Our economy runs on oil. Most of the tractors used for growing food run on oil. Nearly all of today’s cars and trucks run on oil. It is popular to talk about changing to some other fuel, but the practicalities are that any such change will be very slow. There is a huge cost associated with replacing cars and trucks with vehicles using other fuels, assuming we could figure out the technology to do this.

Since 2005, world crude oil supply has bumped up against what seems to be a limit of 75 million barrels of oil a day. No matter how hard companies try to extract more crude oil, and no matter how high world oil prices rise, they seem unable to extract more than 75 million barrels a day (MBD).

Figure 1. World crude oil production has been bumping up against a limit of about 75 million barrels a day (MBD) since 2005, as oil prices have gyrated wildly. (EIA data)

The US Government is aware of this issue, and now issues data for Total Oil Supply. Total oil supply includes various other liquids that are somewhat like crude oil, including biofuels, natural gas liquids, and “refinery gain”. But even including the additional categories, growth in supply has been anemic. Oil prices started rising as early as 2004 because supply (whether defined as crude oil or more broadly) was not rising fast enough to meet increased demand around the world.

With world oil supply virtually flat, countries have had to share what oil is available. Since 1985, there has been a big shift in which countries are the “winners” in the way the world’s limited oil supply is divided (Figure 2).

Figure 2. Growth in oil consumption has varied greatly in recent years. The Former Soviet Union’s oil use dropped off after its break up in 1991. Europe, US, Japan, and Australia showed modest growth until 2005, followed by a drop off. Consumption of countries in “Remainder” (which includes China, India, and oil exporting countries) has risen rapidly since 1985. (Based on EIA data)

Clearly the “winners” in the contest for who is able to buy the oil are the “Remainder” countries—countries like China and India and Korea, and the oil exporting nations.

Over the period 1985 – 2010, the grouping “Europe, US, Japan, Australia” experienced an average real GDP growth rate of 2.4%; the Remainder group experienced an average growth rate of 4.7%. The Former Soviet Union experienced a peak to trough drop in real GDP of 41% after its breakup in 1991. The grouping Europe, US, Japan, and Australia experienced a major dip in oil consumption and a serious recession in 2008-2009, while the Remainder countries continued to grow.

High oil prices are clearly a problem for oil importing countries, because funds that would have been used for discretionary spending suddenly need to be used for necessities—food that is grown and transported using oil, and gasoline used for commuting to work. It is precisely the big oil importing countries that have tended to have a problem with reduced economic growth when oil prices are high.

In my view, what the world needs now is inexpensive oil, and lots of it. What we need is enough inexpensive oil to bring oil prices back down to to dollars a barrel, like it was in the 2001 to 2003 period. If we had inexpensive oil in this large quantity, there would be plenty of oil to go around. It wouldn’t be only the oil exporters and the countries with large coal-based manufacturing industries that would be able to consume as much oil as they need for economic growth. Countries like Greece and Spain, which need low oil prices to stoke world tourism, would be able to consume their share of the oil as well.

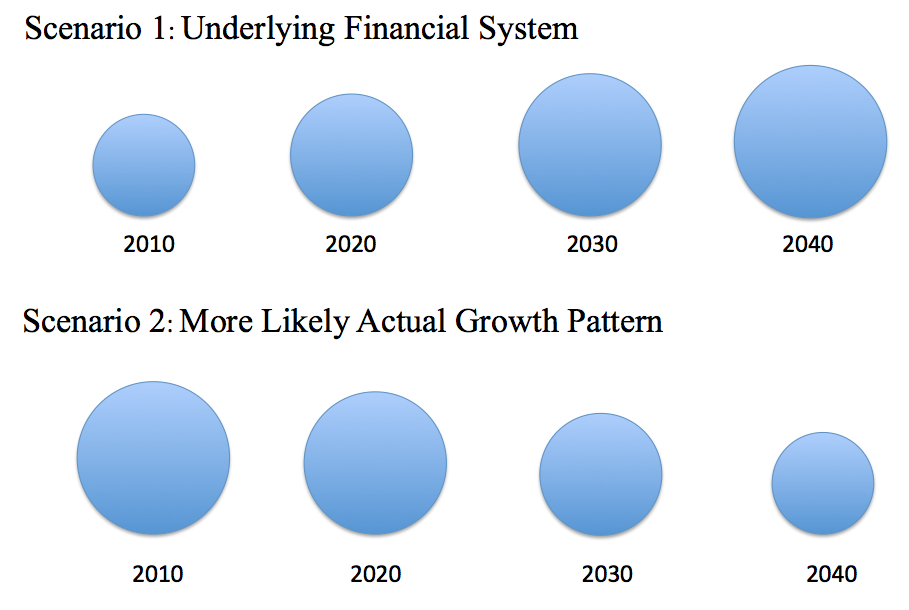

One issue is of concern is the connection between economic growth and debt.

Figure 2. Two views of future economic growth

If an economy is growing, as in Scenario 1, it makes financial sense to borrow money, even if it is necessary to pay it back with interest. Borrowing makes it possible to “pre-spend” a little of the economic growth that will be available in the future. This relationship is especially important for governmental borrowing, but it also plays a role for private borrowing.

If an economy is shrinking, it is hard to make a case for borrowing. In such a case, the future is likely to have less to offer than what we have today. This might happen if there is not enough oil to go around, and oil prices are very high (at least until recession hits).

A great deal has been said about decoupling economic growth from natural resource use. It is not clear to what extent this really is possible. We can move manufacturing to the Far East, and pretend that the resource use isn’t ours, but on a world basis, during the past decade, energy use has been rising as fast as world real GDP. This has happened largely because Asian growth in energy use has offset savings elsewhere.

Theoretically, if world oil supply is inadequate, we should be able to make substitutions that would work—either find a different liquid fuel to substitute for oil, or create new vehicles or machines that use a different source of energy than petroleum products. The problem is that making these substitutions is a slow, expensive process.

We are currently using millions of cars, trucks, trains, airplanes, boats, and machines that require petroleum products to operate. Most of them are nowhere near the ends of their normal lives, so replacing them would be expensive.

Liquid biofuels we have developed are expensive. To solve our problem, they really need to cost or dollars a barrel to make.

What the world really needs now is a huge supply of inexpensive oil. It is not clear where we will find it, however.

(Note: This post was written in response to a request by Business Insider that I write a short editorial in response to the question, “What is the most important resource for our future?” It covers some of the main points in my new academic article in the journal Energy, “Oil Supply Limits and the Continuing Financial Crisis.” That article is temporarily available free at this link, or this one.)

Source: Our Finite World