inc. said Wednesday its third-quarter profit tumbled, hurt by hefty writedowns and higher-than-expected cancellations as the housing downturn and credit quality concerns continue.

Robert Toll, chairman and chief executive, said cancellation rates for the quarter were greater than at any point in the 21 years the company has been traded publicly.

Toll Brothers said its quarterly cancellation rate was 23.8 percent, compared with 18.9 percent in the previous quarter.

Lehman Brothers Amputates Mortgage Arm (08/22/07)

The New York investment bank will cut 1,200 positions in 23 locations as a result of the closing of BNC Mortgage. It will take an after-tax charge of $25 million and a goodwill write-down of $27 million, it said.

Lehman said that poor market conditions in the mortgage space of late have "necessitated a substantial reduction in its resources and capacity in the subprime space," according to a release.

Consumer Fallout

The housing recession has contributed negatively to economic growth for several quarters now as the housing recession is ongoing. What makes the current environment troubling is that all this mess is happening when the rate resets for the explosion in exotic mortgages that took off in 2004 haven't even peaked yet. If this is the fallout when adjustable-rate mortgages haven't peaked yet, what will be the fallout when they eventually do?

Figure 1

Source: Moody's Economy.com, DismalScientist

Figure 2

Source: Moody's Economy.com, DismalScientist

Figure 3

Source: Moody's Economy.com, DismalScientist

The fallout in employment from the housing recession is being especially felt by mortgage brokers that were pushing risky mortgages homeowners couldn't afford. Mortgage loan broker employment has plunged into negative territory along with the negative growth rate in new single-family homes. Mortgage broker employment has been coincident with previous housing bottoms and the lack of a clear turnaround in mortgage broker employment indicates the housing recession will be ongoing.

Figure 4

Source: Moody's Economy.com

Housing is a leading indicator for economic activity and so it's not surprising to see mortgage employment turn south ahead of total employment. Another leading indicator in total employment is temporary employment as temporary employees are the first to go as businesses slow down and the first to be hired when an economic rebound is uncertain. Temporary employment is also in negative territory and like mortgage broker employment, the lack of a turnaround in its trend implicates a weakening labor market ahead.

Figure 5

Source: Moody's Economy.com

As mentioned in previous market observations, businesses are cutting back on their demand for loans as we see the consumer retrench. The deceleration in business appetite for commercial and industrial loans (C&I) often heralds economic weakness as it did in the 1990 and 2001 recessions. The fact that the percent of banks reporting stronger demand for C&I loans has fallen into negative territory is not an encouraging sign, as this was seen at the onset of the 2001 recession.

Figure 6

Source: Moody's Economy.com

As businesses take their cue from the consumer, it appears that the Fed takes its cue from businesses. A close positive correlation in trend can be seen with the Federal Funds Rate and business demand for C&I loans with business C&I loan demand leading the trend in the Fed Funds Rate by 15 months, signaling significant rate cutting ahead, down to roughly 3%.

Then and Now

It's been said that the Fed raises interest rates until something breaks. That break has been subprime mortgages and securities backed by these mortgages. That business demand for C&I loans is signaling a significant rate cut by the Fed directly ahead (Figure 6) is not an encouraging sign despite what Wall Street would have investors believe.

Significant rate cuts by the Fed have occurred just prior to or in the midst of a recession with the 1984/1985 mid-cycle slow down proving the only exception. An aggressive rate cutting program by the Fed would indicate a likely recession in the not too distant future.

Figure 7

Source: Moody's Economy.com

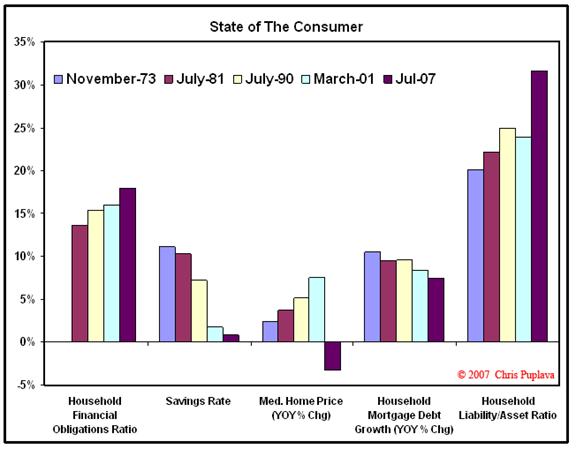

If the US does slip into a recession ahead, it will do doing so on some of the worst fundamentals compared to where it stood at the start of prior recessions with the same for the US consumer.

Four economic indicators are highlighted below for the start of the last four recessions and the present condition. What is clearly visible is the weakening trend in each indicator. Notably, income growth and retail sales growth were abnormally high heading into the 1973 and 1981 recessions as a result of widespread inflation seen in wages and products.

Current income growth is roughly on par with the levels in the least two recessions as is employment growth, though employment growth is currently skewed due to the birth/death model adjustment and is likely much weaker (Figure 7 & 8, 07/11/07).

Figure 8

Data Source: Moody's Economy.com

Overall, current economic conditions are either worse or on par with economic levels seen in the last four recessions, though the state of the consumer is more worrisome. In every single category the US consumer is worse off now than where it stood at the start of the last four recessions: record high financial obligations ratio, record low savings rate, sharply declining home prices, lowest mortgage debt growth, and the highest liability to asset ratio ever.

Figure 9

Data Source: Moody's Economy.com

As mentioned above, the US consumer is currently worse off now then at the last four recessions. How did the US consumer get here? The answer lies in the consumer's insatiable appetite for debt-fueled consumption. This increase in debt taken on by the consumer has propelled the consumer's importance (personal consumption expenditures and residential fixed investment) to GDP from 64% in 1967 to 75% currently.

Figure 10

Source: Moody's Economy.com

This appetite for debt over the last half century has driven the position of the US consumer to its worst point ever. The charts below need no introduction as they speak for themselves, all near record territories and uncharted waters.

Figure 11

Source: Moody's Economy.com

Figure 12

Source: Moody's Economy.com

Figure 13

Source: Moody's Economy.com

Figure 14

Source: Moody's Economy.com

* Cash includes bank deposits and credit market assets

Figure 15

Source: Moody's Economy.com

If the US does slip into a recession, it will need a massive bailout by the Fed with rampant money printing and greatly reduced interest rates just as they did to dampen the effects of the 2001 recession. However, this time around the consumer is much more financially tapped out than in 2001 and the Fed might have to become more creative and aggressive in their efforts to save the markets and economy then they have so far.

Today's Market

The markets rose today as investor anxiety calmed with a pullback seen in Treasuries and an increase in bank borrowing. The markets jumped upwards out of the gates in early morning trading before staying range bound for the remainder of the session. The Dow gained 145.27 points to close at 13236.13 (+1.11%), the S&P 500 rose 16.95 points (+1.17%) to close at 1464.07, with the NASDAQ closing at 2552.80, up 31.50 points (+1.25%).

Treasuries sold off with the yield on the 10-year note rising 3 basis points to close at 4.62%. The dollar index was down on the day, falling 0.26 points to close at 81.24. Advancing issues represented 78% and 67% for the NYSE and NASDAQ respectively, reflecting a broad rally in the markets.

Oil prices were flat on the day after a mixed petroleum inventory release that showed a jump in crude inventories and a sharp decline in gasoline inventories. Precious metals were mixed with gold rising .00/oz to close at 1.30/oz (+0.61%), with silver also posting a gain of __spamspan_img_placeholder__.02/oz to close at .64/oz (+0.17%).

The rally in the markets was broad based as all ten of the S&P 500 sectors were up on the day, with the materials (3.15%), industrials (+1.87%), and the telecommunication sectors (+1.58%) showing the greatest advance. Defensive sectors such as the consumer staples (+0.70%) and health care sectors (+0.87%) as well as the financial sector (+0.83%) were the day's weakest groups.

Overseas markets also rallied with Latin markets leading world markets with the Brazilian Bovespa (+3.87%) and Mexican Bolsa (+2.45%) indexes posting strong gains. Asian markets were the day's weakest markets with the Japanese Nikkei 225 index (+0.00%), Taiwan Taiex index (+0.17%), and Chinese Shanghai index (+0.50%) posting the days smallest gains.