Before you start furiously typing out a retort, hear me out. First, I want to make it clear what I am not skeptical about. I am not skeptical about electric vehicles (EVs) continuing to grow rapidly for the foreseeable future. Indeed, I believe that will happen — although growth has slowed in the US in recent years.

I am also not skeptical over the fact that EVs make sense for many people. Indeed, I would buy one myself if I could justify it economically. I have only put about 5,000 miles on my car in the past 2 years, so it’s hard to justify any sort of premium that could be paid off by fuel savings.

See Pound Replaces Oil As Leading Indicator

I am also not skeptical that EVs will get cheaper, and that improvements in batteries will extend their range. I believe tomorrow’s EV will be much better than today’s.

So far, so good. On these three points, I am on the same page with the most rabid EV enthusiast. But I am extremely skeptical about one thing.

I am skeptical that EVs are going to make any dent in our oil consumption in the foreseeable future.

Let me explain why by first examining global crude oil demand growth over the past three decades. In the 32 years since 1984, global crude oil demand has increased by 36 million barrels per day (bpd) – an average annual increase of 1.1 million bpd per year:

Year-over-year crude oil demand declined in only 3 of those 32 years, and in each case bounced back to the historical growth rate very quickly. Further, the average annual increase since 2010 has been well above the historical average at more than 1.5 million bpd per year.

Of course, that’s history, which merely gives us an indication that the long-term trends of oil consumption have been up for a long time. The reason they continue to grow is that growth is being driven by developing countries. Demand in developed countries has been falling (although US gasoline demand is at a record high this year). But that graph admittedly doesn’t necessarily tell us about the future. So we have to look for examples that may give some insight into the future.

You may also like Kallaus: Stocks Nearing Short-Term Peak; Limited Upside for Oil

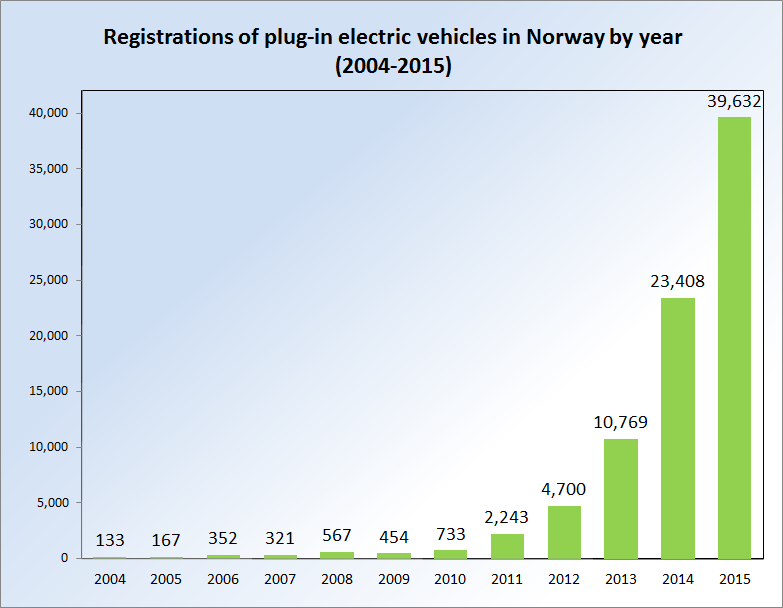

I first give you Norway. Following years of very generous subsidies for EVs, Norway has the largest fleet of plug-in EVs per capita in the world. Norway’s growth rate for EVs has been higher than that of any other country, averaging an amazing 110% per year for the past seven years:

One would expect a decline in Norway’s oil consumption given those trends. After all, Norway is surrounded by members of the European Union (EU), where demand for oil since 2008 is down 14% (primarily in response to much higher oil prices). Nearby countries like Denmark (-14%), Sweden (-16%), and Finland (-21%) all had big declines.

But not Norway. Norway’s consumption has trended slightly higher while all the countries around it experienced double-digit declines in petroleum demand since 2008.

Some may immediately note that Norway’s consumption has been relatively flat for several years, but keep in mind that demand was declining across the developed world in response to 0/bbl oil. So what happened in Norway? Shouldn’t demand there have declined at least as much as in countries that didn’t have explosive EV growth?

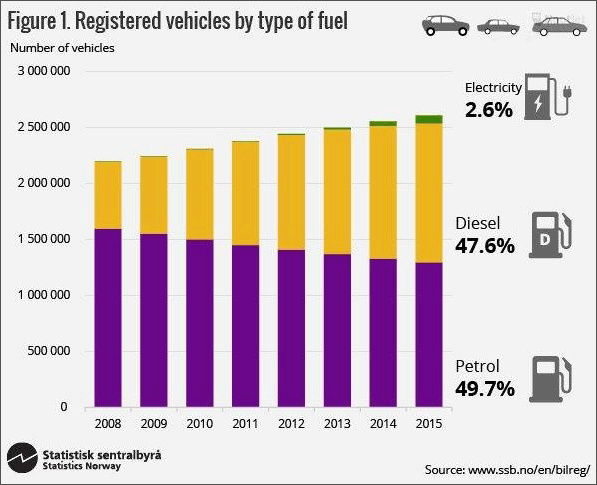

The reason the huge growth in electric vehicles didn’t translate into a reduction in demand in Norway is because it is set against a backdrop of a rising population and a growing fleet of vehicles on the roads (as is the case worldwide). The problem is that the conventional car fleet is adding cars faster than EVs are adding cars:

Also important to note that Norway is adding a lot of diesel engines to the fleet, another factor that helps explain the flattening in their oil demand. But, as the graph shows since 2008 they added about 300,000 diesel and gasoline cars to the roads, but despite the explosive growth in EVs the total over the same time period is only about 80,000 cars. And Norway’s explosive EV growth rate is starting to slow as the country scales back its generous subsidies.

Consider that in the US, from 2014 to 2015, new car sales of conventional internal combustion vehicles increased from 16.5 million to 17.5 million. Yet EV sales in the US actually decreased from 122,438 to 116,099. In other words, they have a very long way to go to even dent the growth in conventional new car sales, much less make an actual reduction in the fleet.

This is essentially the problem with most projections that assume that EVs will soon take a big bite out of oil consumption. The world currently consumes over 90 million barrels per day (bpd) of crude oil. That number is growing by more than 1 million bpd each year, yet most projections fail to account for this growth that is due to increased population, more people driving, etc. Like what happened in Norway. A recent Bloomberg article made this very mistake by assuming that fantastic growth rates in EVs could globally displace 2 million bpd by 2023, and that could crash oil prices. The only problem is that even in the unlikely event that EVs displaced 2 million bpd of petroleum demand by 2023, then global crude oil demand may only be 5 million bpd higher than it is today instead of 7. They assumed it would be 2 million bpd lower than today, again ignoring growth (and the reasons for that growth).

In any case, according to data at Inside EVs, in the US 2016, EV sales year-to-date (YTD) are only about 16% higher than YTD sales a year ago. That would project to maybe an additional 20,000 EVs sold in the US to reach nearly 140,000 for the year. Again, that’s against the backdrop of 2015 sales of 17.5 million conventional cars, which was up a million cars from the previous year.

Globally, EV sales are running 43% ahead of last year’s pace. That’s far behind Norway’s blistering pace that failed to reduce oil consumption, and well behind the 60% growth rate assumed by the Bloomberg article to cause a 2 million bpd drop in demand by 2023. If they assumed a lower growth rate of 45% — still unreasonably high in my view — they don’t impact 2 million bpd of demand until 2028. That’s another 5 years of demand growth for oil, but also importantly another 5 years of depletion of existing fields. Oil demand won’t continue to grow forever because ultimately depletion will catch up and force prices much higher. In that case, what will happen isn’t the price crash that Bloomberg predicted, it’s the exact opposite.

Read The Fuel That May Halt The Electric Car Revolution

We certainly need EVs, but I haven’t seen anyone put together a credible mathematical case that they will even arrest the growth in oil demand over the next decade. Inevitably, they rely on faulty assumptions of fantastic EV growth rates and zero growth for oil — which is contrary to our observations. That’s why I am skeptical. If you project out far enough then indeed you can see EVs making a dent, but that’s far further into the future than proponents like to admit, and oil prices are likely to be much higher — not lower — when that happens.

Link to Original Article: Why I Am Skeptical Of Electric Vehicles