The EIA published International Energy Outlook 2011 (IEO 2011) on September 19, showing energy projections to 2035. One summary stated, “Global Energy Use to Jump 53%, largely driven by strong demand from places like India and China.”

It seems to me that this estimate is misleadingly high. The EIA is placing too much emphasis on what demand would be, if the price were low enough. In fact, oil, natural gas, and coal are all getting more difficult (and expensive) to extract. Prices will need to be much higher than today to cover the cost of extraction plus taxes countries choose to levy on energy extraction. The required high energy prices are likely to lead to recessionary impacts, which in turn will cut back demand for energy products of all types.

We live in a finite world. While it is true that huge resources of oil, natural gas, and coal are still theoretically available, we are starting to reach practical limits regarding extraction at prices that do not lead to economic contraction.

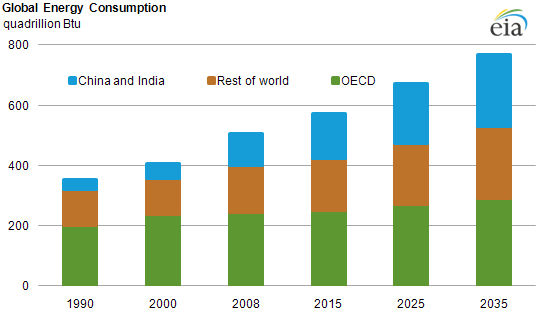

An IEO 2011 summary exhibit shows that world energy consumption will more than double, between 1990 and 2035:

Figure 1. Global energy consumption, from EIA summary https://www.eia.gov/todayinenergy/detail.cfm?id=3130

It is only by drilling down into the report that we can see what the problems with the forecast really are.

Liquids Projections

Clearly oil and other “liquids” (used to extend oil) are one of the potential problem areas, since the price of oil has been rising rapidly since 2000. EIA’s liquid fuels projection is shown as follows:

Figure 2. IEO 2011 World Liquid Fuel Production, according to EIA.

The first thing a person notices when looking at the graphs is how poorly the forecasts of future production match up with recent past actual production. Non-OPEC production has recently been declining, after reaching a peak of 48.1 quadrillion Btu in 2004. Somehow, miraculously, the EIA expects that Non-OPEC production will start increasing, rising from 46.8 quadrillion Btu in 2009 to 53.9 quadrillion Btu in 2035. The text suggests this will come from ultra deep wells, from the arctic, and from enhanced oil recovery.

Oil production from individual wells naturally declines over time, by about 5% per year, so new fields must constantly be added, to keep production level. The graph indicates that since 2004, non-OPEC countries have not been able to add enough new production to keep conventional production level. What makes the EIA think that this problem can be turned around, with very high cost, risky new investments?

The forecast for OPEC conventional is even more of an enigma, because it shows even larger increases. OPEC countries claim very large reserves, but these have not been audited, and when it comes to what should be a simple task–replacing the lost oil output of Libya–they seem to have difficulty. Recently, King Abdulla of Saudi Arabia has been quoted (for example, in a WSJ an article titled, “The Next Crisis: Prepare for Peak Oil,”) as saying that new oil finds should be left in the ground for their children.

If the OPEC countries we are depending on are not planning for the big increases we are hoping for, we have a problem. I am not aware that OPEC has given any indication that their production (conventional oil or otherwise) can reach as a high level as the EIA is forecasting. Even big increases in production from Iraq would not seem to be enough to provide OPEC’s hoped-for increase.

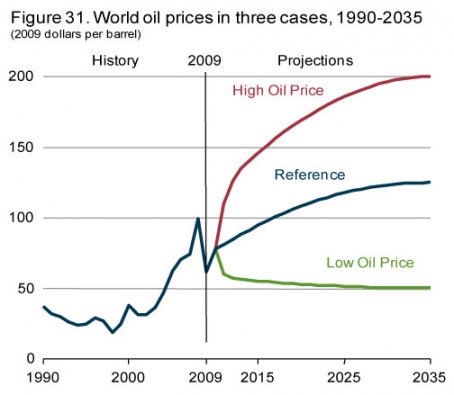

I suppose that a person could argue that if oil prices were a lot higher, oil companies might be willing to use more expensive techniques to extract oil. But the EIA shows this graph regarding price expectations:

Figure 3. IEO 2001 world oil price estimates.

In the reference case, oil prices do not rise much above today’s high level between now and 2035. (The EIA does not indicate what oil benchmark is being used, but the context suggests it would be an average price level, more similar to Brent price than to today’s distorted West Texas Intermediate price level. Such prices have recently been in the 0 to 0 barrel range.)

Part of the reason that very high oil prices are needed is because governments are becoming more and more “needy,” and see oil companies as a potential source of revenue. According to the Economist, next year Russia (the world’s second largest oil exporter) will need a price of 0 barrel to meet its spending obligations. Also, President Obama keeps talking about raising taxes on US oil and gas companies. Higher taxes will mean that higher oil prices will be needed to encourage development of very deep and very risky resources. These issues mean that to have a chance of raising oil production, oil prices really need to be on the “high oil price” trajectory of Figure 3, not the “reference case” scenario.

If oil prices really rose to the high oil price trajectory, there would be huge transfer of funds from importers to exporters, and importers would be in even worse financial trouble than they are today. Food prices would be expected to rise with oil prices, so even oil exporters (who are food importers) could expect to have problems. At such high oil prices, it seems likely that we would see even more revolution and replacement of governments than we saw this spring.

The written analysis in the IEO 2011 report is based on the reference scenario, but schedules are available showing the indications of the high oil price scenario. Amazingly, with EIA’s high price scenario, energy production is even higher, and world economic growth is even higher. The world’s average annual growth in world GDP is 3.4% per year in the reference scenario (with an unrealistically low oil price), and 4.0% per year in the high oil price scenario. When people are spending a disproportionate share of their paychecks on oil and food, and road repairs are becoming increasingly unaffordable for governments, how are economies possibly going to be growing more rapidly? If a greater share of investment will need to be plowed back into the oil and liquids sector, how can this mean that there can be more growth elsewhere?

Besides OPEC and non-OPEC conventional oil, the third category is unconventional liquids. An explanatory chart gives the following breakdown:

Figure 4. IEO Unconventional Fuels Projection by Source

With alternative fuels, high price is again important, because it helps make the big investment required profitable. The Oil Sands / Bitumen projection is perhaps reasonable, if prices can actually follow the high trajectory without sinking economies (a very big if). The biofuels projection depends on the development of biofuels which do not use foods as inputs. So far, technological progress on these has been slow. Even if very high prices can be maintained, the biofuels forecast seems like a “stretch”.

Some gas to liquids increase seems likely, perhaps even more than the EIA is forecasting. These plants appear to be profitable now, even without 0 to 0 barrel oil prices. Coal to liquid and shale oil would seem to be farther away economically than gas to liquids. However, if the world economy could really withstand 0 oil prices, perhaps these types of plants could be built.

Part of the issue with very high oil prices is that they imply that it makes economic sense to use very high energy inputs (and water inputs) to produce these liquids. Clearly, at some point, the cost simply becomes unacceptably high because it takes more than one barrel of oil to produce a barrel of oil, or because the pollution issues become unbearable. For example, theoretically, it would be possible to pump water uphill from the Great Lakes to Colorado to be able to produce shale oil, if the price were high enough. But it is hard to see this making sense on any reasonable terms. The assumption that prices can rise arbitrarily high is simply not true.

Natural Gas

Natural gas indications are less clear, because the forecast is a summary of forecasts for different regions, each with different issues. Transport is more difficult for natural gas than oil also.

New techniques are now being used to extract more difficult-to-extract natural gas, but these are controversial in more than one way:

- Long term profitability is difficult to calculate in advance because a huge up-front investment is required and calculation of long-term profitability includes several assumption which can easily be “selected” to produce the desired result. Are natural gas operators claiming profitability at lower prices than is really possible? If prices were high enough to be profitable, would demand stay at high levels?

- What are the environmental consequences of such huge fracking operations? Will it be possible to dispose of all of the polluted water that comes back up in an environmentally friendly way? Are there other environmental issues? Will governments permit wide-scale use of fracking?

The EIA appears to have decided that these controversies will decided in the direction of allowing big increases in natural gas production. The IEO 2011 shows this estimate of natural gas reserves:

Figure 5. IEO 2011 Natural Gas Reserves by Region

The indication is that North America and Europe have relatively little in reserves. There are huge reserves in locations where it is difficult to verify the accuracy of the reserves, and where transport to North America or Europe would be difficult. While ships carrying liquefied natural gas (LNG) can be used, there would seem to be a practical limit as to how much can be transported in this manner. Pipelines can be built, but it is expensive to build these pipelines, and they need the approval of all of the countries along the pipeline.

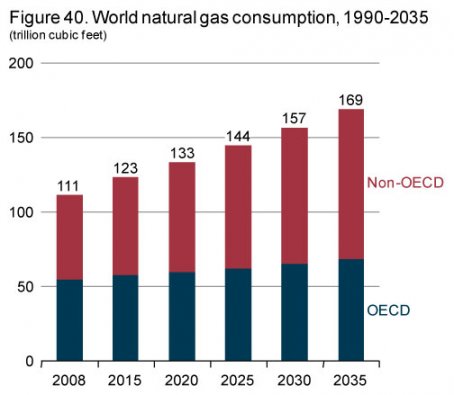

In total, the EIA sees a huge increase (52%) in natural gas use between 2008 and 2035, with the majority of increase outside OECD, according to the report’s Figure 40.

Figure 6. IEO 2011 World Natural Gas Consumption Projections

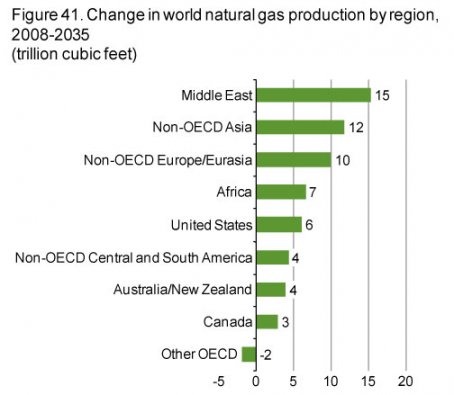

The countries that are expected to increase production tend to be concentrated in the Middle East and in lesser developed countries around the world, according to the report’s Figure 41.

Figure 7. IEO 2011 Change in Natural Gas Production

One area which shows an increase in production is the United States. This is controversial, for reasons mentioned above (likely high price needed for profitability; environmental impacts). Europe shows a continuing decline in production. A number of European countries are already finding themselves in financial difficulty. If more natural gas needs to be imported, this can only add to financial difficulties.

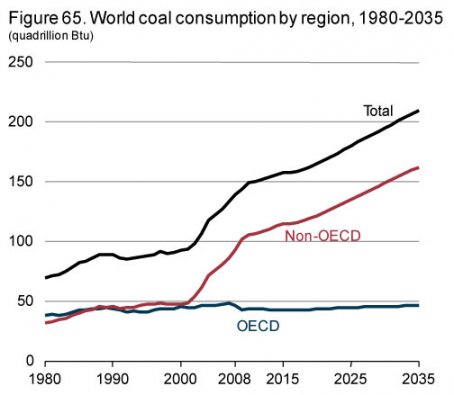

Coal

The EIA shows continued growth rapid growth in coal production and consumption.

Figure 8. IEO 2011 World Coal Consumption Projections

Is this kind of coal projection realistic? As with oil and gas, there is an issue of needing to extract ever lower-quality resources, from greater depths. Many of the seams that are left in easily accessible locations are thinner and more expensive to extract. IEO 2011 indicates that an increasing portion of the coal will be imported. Thus, the cost of shipping will add to the cost to the final customer. All of these factors mean that we can expect the cost to produce a Btu of delivered coal to rise over time. We can think of this as lower Energy Return on Energy Investment (EROEI), or as higher cost of production.

If the price of coal rises, a person would expect coal demand to fall, if coal demand is at all elastic. Because of this relationship, it will be difficult for long-term consumption to rise as much as the EIA forecasts suggest. This expected slowdown in coal production due to higher price is not very different from peak coal indications arrived at through curve fitting techniques, such as this analysis by Dr. Minqi Li.

With coal, there are also environmental issues, both from a CO2 point of view, and from the point of view of other pollutants. Will the world really be willing to put up with such high coal use, over the long-term?

Note that the issues with any of the fossil fuels is not that the resources are not there. The issue is that the cost of extracting them keeps escalating, making it increasingly difficult for society to afford these high costs. There are also environmental costs that must be considered.

Renewables

Renewables are not shown in a separate section in IEO 2011. Instead, the biofuel portion is included with liquids (see Figure 4 above) and other renewables are shown as a subsection of Electricity. The Electricity subsection says:

Although renewable energy sources have positive environmental and energy security attributes, most renewable technologies other than hydroelectricity are not able to compete economically with fossil fuels during the projection period except in a few regions or in niche markets. Solar power, for instance, is currently a “niche” source of renewable energy, but it can be economical where electricity prices are especially high, where peak load pricing occurs, or where government incentives are available. Government policies or incentives often provide the primary economic motivation for construction of renewable generation facilities.

Renewables are mentioned in the summary. There, one of the key findings is

Renewables are the world’s fastest-growing energy source, at 2.8% per year; renewables share of world energy grows to roughly 15% in 2035

This graph is also provided in the summary presentation:

Figure 9. IEO 2011 Expected Growth in Various Fuels to 2035

A backup exhibit shows that hydroelectric amounted to 85% of renewables in 2008, so the 10% of energy consumption is split roughly 8.5% to hydroelectric, and 1.5% to other renewables. In 2035, hydroelectric amounts to only 68% of the renewable subtotal, so the 14% in 2035 is roughly 9.5% hydroelectric and 4.5% other renewables. Thus, “other” renewables used in electricity production are expected to roughly triple as a percentage, from 1.5% to 4.5% of the total, by 2035.

Concluding Thoughts

The EIA estimates of future fuel consumption seem to be optimistic throughout. It is hard to see what benefit such a bias would have, other than to protect the careers of political leaders and to keep people from understanding that there is a real possibility of energy limits affecting the economic system in the not too distant future.

There is widespread misunderstanding of our fossil fuel problems. The belief is that the fuels will somehow “run out.” In fact, the issue is that they will become too expensive to afford, or, if you think in terms of “peak oilers,” the Energy Return on Energy Investment (EROEI) will drop too low. High energy prices will likely lead to reduced energy consumption, which in turn will lead to recession, reduced economic growth, and eventually lower energy prices (as we saw in late 2008). At these lower prices, the high cost (low EROEI) resources will no longer be profitable to extract, and the extraction of these high cost resources will disappear.

Thus, the issue is really that high price / low EROEI is the limiting factor on resource extraction. That is what the EIA missed in their forecasts.

Source: Our Finite World