The complete unabridged research paper can be found on Gordon T Long's Tipping Points

In September 2008 the US came to a fork in the road. The Public Policy decision to not seize the banks, to not place them in bankruptcy court with the government acting as the Debtor-in-Possession (DIP), to not split them up by selling off the assets to successful and solvent entities, set the world on the path to global currency wars.

In September 2008 the US came to a fork in the road. The Public Policy decision to not seize the banks, to not place them in bankruptcy court with the government acting as the Debtor-in-Possession (DIP), to not split them up by selling off the assets to successful and solvent entities, set the world on the path to global currency wars.

By lowering interest rates and effectively guaranteeing a weak dollar through undisciplined fiscal policy, the US ignited an almost riskless global US$ Carry Trade and triggered an uncontrolled Currency War with the mercantilist, export driven Asian economies. We are now debasing the US dollar with reckless spending and money printing with the policies of Quantitative Easing (QE) and the expectations of QE II. Both are nothing more than effectively defaulting on our obligations to sound money policy and a “strong US$”. Meanwhile with a straight face we deny that this is our intention.

It’s called debase, default and deny.

Though prior to the 2008 financial crisis our largest banks had become casino like speculators with public money lacking in fiduciary responsibility, our elected officials bailed them out. Our leadership placed America and the world unknowingly (knowingly?) on a preordained destructive path because it was politically expedient and the easiest way out of a difficult predicament. By kicking the can down the road our political leadership, like the banks, avoided their fiduciary responsibility. Similar to a parent wanting to be liked and a friend to their children they avoided the difficult discipline that is required at certain critical moments in life. The discipline to make America swallow a needed pill. The discipline to ask Americans to accept a period of intense adjustment. A period that by now would be starting to show signs of success versus the abyss we now find ourselves staring into. A future that is now significantly worse and with potentially fatal pain still to come.

Unemployed Americans, the casualties of the financial crisis wrought by the banks, witness these banks declaring record earnings while the same banks refuse to lend. When the banks once more are caught with their fingers in the cookie jar with falsified robo-signing mortgage title fraud, they again look for the compliant parent to look the other way. Meanwhile the US debt levels and spending associated with protecting these failed (and still insolvent institutions) are so out of touch with US de-industrialized productive capability that the US dollar is falling and forcing countries around the world to devalue their currencies in a desperate attempt to maintain competitive advantage. So much for the “strong dollar” mantra we heard endlessly for years from every US Secretary of the Treasury that needed foreign investment to fund our deficits. Like second rate powers, our word is no longer our bond.

The fork in the road which we chose has resulted in:

The fork in the road which we chose has resulted in:

1) massive public debt levels that can never realistically be expected to be paid back,

2) Financial markets that are disconnected from fundamental historical values,

3) A global banking industry that can best be described as fragile and is realistically insolvent if the accounting games were to be removed.

I think most would agree that massive public, private and consumer debt levels are a central problem to the current global predicament. We also however need to appreciate that these massive debt build ups have also allowed the over-building of production capacity. We have global supply that is now outstripping demand. The output gap in the US alone would require a theoretical -7% Fed Funds rate according to the Taylor Rule (6).

EXCESS CAPACITY

The currency wars are being fought because global players are being forced to fight for a piece of the global demand pie that is growing at a slower rate (a first derivative problem) versus the capacity presently available and coming online. The Asian buildup of production capacity is nothing short of startling but it is premised on a free spending and 70% consuming US economy. A slowdown in the US and a weakening US dollar are major threats to political and social stability in the Asian export economies. Everything in the mercantile, export led Asian economies must be done to avoid this. The facts however are that there are no longer sufficient jobs in America to support past and present levels of consumptions. The middle class in America is quickly becoming extinct and with it the ability to famously ‘shop till they drop’.

What are the US politicos to do? The well recognized Michael Hudson asserts in Why the U.S. Has Launched a New Financial World World War:

“Finance is the new form of warfare – without the expense of a military overhead and an occupation against unwilling hosts. It is a competition in credit creation to buy foreign resources, real estate, public and privatized infrastructure, bonds and corporate stock ownership. Who needs an army when you can obtain the usual objective (monetary wealth and asset appropriation) simply by financial means? All that is required is for central banks to accept dollar credit of depreciating international value in payment for local assets. Victory promises to go to whatever economy’s banking system can create the most credit, using an army of computer keyboards to appropriate the world’s resources. The key is to persuade foreign central banks to accept this electronic credit.

U.S. officials demonize foreign countries as aggressive “currency manipulators” keeping their currencies weak. But they simply are trying to protect their currencies from being pushed up against the dollar by arbitrageurs and speculators flooding their financial markets with dollars. Foreign central banks find them obliged to choose between passively letting dollar inflows push up their exchange rates – thereby pricing their exports out of global markets – or recycling these dollar inflows into U.S. Treasury bills yielding only 1% and whose exchange value is declining. (Longer-term bonds risk a domestic dollar-price decline if U.S interest rates should rise.)

What is to stop U.S. banks and their customers from creating trillion, trillion or even trillion on their computer keyboards to buy up all the bonds and stocks in the world, along with all the land and other assets for sale in the hope of making capital gains and pocketing the arbitrage spreads by debt leveraging at less than 1 per cent interest cost? This is the game that is being played today.”

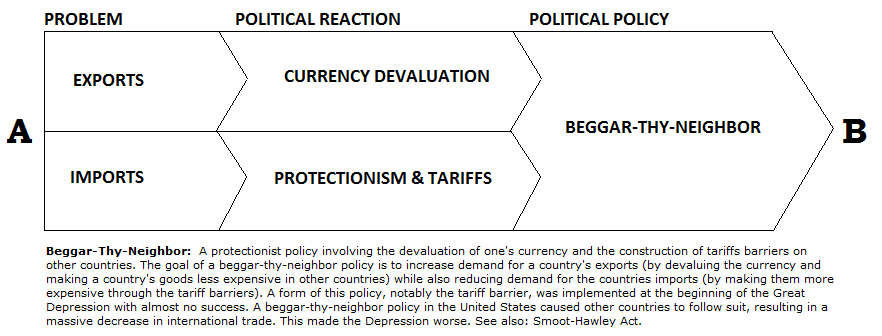

The chart below was published in early spring of this year specifically spelling out that a ‘Beggar-thy-Neighbor’ roadmap lay ahead.

WINNERS & LOSERS IN A CURRENCY WAR

How could I have been so sure when I put this chart together? The realistic fact about wars are that there are winners and losers. These however are not the people on the battlefield. Since Caesar, wars are about money. The winners are those who finance them and the losers are those that pay for them. Rich banking families are well documented to have financed both sides. It matters not much who wins but rather that a war is fought so money is made.

So who actually wins in a currency war? The answer is found by forensically following the money.

EVERY WAR COMES WITH NEW TECHNOLOGY

The most effective way of following the money is to consider the major new innovations in the financial world. Like all wars the winner is the one who innovates the ‘combat technology’ the fastest.

We need to remember that the financial innovations discovered during and after the financial crisis such as: Collateralized Debt Obligations (CDOs), Credit Default Swaps (CDSs), Structured Investment Vehicles (SIVs), Special Purpose Entities (SPE’s) and a raft of securitization products were the foundations upon which were built the “Toxic Assets” and the reason for the global financial crisis. The toxic assets were the catalyst which we continuously heard referred to during the crisis which forced the government into massive public debt government spending in an apparent attempt to avoid a financial collapse.

If we examine the latest raft of new weaponry, we can easily see where this is headed, how the money will flow, who wins and unfortunately who loses.

1- FIAT PAPER BOMBERS - Quantitative Easing

Quantitative Easing is an euphemism for printing money. The US has embarked on a massive untested trial in recklessly printing money.

2- CURRENCY MISSILES - US$ Carry Trade

Like the hydrogen bomb was to the early atomic bomb, the US$ Carry Trade is to the original pilot Japanese Carry Trade. IF QE are the bombs, then the US dollar carry trade are the missiles that deliver the bombs. With borrowing costs in the US approaching zero, a weakening carry currency and unlimited money creation, we have the perfect carry trade missile that can and will hit any economy in the world.

3- REGULATORY ARBITRAGE - Guarantees and Contingent Liabilities

I have written extensively how the financial crisis has served as a vehicle to shift debt obligations from the banking and private sector to the public sector. This has been achieved through government guarantees, the use of balance sheet contingent liabilities and interest rate / currency swaps. It is the battlefield strategy of Regulatory Arbitrage.

ARTICLES: SULTANS OF SWAP: Smoking Guns! , SULTANS OF SWAP: The Sting! , SULTANS OF SWAP: The Get Away!

4- PUBLIC PRIVATE PARTNERSHIPS / PRIVATE FINANCE INITIATIVES – PPP/PFI

The extensive hidden use of Public Private Partnerships & Private Finance Initiatives (PPP/PFI) recently came to light during the European Sovereign debt crisis. This tool has become the guidance system for missile delivery since it allows the conversion of freshly printed fiat paper into real, unencumbered, revenue producing assets.

ARTICLES: SULTANS OF SWAP: Explaining 5 Trillion in Derivatives! , SULTANS OF SWAP: Smoking Guns!

5- AN UNREGULATED 5 TRILLION – Derivative Swaps

The unregulated, off balance sheet, offshore, non exchange traded, private SWAP vehicle is the ideal vehicle with which to control global financial markets. The Sultans of Swaps now operate much as the Bond Vigilantes did at one time but with different control and much different motives. The growth of the SWAP market in interest rate and currency swaps effectively muzzled and obsoleted the Bond Vigilantes of yesteryear.

ARTICLES: SULTANS OF SWAP: Explaining 5 Trillion in Derivatives!

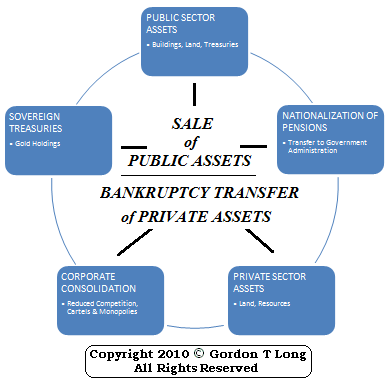

HOW THE MONEY WILL BE MADE – Paper Assets Exchanged for Real Assets

1- TAKE OVER PUBLIC SECTOR ASSETS – buildings, land, treasuries.

2- TAKE OVER PRIVATE SECTOR ASSETS - land and resources.

3- TAKE OVER OF SOVEREIGN TREASURY – transfer of sovereign treasury gold holdings

4- MAJOR CORPORATE CONSOLIDATIONS - reduced competition, reduced monopoly laws and emergence of cartels

5- NATIONALIZATION OF PRIVATE & PUBLIC PENSIONS - government grab of financial assets

REAL WEALTH

The financiers of the currency wars understand that real wealth in its most simplistic essence can only be created by:

1- GROWING IT

2- MINING IT

3- BUILDING IT

Paper money is simply a tool for the trading of wealth. When money is backed by a hard asset then it also becomes a store of that wealth. However that is not the case with fiat currencies. Though Gold is real wealth it does not grow wealth, but rather stores it or protects it from the debasement of paper ‘trading’ instruments. Ideal real wealth is wealth that continues to grow and yet maintains its inherent value. Over the longer term it is usually better to own well managed, unencumbered agricultural producing land, producing mines and production facilities than just the wealth product they output. The Rothschild banking family learned this hundreds of years ago and is the reason why they moved from solely owning gold to energy, mining, agriculture and selective base materials process production.

FLAWED PUBLIC POLICY DECISIONS ASSURE THE OUTCOME

FLAWED PUBLIC POLICY DECISIONS ASSURE THE OUTCOME

One mistake after another has been made in an attempt to ‘kick the can down the road’ and avoid the inevitable necessity to restructure the debt. Unfortunately when it is restructured it will be at the expense of the public and not the original parties. The cost to the tax payer will be insurmountable debt and the forced surrender of pubic assets. Public assets that in the future will be charged for by ’Private Banking’ and Special Purpose Entity (SPE) owners.

=> BAILOUTs: Banks, AIG, GM, Fannie Mae / Freddie Mac

=> ZIRP

=> TARP & ARRA

=> HAMP, Cash for Clunkers etc.

=> Extend & Pretend Accounting

=> QE I (Buying .7B in Mortgage & Treasury Products)

=> QE II

TIMING

Like a well oiled machine the sequence of events continue to unfold as laid out in my Extend & Preserve article series. The implementation of Quantitative Easing (QE I) and change in GAAP Mark-to-Market accounting treatment ignited the initial rally leg. With further refinements (see EXTEND & PRETEND - Manufacturing a Minsky Melt-Up) it continued until it became evident that the US employment and GDP were not improving in any meaningful manner despite T of Spend, Lend and Guarantee initiatives. Then as the polarization of the EU wanting ‘austerity’ policies versus the US wanting ‘stimulus’ measures, the US dollar began weakening and stocks stopped their retracement in June. When Bernanke signaled QE II in August the financial markets were once again ignited and the US dollar weakened further. The financial markets are now propelled by both euphoria and fear of more liquidity being made readily available. It will not end well as we naively get caught in the spider’s carefully laid out trap.

CONCLUSION

An interesting fact is that the US has positioned itself for this war as a result of the spending on previous wars. According to Michael Hudson (5):

“What destabilized the system was war spending. War-related transactions spanning World Wars I and II enabled the United States to accumulate some 80 per cent of the world’s monetary gold by 1950. This made the dollar a virtual proxy for gold. But after the Korean War broke out, U.S. overseas military spending accounted for the entire payments deficit during the 1950s and ‘60s and early ‘70s. Private-sector trade and investment was exactly in balance.

By August 1971, war spending in Vietnam and other foreign countries forced the United States to suspend gold convertibility of the dollar through sales via the London Gold Pool. But largely by inertia, central banks continued to settle their payments balances in U.S. Treasury securities. After all, there was no other asset in sufficient supply to form the basis for central bank monetary reserves. But replacing gold – a pure asset – with dollar-denominated U.S. Treasury debt transformed the global financial system. It became debt-based, not asset-based. And geopolitically, the Treasury-bill standard made the United States immune from the traditional balance-of-payments and financial constraints, enabling its capital markets to become more highly debt-leveraged and “innovative.” It also enabled the U.S. Government to wage foreign policy and military campaigns without much regard for the balance of payments.”

We don’t need to go into the additional costs of the wars in Iraq and Afghanistan, Homeland Security (War on Terror) and military base expansion into 130 countries which have exploded the US fiscal deficits. Suffice it to say that these and all wars since Vietnam are wars that have been conducted without increasing taxes – a historical first which draws little attention or concern.

The present fiat currency system will end based on the strategy of Debase, Default and Deny! It is my opinion that it will be replaced by a system structured on the IMF and BIS’s Strategic Drawing Rights (SDRs) partially backed by precious metals. The question to be asked however is not what will be the replacement for fiat currency, but who will have ownership of the assets after this war ends? Who will pay the requisite ‘tribute’ that goes to the victors?

“Fiat Paper Bombers Spotted Overhead!!”

Sign Up for the next release in the Currency Wars series: Currency Wars

Follow developments in the Currency Wars daily at Tipping Points

SOURCES:

(1) 10-25-10 Trade of the Decade: The Power Elite's Grand Strategy Of Two Minds

(2) 10-04-10 Economic Measures Continue to Slow Hussman Funds John P Hussman Ph.D.

(3) 10-11-10 No Margin of Safety, No Room for Error Hussman Funds John P Hussman Ph.D.

(4) 01-19-10 Bernanke’s Sorcery Will Fail Arun Motianey

(5) 10-11-10 Why the U.S. Has Launched a New Financial World World War Michael Hudson

(6) 10-27-10 The Fed's impending blunder Ambrose Evans-Prichard Telegraph.co.uk

Gordon T Long

Mr. Long is a former senior group executive with IBM & Motorola, a principal in a high tech public start-up and founder of a private venture capital fund. He is presently involved in private equity placements internationally along with proprietary trading involving the development & application of Chaos Theory and Mandelbrot Generator algorithms.

Gordon T Long is not a registered advisor and does not give investment advice. His comments are an expression of opinion only and should not be construed in any manner whatsoever as recommendations to buy or sell a stock, option, future, bond, commodity or any other financial instrument at any time. While he believes his statements to be true, they always depend on the reliability of his own credible sources. Of course, he recommends that you consult with a qualified investment advisor, one licensed by appropriate regulatory agencies in your legal jurisdiction, before making any investment decisions, and barring that, you are encouraged to confirm the facts on your own before making important investment commitments

© Copyright 2010 Gordon T Long. The information herein was obtained from sources which Mr. Long believes reliable, but he does not guarantee its accuracy. None of the information, advertisements, website links, or any opinions expressed constitutes a solicitation of the purchase or sale of any securities or commodities. Please note that Mr. Long may already have invested or may from time to time invest in securities that are recommended or otherwise covered on this website. Mr. Long does not intend to disclose the extent of any current holdings or future transactions with respect to any particular security. You should consider this possibility before investing in any security based upon statements and information contained in any report, post, comment or recommendation you receive from him.