As the euro continues to drift lower, it has become the accepted wisdom that we are headed for parity with the dollar.

Source: barchart.com

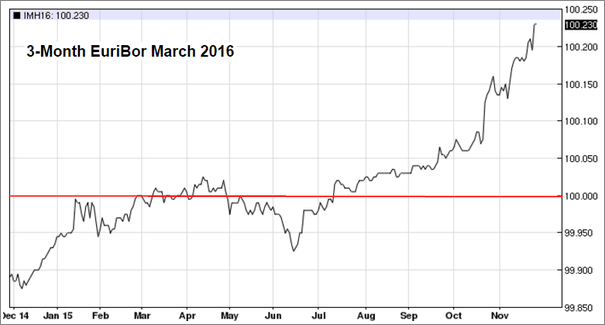

Indeed it is widely expected that the ECB will expand its securities buying program in size, duration and scope (the ECB has been exploring buying municipal bonds for example). The central bank is also expected to cut the benchmark rates, pushing deeper into negative territory. The chart below shows the Euribor futures trading significantly above par as the market expects sharply lower interbank rates.

Source: barchart.com

This of course differs sharply from the monetary policy in the US where markets now assign 70%+ probability of a rate hike next month (as discussed here back in October). There is no question that such divergent policy trajectories should push the dollar lower. But has a great deal of this divergence been priced into the markets?

Read: What Lurks Beneath the Surface – Economic Conditions, a Stronger Dollar, and Global Headwinds

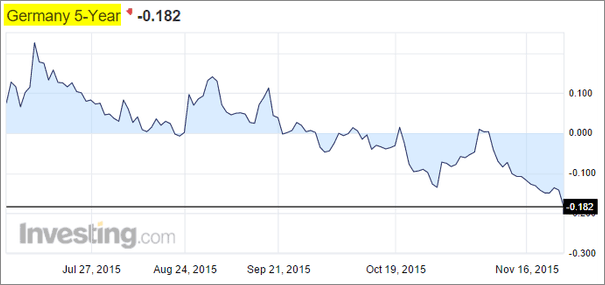

As the Euribor chart (above) shows, the market could now be "priced to perfection". The expectations for a "bazooka" new stimulus from the ECB are also manifested in the record low Eurozone bond yields. For instance, here is Germany's 5-year government bond yield which is clearly pricing in much more demand ahead.

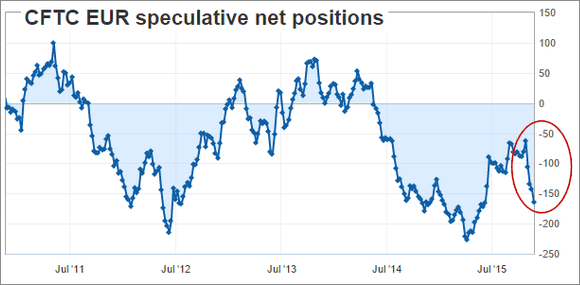

These expectations have resulted in the short euro position becoming a crowded trade once again. The chart below shows speculative accounts' net euro futures positions. What happens if the announcement from the ECB is not quite the "shock and awe" that markets expect?

Source: Investing.com

What could push the ECB to come out with a more modest stimulus increase? Here are some possibilities.

1. In spite of the VW scandal and the Paris attacks, German business sentiment remains strong. The Ifo industrial sentiment exceeded economists' forecasts while the service sector climate hit record highs (below). While the China slowdown certainly created a drag on German GDP growth, the impact has not been as severe as many economists were expecting.

Source: Ifo

2. Moreover, we are seeing significant fiscal stimulus from Germany as the nation's government is addressing the refugee influx.

Source: Deutsche Bank

3. At the Eurozone-wide level we see the composite PMI also beat consensus, touching multi-year highs. The ECB has been known to monitor such PMI indicators.

Source: Markit/Tradingeconomics.com

4. The euro area credit situation is improving, albeit gradually. The deleveraging in the banking system has been over for some time as loan balances continue to grow.

Source: ECB (adjusted for sales and securitization)

We can see signs of stronger bank lending showing up in the Eurozone's broad money supply, which increased more than expected.

Source: Investing.com

5. Finally, the euro area's core CPI rose more than consensus in the latest report. While this is still far from the ECB's target, some central bankers looking at the chart below may want to pause before introducing massive amounts of new stimulus.

Source: Investing.com

This latest core CPI report will therefore increase pressure from some of the more hawkish council members to proceed with a more modest/gradual program when introducing new stimulus.

Jens Weidmann (FT): - The core inflation rate stands at 1% and should gradually increase towards our definition of price stability, which is – let me remind you – a medium-term concept.

Crucially, the decline in oil prices is more of an economic stimulus for the euro area than a harbinger of deflation.

Lower oil prices reduce energy bills for both households and firms. That frees up financial resources which can then be put to use elsewhere – for consumption, investment or for reducing the debt overhang. All of this is good for the economies of the euro-area countries.

There is no question that the fundamentals for the euro remain bearish, especially vs. the US dollar. However, given some of the trends discussed above, a contrarian approach would suggest more caution on that crowded short euro trade.