Today the Institute for Supply Management published its monthly Manufacturing Report for February. The latest headline PMI was 49.5 percent, an increase of 1.3 percent from the previous month and above the Investing.com forecast of 48.5.

Here is the key analysis from the report:

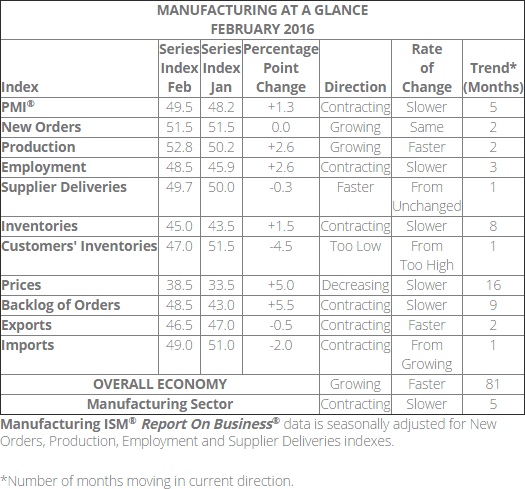

"The February PMI® registered 49.5 percent, an increase of 1.3 percentage points from the January reading of 48.2 percent. The New Orders Index registered 51.5 percent, the same reading as in January. The Production Index registered 52.8 percent, 2.6 percentage points higher than the January reading of 50.2 percent. The Employment Index registered 48.5 percent, 2.6 percentage points above the January reading of 45.9 percent. Inventories of raw materials registered 45 percent, an increase of 1.5 percentage points above the January reading of 43.5 percent. The Prices Index registered 38.5 percent, an increase of 5 percentage points above the January reading of 33.5 percent, indicating lower raw materials prices for the 16th consecutive month. Comments from the panel indicate a more positive view of demand than in January, as 12 of our 18 industries report an increase in new orders, while four industries report a decrease in new orders."

Here is the table of PMI components.

The ISM Manufacturing Index should be viewed with a bit of skepticism for various reasons, which are essentially captured in Briefing.com's Big Picture comment on this economic indicator.

This [the ISM Manufacturing Index] is a highly overrated index. It is merely a survey of purchasing managers. It is a diffusion index, which means that it reflects the number of people saying conditions are better compared to the number saying conditions are worse. It does not weight for size of the firm, or for the degree of better/worse. It can therefore underestimate conditions if there is a great deal of strength in a few firms. The data have thus not been either a good forecasting tool or a good read on current conditions during this business cycle. It must be recognized that the index is not hard data of any kind, but simply a survey that provides broad indications of trends.

The chart below shows the Manufacturing Composite series, which stretches back to 1948. The eleven recessions during this time frame are indicated along with the index value the month before the recession starts.

For a diffusion index, the latest reading of 49.5 indicates contraction and the fifth month in a row. What sort of correlation does that have with the months before the start of recessions? Check out the red dots in the chart above.

How revealing is today's 1.3 point change from last month? There are 818 monthly data points in this series. The absolute average month-to-month point change is 2.0 points, and the median change is 1.5 points.

Here is a closer look at the series beginning at the turn of the century.

To reiterate the Briefing.com assessment: "The data have thus not been either a good forecasting tool or a good read on current conditions during this business cycle." The ISM reports nevertheless offer an interesting sidebar to the ongoing economic debate.

Note: This commentary used the FRED USRECP series (Peak through the Period preceding the Trough) to highlight the recessions in the charts above. For example, the NBER dates the last cycle peak as December 2007, the trough as June 2009 and the duration as 18 months. The USRECP series thus flags December 2007 as the start of the recession and May 2009 as the last month of the recession, giving us the 18-month duration. The dot for the last recession in the charts above are thus for November 2007. The "Peak through the Period preceding the Trough" series is the one FRED uses in its monthly charts, as illustrated here.

You may also like:

Book Interview: “The Industries of the Future” With Alec Ross