Introduction to the GSR

Today I want to take a deep look at the global biofuels picture, drawing mainly from the Renewables 2014 Global Status Report (GSR) that was released in June by REN21, the Renewable Energy Policy Network for the 21st Century. I had intended to draw data primarily from the recently released Statistical Review of World Energy 2014, but I believe that the GSR is the most comprehensive report available when it comes to the global renewable energy picture. The GSR has more complete renewable energy data than the BP Statistical Review, but both reports complement each other. Full disclosure, however, I have been a contributor to the GSR for the past five years.

Before I begin, let me introduce REN21 and what are they trying to achieve. From the foreword to the 215-page report:

REN21 is the global renewable energy policy multi-stakeholder network that connects a wide range of key actors. REN21’s goal is to facilitate knowledge exchange, policy development and joint action towards a rapid global transition to renewable energy.

REN21 brings together governments, nongovernmental organisations, research and academic institutions, international organisations and industry to learn from one another and build on successes that advance renewable energy. To assist policy decision making, REN21 provides high quality information, catalyses discussion and debate and supports the development of thematic networks.

With that introduction, let’s do a deep dive on the global biofuel picture.

Ethanol

Global biofuel production falls primarily into three categories; ethanol, biodiesel, and hydrotreated vegetable oil (HVO), also known as “green diesel.” Of the 30.8 billion gallons (116.6 liters) of biofuel produced globally in 2013, 23 billion gallons (75%) were ethanol.

Ethanol is the second simplest alcohol, with only two carbon atoms, and is used as a gasoline substitute and additive. (Methanol, with a single carbon atom, is the simplest alcohol.) Ethanol is produced from fermenting the sugars or starches in feedstocks like corn, wheat, and sugarcane. It is primarily used as a 10% blend with gasoline in hundreds of millions of vehicles worldwide, and more than 20 million vehicles globally are capable of running on either pure ethanol or a blend of 85% ethanol and 15% gasoline. If you own a vehicle in the U.S., it is almost certain that you have operated that vehicle on a 10% ethanol blend at some point.

Ethanol has some key differences from gasoline. First, the energy density is only about two-thirds that of gasoline, which means that a greater volume of ethanol is required to travel an equivalent distance. Ethanol will also absorb water from the air. This can be an issue when transporting or storing ethanol, as well as when using ethanol blends in boats. On the plus side, the octane rating for ethanol is higher than for gasoline. Octane rating is a measure of the tendency of a fuel to pre-ignite when it is compressed. Higher-octane fuels are more resistant to pre-ignition, which allows them to be used in an engine with a higher compression ratio (which enables higher efficiency than engines with lower compression ratios).

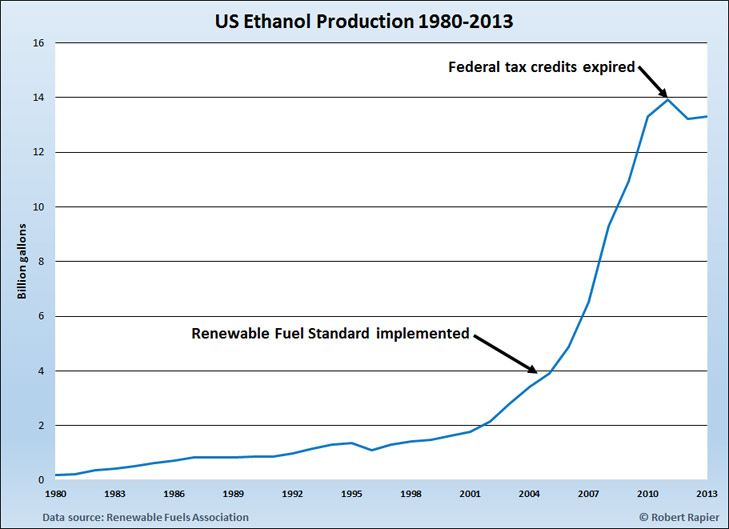

When it comes to ethanol production, the U.S. and Brazil dominate the market, cumulatively accounting for 87% of the global total. In 2013 the U.S. produced 13.2 billion gallons, which was 57% of total global ethanol production. Brazil produced another 6.7 billion gallons. Other global producers of ethanol included Argentina, Canada, China, and India.

[Read: Identifying Opportunities in the Energy Sector Using Warren Buffett’s Investment Strategies]

Both countries have a long history of strong government support for the ethanol industry. U.S. government support for ethanol as fuel began with tax credits for ethanol usage with the Energy Tax Act of 1978. The tax credit was an exemption from the federal excise tax on gasoline, and was in place at varying levels until the end of 2011. In addition to the tax credit, the U.S. government made government-backed loans available to ethanol producers for plant construction and implemented an import fee to protect domestic ethanol producers from cheaper ethanol imports (mainly from Brazil).

As a result of the incentives, U.S. ethanol production slowly grew over time, reaching 1.6 billion gallons by 2000 and 3.9 billion gallons by 2005. Then the U.S. Congress gave the industry a huge boost by mandating ethanol usage in the Energy Policy Act of 2005. One of the key provisions of the new energy policy was the Renewable Fuel Standard (RFS). The RFS started with a requirement of adding 4 billion gallons of ethanol to the fuel supply in 2006—just about the amount that was being produced at that time—and initially increased the amount each year to 7.5 billion gallons of ethanol by 2012.

Congress accelerated ethanol adoption with the Energy Independence and Security Act of 2007. The new act required the use of 12 billion gallons of corn ethanol in the U.S. fuel supply by 2010, rising to 15 billion gallons by 2015. To meet their proportional share of that mandate, refiners have been required to purchase Renewable Identification Numbers, or RINs — effectively ethanol consumption quotas — from producers.

Government mandates in Brazil have an even longer history, dating back to 1976. The mandated percentage of ethanol is higher than in the U.S. (it has mostly fluctuated between 20% and 25% for a decade), and car companies there have developed flex-fuel vehicles that can run on varying concentrations of ethanol. Ethanol in Brazil is produced from sugarcane, as opposed to U.S. ethanol, which is almost entirely derived from corn.

Weather and market forces have recently been kind to U.S. ethanol producers, with an expected bumper corn crop lowering the price of their main input, while ethanol prices have been propped up by the high price of gasoline refined from increasingly expensive crude oil. In the long run continued government support is critical for the industry (corn prices will rise again), but in my estimation is unlikely to waver in the U.S..

Biodiesel

Biodiesel is the second largest category of global biofuel, accounting for 6.9 billion gallons globally in 2013 — 22.6% of total biofuel production. Biodiesel is derived from reacting fats like vegetable oil with an alcohol like methanol. The products of the reaction are biodiesel and glycerin.

The chemical structure of biodiesel is distinctly different from that of petroleum diesel. Petroleum diesel is composed of only hydrogen and carbon (hydrocarbons), but biodiesel also contains oxygen. This gives biodiesel somewhat inferior physical and chemical properties compared with petroleum diesel.

A key difference is that biodiesel will gel and freeze at higher temperatures than petroleum diesel. This can cause fuel filters to plug if the biodiesel concentration is too high in cold weather conditions. Thus, biodiesel tends to be blended at much lower levels with petroleum diesel in cold weather, and is unsuitable for aircraft that fly at high altitudes.

On the other hand, biodiesel is relatively easy to produce. Unlike many alternative fuel technologies, biodiesel can be made in a garage from widely available waste cooking grease with minimal equipment or training. Most alternative fuel technologies have much larger capital expenditure and expertise requirements.

[Read: What Happened to Advanced Biofuels? Let Me Explain]

Biodiesel is produced and used in numerous countries around the world, and is the most commonly used biofuel in the European Union. The EU produced 2.8 billion gallons of biodiesel in 2013, 40% of the global total. Many EU countries have biofuel mandates that encourage the use of biodiesel, although some countries have weakened their mandates in recent years over concerns that cultivation of certain biodiesel feedstocks was encouraging deforestation.

As with ethanol, the U.S. was the largest national producer of biodiesel in 2013. U.S. production in 2013 was 1.4 billion gallons, produced primarily from soybeans. Production exceeded the mandate from the RFS, which covers ethanol, biodiesel, and advanced biofuels, and which called for inclusion of 1.28 billion gallons of biodiesel in diesel fuel markets in 2013.

Behind the U.S. in biodiesel production were Germany and Brazil, which increased production by by 16% and 5% respectively in 2013, to 820 million gallons and 766 million gallons. Argentina was the fourth largest producer with 608 million gallons. France was the world’s fifth largest biodiesel producer, but is moving toward reducing its biofuel mandates.

Most of the major biodiesel producers consumed what they produced. China, on the other hand, is a significant consumer of biodiesel, but satisfies most of its demand by importing biodiesel from Southeast Asian countries like Malaysia and Indonesia. In fact, I visited Malaysia several years ago and asked a palm oil producer if the EU’s concerns about the sustainability of palm oil (production of which has caused deforestation in Malaysia and Indonesia) might slow their growth. I was told that China had no such concerns and would buy every drop they could produce.

Hydrotreated Vegetable Oil

Hydrotreated vegetable oil (HVO) has emerged as an attractive alternative to biodiesel in recent years. With this process the same kinds of vegetable oil feedstocks that are used in biodiesel production are reacted with hydrogen in a process called hydrotreating — a common process in the petroleum industry. The products of this reaction are diesel-length hydrocarbons (also known as “green diesel”), with propane produced as a byproduct.

The primary advantage of hydrotreated green diesel over biodiesel is that the product is chemically equivalent to petroleum diesel, so it can be used in diesel engines in any concentration with no modifications. The disadvantage is that the capital costs of hydrotreating equipment are much higher than for the equipment required to produce biodiesel, and thus the process requires larger scale to be economical.

HVO accounted for only 2.7% of global biofuel production (820 million gallons), but grew by 16% in 2013. In 2013 HVO production took place primarily in Europe (475 million gallons), Singapore (238 million gallons) and the U.S. (80 million gallons).

The HVO space is dominated by Finland’s Neste Oil. Neste began developing its hydrotreating technology — called NEXBTL — in 2002, and in May 2007 started up a plant at its Porvoo refinery outside Helsinki, Finland with an initial capacity of 55 million gallons per year of HVO. The feedstock for the HVO refinery is vegetable oil and animal fat, and in 2009 the capacity was doubled to 110 million gallons. In November 2010, Neste commissioned the largest HVO plant in the world in Singapore with a capacity of 245 million gallons per year (800,000 metric tons), and in 2011 started up another 245 million gallon per year HVO refinery in Rotterdam. The Rotterdam facility is Europe’s largest renewable diesel refinery, and to my knowledge this facility and the Singapore plant are the two largest biofuel plants of any kind in the world.

Besides Neste, HVO processes have been developed by Honeywell (NYSE: HON) subsidiary UOP, Syntroleum (recently purchased by Renewable Energy Group), ConocoPhillips (NYSE: COP) and Petrobras (NYSE: PBR). Syntroleum formed a joint venture with Tyson Foods (NYSE: TSN) called Dynamic Fuels LLC, which opened a $150 million facility in Geismar, Louisiana in 2010 with an annual HVO capacity of 40 million gallons per year.

Conclusions

Global biofuel production continues to be dominated by ethanol, and the U.S. is the world’s dominant biofuel producer — leading in both ethanol and biodiesel. HVO is the world’s third largest volume biofuel and its production is growing at a faster pace than the more mature ethanol and biodiesel industries.

Biofuel volumes will continue to be heavily influenced by government policies and subsidies, and some weakening of these policies has hurt both the ethanol and biodiesel industries in several countries. Investors wishing to place their bets on the future of biofuels need to understand the role that governments will play in the future success of these fuels.