Time was, no one gave a crap about the Federal Reserve’s board. Who the drones were? What they did? Who cared!

Time was, no one gave a crap about the Federal Reserve’s board. Who the drones were? What they did? Who cared!

But ever since the Fed started to expand its balance sheet in the fall of 2008, what the Fed does has mattered—and now with Quantitative Easing 2 and the effective monetizing of 50% of the Federal government’s deficit, it matters more than ever.

Next week, on January 25, the Federal Reserve’s Open Market Committee (FOMC) will meet. This meeting is important, because the composition of the board will change—and therefore, possibly the direction of the board.

So like Kremlinologists of old, we have to start paying attention to what the FOMC looks like, if we want to divine what will happen.

What will happen not merely with monetary policy, but with the American economy itself.

The Composition of the FOMC—Past & Future

From the Beast itself—the Fed’s own web page—we get the following description:

The Federal Reserve controls the three tools of monetary policy—open market operations, the discount rate, and reserve requirements. The Board of Governors of the Federal Reserve System is responsible for the discount rate and reserve requirements, and the Federal Open Market Committee is responsible for open market operations. Using the three tools, the Federal Reserve influences the demand for, and supply of, balances that depository institutions hold at Federal Reserve Banks and in this way alters the federal funds rate. The federal funds rate is the interest rate at which depository institutions lend balances at the Federal Reserve to other depository institutions overnight.

So like the Beast says: Insofar as the extraordinary measures the Fed has taken over the last two years or so, what matters is the Fed’s Open Market Committee (FOMC). The Board of Governors plus four of the regional Federal Reserve presidents serve on the FOMC, the four regional Fed presidents serving on a rotating basis. As the website says, the FOMC is “responsible for open market operations”—and that covers the original Quantitative Easing (QE), QE-lite, and QE-2.

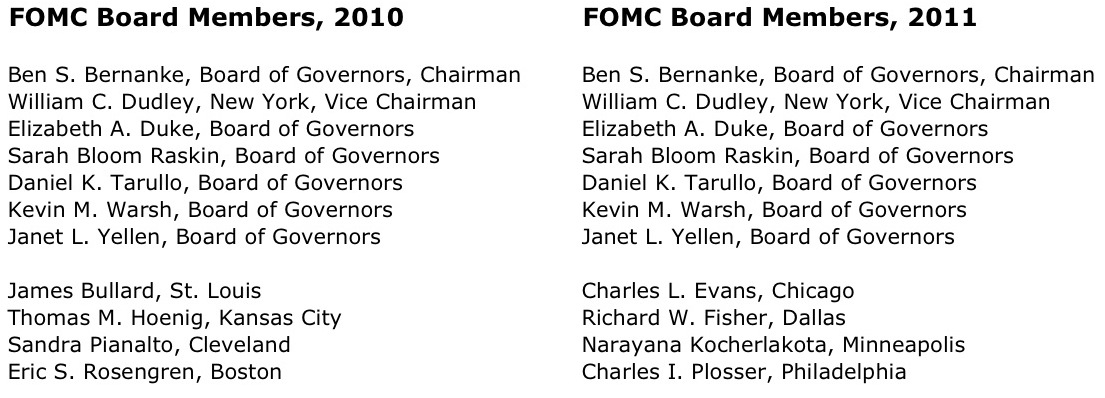

So who makes up the FOMC is crucial. The following is a list of the voting members for the 2010 calendar year, and a list of the voting members for the year 2011 starting at the first meeting, January 25:

The first seven names are the permanent members of the FOMC, while the last four names are the rotating members from the regional banks.

Clearly, the Board of Governors—because of their permanence—is where we should start our analysis. So let’s:

Ben Bernanke: Little needs be said about The Bernank—we know him all too well. Clearly in favor of Quantitative Easing in its various iterations. Here’s a video interview of him on 60 Minutes broadcast this past December—notice the trembling lips and trembling voice:

(Frankly, it was surprising that the bond and equity markets didn’t all crash to smithereens on the Monday following this interview.)

William C. Dudley: A former employee of Goldman Sach (1986–2007), where he held the post of Chief Economist for ten years, Dudley was hired by Timothy Geithner when he headed up the NY Fed; when Tinny Timmy went to Washington, Dudley assumed his old job. Close ties to Wall Street as well as hedge funds and private equity firms. He has supported The Bernank in all his foolish schemes—back in October 2010, he gave a speech where he said, “Viewed through the lens of the Federal Reserve’s dual mandate — the pursuit of the highest level of employment consistent with price stability — the current situation is wholly unsatisfactory.” This was the signal to Wall Street that QE-2 was a definite go. As the situation has not materially changed—unemployment steady at about 10%, “core inflation” at less than a percent—he will likely be at the vanguard for pressing for more QE, if QE-2 isn’t shown to be producing results when it expires in mid-year.

Elizabeth A. Duke: An up-from-behind-the-teller’s-window-by-her-bootstraps banker, Duke studied physics in college before switching to drama (I’m not kidding), graduating from Chapel Hill in ‘74. She worked as a teller, then rose rapidly through commercial banking, picking up an MBA at Old Dominion in ‘83 without interrupting her steady climb, with lots of positions in the local banking industry establishment. She’s a commercial banker—not an economist, not an investment banker: She’s a troops-on-the-ground community banker, housing being her thing; see this recent speech. She’s clearly in favor of keeping real-estate prices propped up in order to “stabilize” the economy—so she’s a hard-core supporter of QE insofar as it guarantees that real-estate prices will not “fall”. She recently declared that rising Treasury bond yields signalled, “If the market expects the economy to strengthen, investors ratchet back expectations for Fed purchases and reduce their bid for the assets, and rates rise.” Her blindspot is obvious: She doesn’t see the dangers of QE—so she will push for more of it, as it helps real-estate prices remain at their bubble level.

Click here to continue reading "Reading The Tea Leaves of the Federal Reserve Board"