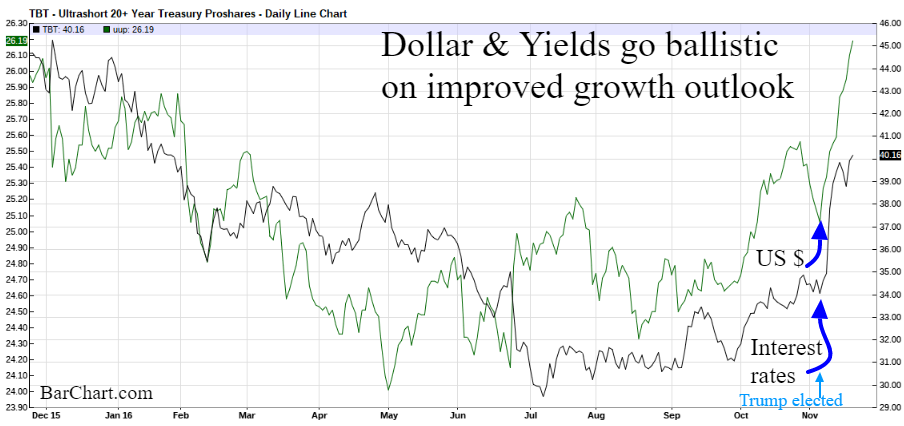

The confidence of a “big league” fiscal stimulus by President Trump in 2017 has sent shock-waves through our financial markets and seismic shifts in the political landscape around the world tilting Trump. Trepidation remains, but the rhetoric has turned from radioactive to magnetic as the populist nerve captured by Trump is being mirrored in France and Italy. Commensurate with the resplendent stock market records and faster economic growth rates are the surging interest rates on elevated inflation expectations. A “yuuge” beneficiary of rising yields is the banking sector. After 2 years of stagnant earnings, the bank stocks have blasted off on the election day with a supreme conviction that the long anticipated secular rise in bank net margin profits from rising interest rates has begun. Until inauguration day on January 20th or beyond it may be challenging to find corrections to surf this Bull wave. Look for a “modest” pullback in the week prior to or just after the assured Fed Funds rate hike December 14th if seeking a better entry.

Intuitively the US Dollar has surged on the expectation that the US infrastructure boom will attract capital supporting currency appreciation versus our trading partners. US yields rising faster than foreign yields is supportive for the Dollar, but we expect this surge will stall in the next couple of months as reality falls short of the markets fantastic forecast. A stronger Dollar is not only good for US bank stocks but most large cap domestic companies that produce their product in the US. A rising dollar implies more costly imports, thus US revenue-based companies should outperform. Investors remain 95% exposed to equities.

Our US Dollar moves inversely to commodities in general as it signals building deflationary pressures. However, this election season is unique. Since June the industrial metals have been inflating while the rising dollar has been hinting deflation. The less speculative industrial metals are surging higher in anticipation of accelerating demand for US infrastructure – think roads, bridges and power grids. These markets can remain in rare harmony until a bit after the January inauguration, but we suspect the dollar will reverse course in 2017.

We all know that energy and crop prices and even precious metals have been lackluster the past 4 months, while base industrial metals like zinc and aluminum have taken a shine to Trump’s towering rhetoric. Once the US Dollar stops rising, the rest of the commodity markets should begin to join the party. Wheat and Corn should rise from their prolonged bases in 2017 when the Dollar peaks.

Political pundits and apolitical money managers are equally split on the veracity of a Trumpian economic boom. We would note that current excess capacity utilization rates, low productivity, and capital investment flows can accommodate policy-induced fiscal stimulus and accelerating GDP without near-term overheating. What the global economy can’t handle are rising trade barriers. Let’s hope Trump surprises economic forecasters as much as he astonished virtually all election experts who were living in an alternate reality. Short-term we may witness minor stock market corrections in early to mid-December as the Fed rate hike approaches and later in the first quarter when the markets anticipate the filibuster blockade being erected by Democrats. Despite some irrational exuberance building, we expect a lucrative investment environment led by banks, industrial and energy stocks.

Related podcast: Kurt Kallaus on What Commodities Are Saying About the US, Global Economy