Overview:

- Deteriorating dollar being masked by weakening Euro/Yen

- More and more currencies strengthening relative to the dollar

- Euro still likely to rally as economic growth and monetary conditions improve

- Europe already leading global recovery while U.S. growth wanes

“Markets can remain irrational longer than you can remain solvent”

–John Maynard Keynes

In my last article I was laying the foundation for a US dollar (USD) correction predicated on the following:

- Extreme bullish sentiment towards the USD

- Mean reversion – USD move is stretched by several metrics

- A global economic recovery would turn optimism away from USD and towards foreign markets/currencies

- USD at long-term technical resistance

Currently the USD Index rests at 95.162 and is only slightly below the high made on January 25th at 95.527 and at first glance it appears as though it is strengthening. However, the recent strength by the USD appears to be stemming from strength relative to two currencies, the Euro and the Yen. The weights in the USD Index are shown below and the weight of the Euro and Yen explain 71.2% of the USD Index and can mask how the USD is doing on a global scale.

Source: Bloomberg

The Japanese Yen has been consolidating the weakness seen in 2014 and appears as though it may start a new leg lower relative to the dollar and today the Euro broke down after stabilizing in the past month though it is still above its January lows of 1.1098 and is heavily influencing the USD Index higher today which is up just over 1%.

While the USD Index is rallying there is deterioration beneath the surface that suggests a cyclical correction in the dollar may be in the offing. We can look at breadth to determine how strong or weak the dollar is by comparing it to many currencies across the globe. I look at breadth in two ways: first by measuring foreign currency returns relative to the USD over different time periods and then as the percentage of currency pairs that are over various moving averages.

If the dollar is set to turn lower we should begin to see more and more currencies posting gains relative to it on short-term time frames (1-day returns, 5-day returns) and then, if the move is going to be sustained, foreign currency gains spill over into longer time frames (1-month, 3-month, and so on). Shown below are foreign currency and precious metal returns relative to the dollar and, despite the strength it has shown recently, the dollar is actually down compared to 22 of the 34 currency pairs (~ 65%).

Foreign Currency Returns Relative to USD

Source: Bloomberg

The other way I monitor the strength or weakness of the dollar is by looking at the percentage of foreign currency USD pairs that are above various moving averages from short-term moving averages (10-day) to longer term-moving averages (200- day). Like the return table above, if the dollar is getting ready to correct more, foreign currency pairs to the USD will be above short-term moving averages (10-day) which will then show an increase in currency pairs above intermediate-term moving averages (50-day) as the correction matures.

Looking at the table below shows that 15 out of the 34 currency pairs are above their 20-day and 50-day moving averages as the USD has begun to weaken on a global scale in the last few weeks. However, on a long-term basis only two currencies out of 34 (Thai Baht, Philippine Peso) are above their 200-day moving averages which shows how powerful and broad-based the USD move has been over the last year. That said, the recent strength by foreign currencies suggests the USD could be taking a much needed breather in the weeks ahead.

Source: Bloomberg

While the weakness in the Euro is masking the recent deterioration in the dollar on a global basis and may be embarking on a new leg lower I believe we should still see a strong rally in the Euro and correction in the USD in the weeks and months ahead even with the European Central Bank (ECB) is slated to officially begin quantitative easing (QE) in March. While it may sound crazy for the Euro to rally while its central bank is actively devaluing the currency by printing money, we’ve seen it happen several times in the U.S. and the flow of logic is explained below.

- Stock market declines as it discounts future economic weakness

- Economy slows down as does inflation rates and currency weakens as a result

- Central bankers then worry about declining economic growth and falling inflation rates and launch QE

- QE program boosts consumer and business confidence and easing monetary conditions spur credit growth

- Rising confidence and credit growth lead to a bounce in economic activity and currency rises on economic strength

- Inflation later in the cycle heats up and hurts consumers and corporate profit margins

- Stocks decline as they anticipate future economic weakness as does the currency…..wash, rinse, repeat

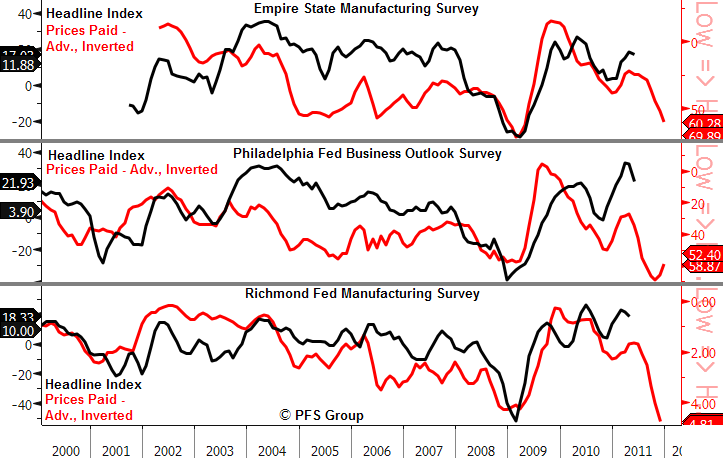

To see this cycle in action I was looking at inflationary trends back in May 2011 just after Bill Gross who was at PIMCO at the time made news that he was shorting UST Bonds in the company’s flagship Total Return Fund. In the article (Why Bill Gross is Wrong…In the Short Term) I laid out how leading economic indicators and the pickup in inflationary signals like the relative performance of early to late cyclicals were heralding a growth slowdown ahead which would push stocks lower and UST bond prices higher. I expanded on the article later in May (Global Slowdown Head, Recession Not Likely) and showed how the increase in the prices paid component in various regional Fed surveys was indicating a growth slowdown as they were hitting their inflationary highs seen in 2008 when oil rose near 0/barrel with the chart highlighted back then shown below.

Source: Bloomberg

Follow the Money

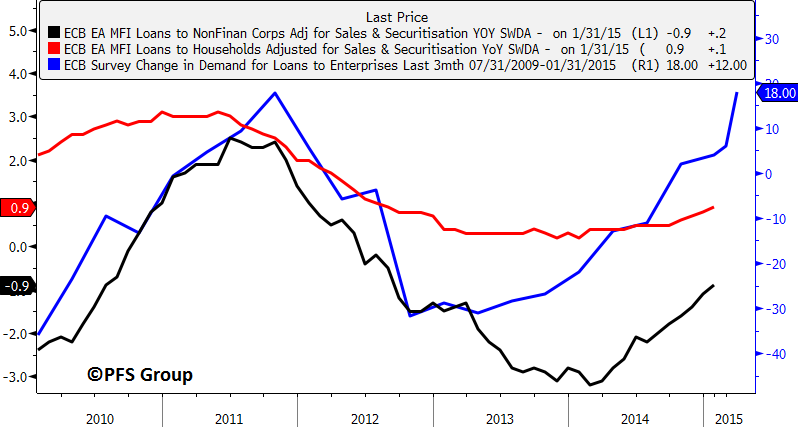

Various leading economic indicators I am tracking as highlighted in my last several articles suggest that not only European growth should pick up but so too global growth. In the case of Europe, bank lending which had been declining since 2011 is making a turnaround and being led by loans to enterprises while even loans to households has stabilized and is turning up. As well, M3 money supply growth is at its strongest level since 2009.

Source: Bloomberg

Source: Bloomberg

Europe Leading Global Economic Charge While U.S. Lags

We are already seeing signs that European growth is turning around as the Eurozone Market PMI has seen three consecutive monthly increases and when looking at the Citigroup Economic Surprise Indices for global regions, Europe (green line below) is leading the charge with the strongest string of positive economic surprises while the U.S. (blue line below) is showing the most negative surprises.

Source: Bloomberg

If we see European growth pick up we are likely to see the Euro rally even with the ECB undergoing QE. As crazy as this sounds this is exactly what happened early on with QE2 and QE3 in the US. Back in 2010 the U.S. Manufacturing PMI was decelerating and along with it we saw a falling USD and stock market. However, once QE2 began we saw the stock market was already in a powerful rally as Bernanke hinted at QE2 in August 2010 and the PMI was recovering as the economy improved which led to a USD rally even with the Fed expanding its balance sheet (see green shaded box below). As the economy heated up we saw the CPI inflation rate rise from just over 1% late in 2010 to a peak near 4% in the middle of 2011 which hurt the USD and brought economic growth lower.

Source: Bloomberg

A similar scenario played out with QE3 in which we had a rising stock market, a stronger USD, increasing economic activity all in the face of an expanding Fed balance sheet (green box below).

Source: Bloomberg

I believe this same situation is likely to be seen in Europe where the Euro should rally even as the ECB ramps up the printing presses on higher optimism towards Europe in conjunction with an improved economic outlook.

Summary

In my last article I made the case that we are likely to see a dollar correction and promised to write about the investment implications in my next article. However, in light of the recent strength in the USD and weakness in the Euro I wanted to shed more light and provide greater evidence as to why I still believe the USD should correct while the Euro rallies and will touch upon the investment applications should the dollar decline in my next article.

The broadening economic confidence in Europe in conjunction with easing lending standards and a stronger demand for credit should lead to a European recovery and a stronger Euro even with the ECB expanding its balance sheet as this has happened twice already in the U.S.