The U.S. economy is building momentum in both the service and manufacturing sector which is clearly visible no matter where you look, and June’s employment report is a perfect example. The U.S. economy added 288K jobs in June which puts the average monthly payroll addition this year at 231K jobs added each month. With the U.S. economy's average at 174K/mo in 2011, 186K in 2012, 194K in 2013 and the current 231K this year, there is a clear and undeniable acceleration in payroll growth. In fact, as you can see below, we haven't seen job growth this strong since going back to the mid to late '90s.

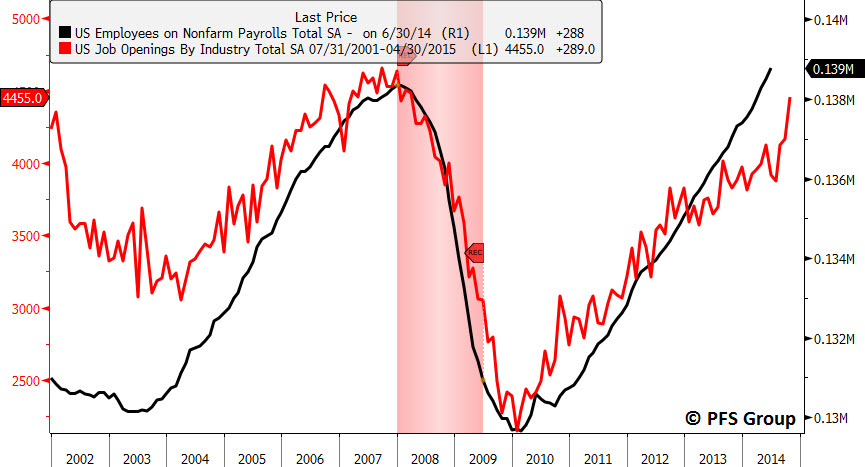

When looking at leading economic indicators of employment, the recent momentum may continue to build into the fall. The Job Openings and Labor Turnover Survey (JOLTS) report put out by the Bureau of Labor Statistics (BLS) measures total job openings which leads payroll levels by several months. There was a sharp acceleration seen in April (the most recent monthly release), which gave advance notice of today's strong number. Given the lead time of six months between the job openings data and monthly payrolls, the recent April release of job openings suggests monthly payroll growth should continue to build on June’s strong 288K addition.

Source: Bloomberg

The recent surge in economic momentum is taking economists by surprise as they are consistently making forecasts that are too low. The Bloomberg Economic Surprise Index, which measures the percentage of releases coming in above or below consensus expectations, jumped to the highest level since early 2013 and broke a string of lower highs that have been in place since 2011.

Source: Bloomberg

We’ve also seen a break in the declining trend that has been in place since 2011 for transportation shipments. The Cass Freight Shipment Index has been accelerating over the last few months, which supports the move higher in the Dow Jones Transportation Index.

Source: Bloomberg

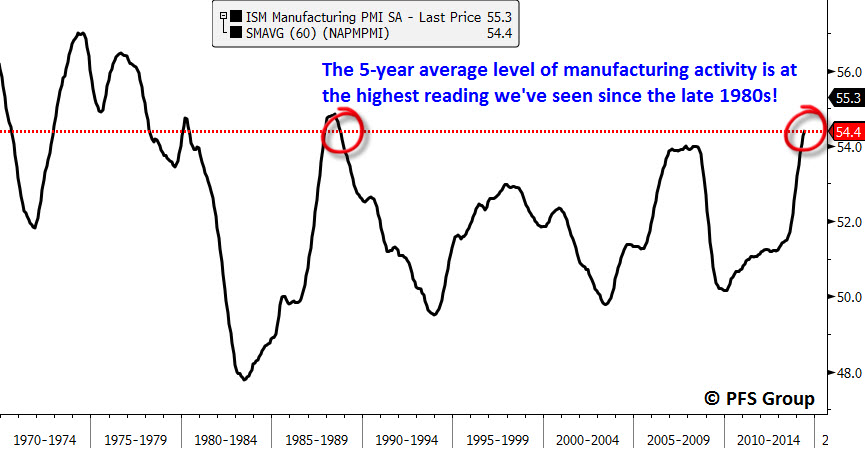

Not only is our job market and transportation sectors picking up momentum but so too is the manufacturing sector. While the average monthly payroll growth in the U.S. is at a 15-year high, the 5-year average in the ISM Manufacturing PMI is at the highest level seen in a quarter century with its 54.4 reading.

Source: Bloomberg

Hat Tip: Neil Dutta, Renaissance Macro

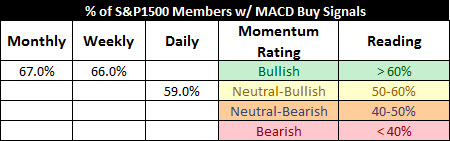

The markets are not ignoring the good news as we saw the Dow Jones Industrial Average close over the 17,000 mark for the first time with the S&P 500 only 15 points away from hitting 2000. The momentum building in the economy is also translating into market momentum as we are seeing the strongest intermediate-term momentum in the markets since November of last year. I measure market momentum with the Moving Average Convergence-Divergence (MACD) indicator and use daily readings for short-term momentum, weekly readings for intermediate-term momentum and monthly readings for long-term momentum.

I survey the percentage of members within the S&P 1500 (approximately 92% of the entire US market cap) on MACD buy signals and what worried me late last year and the early part of this year was that the intermediate-term momentum of the market was slipping which is of great concern because momentum always peaks before the stock market does. What worried me was that we were seeing new highs in the market associated with weaker intermediate-term momentum, however, that has changed recently as the weekly MACD buy readings for the S&P 1500 has surged and are almost back above 70%. The improvement in the weekly numbers has helped to also arrest the decline we were seeing in the monthly numbers and suggests we could be in the midst of a summer melt up in the stock market.

Summary

We are seeing economic and stock market momentum building after a very weak Q1 which saw the first negative GDP print in some time. The recent surge in momentum is alleviating investor concerns that the US economy is faltering and current leading economic indicators suggest the momentum we are seeing should continue for several more months, which may lead to a summer melt up in stocks.

We need to be on the lookout though for a surge in inflation which may bring the timetable for the Fed’s first rate hike into view closer than many participants are expecting. This should lead to greater volatility and the potential for economic momentum to slip in the fall, something that was commented upon in an earlier article (“Countdown to Another Market Peak Has Begun”). While there may be some distant clouds on the horizon suggesting caution we have bright and sunny skies overhead as a summer melt up in stocks remains a strong possibility given high cash levels and high short interest levels by institutional investors.