Editor's note: Click on any image in this editorial to enlarge.

A working paper published by the Economics Department of the Organization for Economic Cooperation and Development (OECD) last week examined the long term trends that are driving global crude oil supply and demand levels and hence influencing oil prices. OECD is composed of 34 developed countries. The Organization promotes global economic growth and trade. The OECD study concluded that:

“A return to world [economic] growth to slightly below pre-crisis rates would be consistent with an increase in the price of Brent crude to far above the early-2012 levels by 2020. This increase would be mostly driven by higher demand from non-OECD economies – in particular China and India. The expected rise in the oil price is unlikely to be smooth. Sudden changes in the supply or demand of oil can have very large effects on the price in the short run.”

Projecting oil prices is difficult according to the study. The researchers note there is a case to be made for surging demand, especially in emerging economies. Rapidly rising demand, and increasing prices, could adversely impact future economic growth.

The study contained a number of interesting charts:

With the global economic collapse associated with the Great Recession oil prices fell sharply in 2008 from record levels. The OCED study points out that as global economic growth has resumed the price of crude oil has recovered and stabilized just over 0 a barrel. The underlying demand for the commodity has also recovered and is now at record levels.

With the global economic collapse associated with the Great Recession oil prices fell sharply in 2008 from record levels. The OCED study points out that as global economic growth has resumed the price of crude oil has recovered and stabilized just over 0 a barrel. The underlying demand for the commodity has also recovered and is now at record levels.

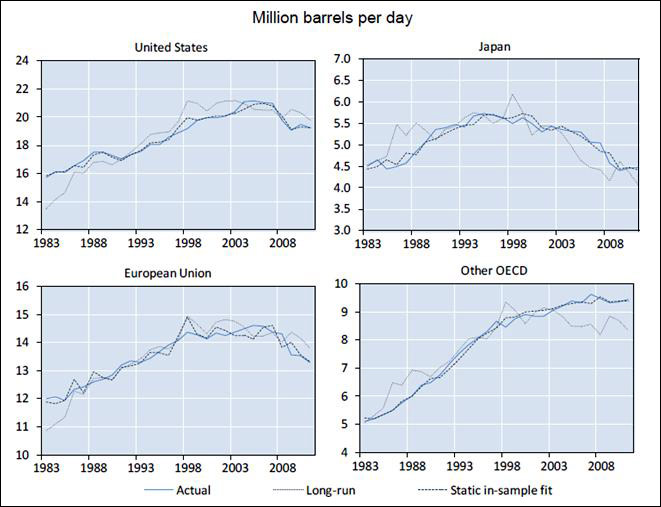

Most of the incremental demand growth for crude oil has originated in China and in the less developed non-OCED countries. The chart at right represents demand changes in the 2001 to 2010 period, but the long term trend continues. Demand in the U.S. and in OCED countries (including Europe and Japan) actually declined during this time period.

Conventional oil discoveries are falling short of global production levels. Discoveries far outpaced production until around 1980. Since that date production has exceeded conventional discoveries.

Unconventional shale oil and tar sands development have made up for some of this shortfall, although in general these resources require higher oil prices to make them economic.

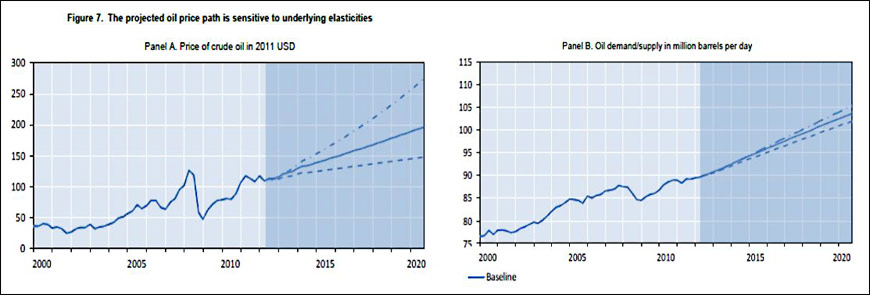

Based on the OCED model future global oil demand and prices were forecast as follows:

The report also noted that even a small (one percent) sudden decrease in oil supply would have a major impact on oil prices. And they ran sensitivity analysis on assumed economic growth rates and crude oil price response (see chart below).

The following main conclusions emerged from the OCED analysis:

- World oil demand rose markedly in the decade to 2010 as improvements in energy efficiency did not offset the upward pressure from a growing world population and rising per capita income levels in developing countries.

The costs of oil exploration and production, both to operate current capacity and develop new supply, rose substantially as new resources became more costly to access.

The costs of oil exploration and production, both to operate current capacity and develop new supply, rose substantially as new resources became more costly to access.

- Oil demand responds very little to price changes in the short run. In more than half of the countries and regions considered the short-run price elasticity is not significantly different from zero. Oil demand is somewhat more responsive to prices changes in the medium to long run.

- Oil demand in developed OECD countries has stagnated, and in some cases is declining (see charts of historical demand above)

- Fast growing non-OCED economies are less energy efficient. On average across countries, a one per cent rise in real GDP pushes up oil demand by half a per cent in OECD countries over the medium to long run, whereas the figure is closer to unity for most non-OECD countries.

- Predictions of future oil prices are inherently difficult to make. A return of world economic growth to slightly below pre-crisis rates would be consistent with an increase in the price of Brent crude far above early-2012 levels.

- Based on plausible demand and supply assumptions there is a risk that prices could go up to anywhere between 0 and 0 dollars per barrel in real terms by 2020 depending on the responsiveness of oil demand and supply. These projections account for a negative feedback effect of higher oil prices on economic growth.

- The crude oil price increase forecast above would be associated with a rise in total oil supply of around 14 million barrels per day. The additional supply is likely to come from unconventional resources such as Canadian oil sands and U.S. oil shale. If oil supply were to increase by 2 million barrels per day less than in the baseline the oil price would increase by per barrel.

- A phasing out of fossil fuel subsidies to consumers in non-OECD countries would reduce the projected price increase.

- Demand growth from China, India, Indonesia and the developing world will be extremely high over the next decade. This will by far outweigh any decline in consumption seen in the in the U.S., Japan, and European countries (see charts of historical demand at right).

- The projected oil price is sensitive to world economic growth. If both OECD and non-OECD economies grew each year one percentage point more than in the baseline scenario, the analysis suggests that the oil price could end up about $40 per barrel higher in 2020.

- A trend increase in oil prices would not necessarily be smooth as sudden changes in the supply or demand of oil can have very large short-run effects on the price.

Investment implications – Assuming the OECD study is correct with regard to the upward long term direction of both oil demand and prices, petroleum reserves in the ground in politically secure areas of the world should increase in value. The aggressive monetary easing now seen in many central banks should also keep prices of commodities and real assets higher than they have been historically and uptrending.