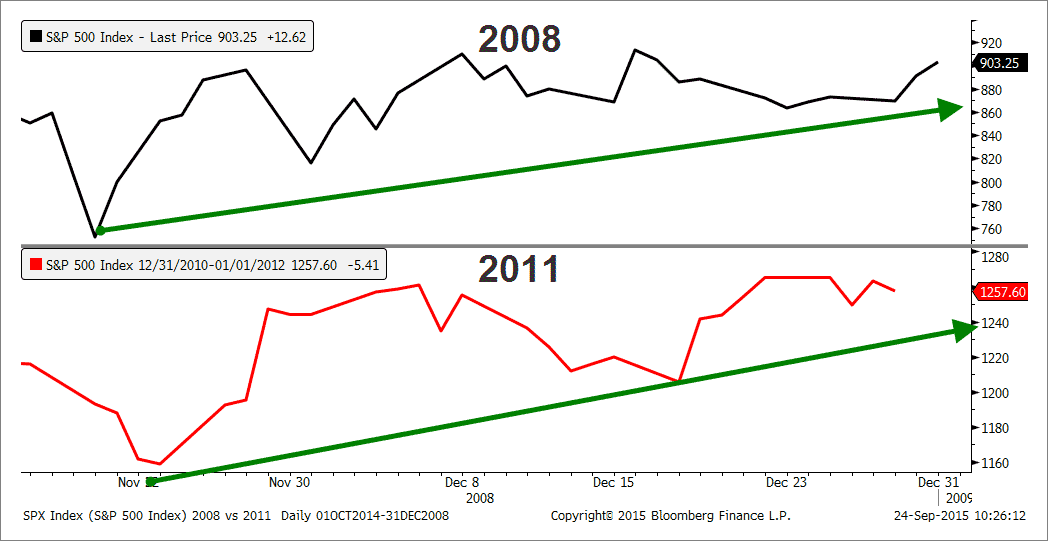

I think we are replaying the general market correction process similar to 2011. Back then the concern was over Europe, which represents the single largest economic region in the world, and this time around it’s China. Notice the S&P's similarity between today (in black) and 2011 (in red):

Looking at the US economy, manufacturing (top panel) continues to weaken from a combination of a strong dollar, weak foreign demand, and falling commodity prices. However, the service sector (bottom panel), which is roughly 70% of GDP, is doing VERY well.

Given how strongly the service-based sector of the economy is performing, I see little to no odds of a recession on the near-term horizon, which would likely lead to a protracted bear market the likes of 2001-2002 or 2008-2009. That said, we can have a technical bear market (20% or more decline) without a recession as we saw in 2011 (2011 May high to October low was close to 21%), which is what I think we may see again. If that's indeed the case, we should revisit last month’s levels and bounce around into October before a possible year-end rally. The last two months of the year have historically been some of the best months due to Christmas holiday sales in which many retailers finally make a profit and I would expect the same this year. Even in 2008 in the midst of the worst bear market since the Great Depression we rallied in Nov-Dec. The same was true in 2011 after the mini-bear market where we rallied in Nov-Dec as shown below:

In general, I expect the world's largest economy, the US, to continue to hang in there as the service sector is still doing very well. Financial market volatility will likely persist heading into October until seasonal forces help bring about a possible year-end rally. If this scenario plays out, it will be important to see whether US and global economic growth improves, both alleviating market fears and leading to a resumption of the bull market. If the opposite is true and we see risk measures deteriorate further, preservation of capital will be much more important as the likelihood of a structural bear market increases.