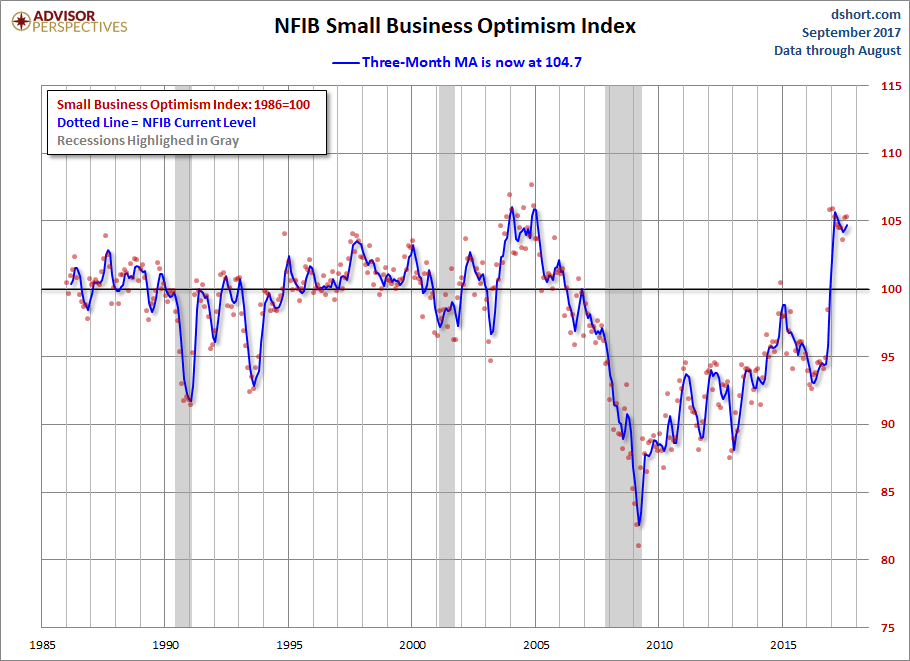

The latest issue of the NFIB Small Business Economic Trends came out this morning. The headline number for August came in at 105.3, up 0.1 from the previous month. The index is at the 97th percentile in this series. Today's number came in above the Investing.com forecast of 105.0.

Here is an excerpt from the opening summary of the news release.

The NFIB Index rose 0.1 points to 105.3. Five of the components increased, while five declined. The lofty reading keeps intact a string of historically high performances extending back to last November.

You may also like Richard Sylla: Human Civilization at Momentous Turning Point With Record Debt Levels and Ultra-Low Interest Rates

The first chart below highlights the 1986 baseline level of 100 and includes some labels to help us visualize that dramatic change in small-business sentiment that accompanied the Great Financial Crisis. Compare, for example, the relative resilience of the index during the 2000-2003 collapse of the Tech Bubble with the far weaker readings following the Great Recession that ended in June 2009.

Here is a closer look at the indicator since the turn of the century. We are now just below the post-recession interim high.

The average monthly change in this indicator is 1.3 points. To smooth out the noise of volatility, here is a 3-month moving average of the Optimism Index along with the monthly values, shown as dots.

Here are some excerpts from the report.

Labor Markets

Small business owners reported a seasonally adjusted average employment change per firm of 0.18 workers per firm over the past three months, virtually unchanged from July.

Inflation

How effective has the Fed's monetary policy been in lifting inflation to it two percent target rate?

The net percent of owners raising average selling prices increased 1 point, rising to a net 9 percent. This is the highest reading since 2014, good news for the Federal Reserve which is trying to generate more inflation.

Credit Markets

Has the Fed's zero interest rate policy and quantitative easing had a positive impact on Small Businesses?

Three percent of owners reported that all their borrowing needs were not satisfied, unchanged and historically very low. Thirty-four percent reported all credit needs met (up 3 points) and 49 percent explicitly said they were not interested in a loan, down 2 points. Including those who did not answer the question, 63 percent of owners have no interest in borrowing, down 3 points.

NFIB Commentary

This month's "Commentary" section includes the following observations and opinions:

Second quarter GDP growth was revised up to 3 percent (annual rate) revealing stronger consumer and private sector spending which raises the odds that the Federal Reserve will raise rates again. With little good news from Washington D.C., it appears that owner optimism is holding at record levels because of private sector activity on Main Street, a reason to hire and build inventories and make capital purchases. Eventually, something will happen to taxes and health care, presumably improving on the current situation, so at least the outcome will not be a negative for owners.

Business Optimism and Consumer Confidence

The next chart is an overlay of the Business Optimism Index and the Conference Board Consumer Confidence Index. The consumer measure is the more volatile of the two, so it is plotted on a separate axis to give a better comparison of the two series from the common baseline of 100.

These two measures of mood have been highly correlated since the early days of the Great Recession. The two diverged after their previous interim peaks, but have recently resumed their correlation. A decline in Small Business Sentiment was a long leading indicator for the last two recessions.