The Latest Conference Board Consumer Confidence Index was released this morning based on data collected through November 13. The headline number of 88.7 was a surprising drop from the revised October final reading of 94.1, a downward revision from 94.5. Today's number was well below the Investing.com forecast of 95.9.

Here is an excerpt from the Conference Board press release.

Says Lynn Franco, Director of Economic Indicators at The Conference Board: “Consumer confidence retreated in November, primarily due to reduced optimism in the short-term outlook. Consumers were somewhat less positive about current business conditions and the present state of the job market; moreover, their optimism in the short-term outlook in both areas has waned. However, income expectations were virtually unchanged and gas prices remain low, which should help boost holiday sales.”

Consumers’ assessment of present-day conditions was moderately less favorable in November than in October. The proportion saying business conditions are “good” decreased from 24.7 percent to 24.0 percent, while those claiming business conditions are “bad” increased from 21.3 percent to 22.4 percent. Consumers’ assessment of the job market was slightly less favorable, with the proportion stating jobs are “plentiful” falling from 16.5 percent to 16.0 percent, and those claiming jobs are “hard to get” increasing marginally from 29.0 percent to 29.2 percent.

Consumers’ optimism, which had improved in October, retreated in November. The percentage of consumers expecting business conditions to improve over the next six months decreased from 19.4 percent to 17.6 percent, while those expecting business conditions to worsen rose from 8.9 percent to 10.7 percent. Consumers’ outlook for the labor market was also less optimistic. Those anticipating more jobs in the months ahead decreased from 16.0 percent to 15.0 percent, while those anticipating fewer jobs rose from 14.1 percent to 16.4 percent. The proportion of consumers expecting growth in their incomes edged down from 16.7 percent to 16.3 percent, while the proportion expecting a drop in income was virtually unchanged at 11.4 percent compared to 11.3 percent in October.

Putting the Latest Number in Context

Let's take a step back and put Lynn Franco's interpretation in a larger perspective. The table here shows the average consumer confidence levels for each of the five recessions during the history of this monthly data series, which dates from June 1977. The latest number is 19.3 points above the recession mindset and 5.5 points below the non-recession average.

Let's take a step back and put Lynn Franco's interpretation in a larger perspective. The table here shows the average consumer confidence levels for each of the five recessions during the history of this monthly data series, which dates from June 1977. The latest number is 19.3 points above the recession mindset and 5.5 points below the non-recession average.

The chart below is another attempt to evaluate the historical context for this index as a coincident indicator of the economy. Toward this end I have highlighted recessions and included GDP. The exponential regression through the index data shows the long-term trend and highlights the extreme volatility of this indicator. Statisticians may assign little significance to a regression through this sort of data. But the slope clearly resembles the regression trend for real GDP shown below, and it is a more revealing gauge of relative confidence than the 1985 level of 100 that the Conference Board cites as a point of reference. Today's reading of 88.7 is above the current regression point of 78.6.

On a percentile basis, the latest reading is at the 42th percentile of all the monthly readings since the start of the monthly data series in June 1977 and at the 37th percentile of non-recessionary months.

For an additional perspective on consumer attitudes, see my post on the most recent Reuters/University of Michigan Consumer Sentiment Index. Here is the chart from that post.

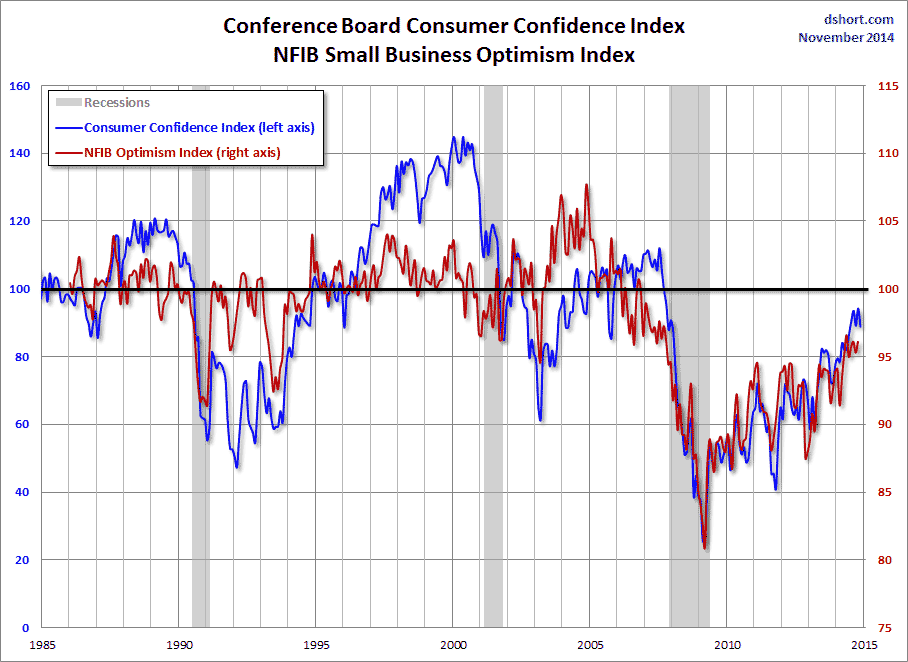

And finally, let's take a look at the correlation between consumer confidence and small business sentiment, the latter by way of the National Federation of Independent Business (NFIB) Small Business Optimism Index. As the chart illustrates, the two have tracked one another fairly closely since the onset of the Financial Crisis.