Summary:

- The 10-Yr UST yield has fallen from a high of 3.05% in January to a low of 2.52%

- Low bond yields and stocks near highs are sending conflicting messages

- Although many think this is bearish for stocks, I show why this probably isn't the case

The 10-yr UST yield hit a low of 2.52% today, the lowest level since October of last year and continuing a trend of lower US long-term interest rates that began since the start of the year. Historically, falling bond yields have coincided with falling stock prices and vice versa; so, with the S&P 500 and the Dow Jones Industrial Average sitting near all-time highs, the biggest question right now is why are US Treasury rates still falling? The explanations crossing trade desks and media outlets are usually one or more of the following:

- Geopolitical concerns

- Worsening US growth forecasts

- Arbitrage between U.S. and European debt on ECB stimulus plans

- Rising credibility of the Fed’s ZIRP pledge

Since this has important implications for the stock market, let's now examine each of the four explanations above and see which one holds water.

1. Geopolitical Concerns

One argument for lower bond yields making the rounds is that stock markets have largely ignored the unrest between Ukraine and Russia and are just now beginning to price in the growing geopolitical risk. There are hundreds of commentaries about the unrest between the two countries that argue things will spiral out of control while others are sanguine and think it is a non-event. What does the market tell us? If markets are truly just now pricing in geopolitical risk and beginning to weaken, then would it not be rational to conclude that Russian markets would also be deteriorating? Instead, we see the ruble and Russian stock market showing signs of stabilization. Shown below we see the MSCI Russia Index is up more than 20% from its March lows with the Russian ruble rallying nearly 7% relative to the USD. If tensions were unraveling we would expect to see the Russian stock market and ruble decline as it had in January and February.

Source: Bloomberg

2. Worsening U.S. Growth Forecasts

It is completely rational to think that lower bond yields are occurring as the economy is set to slip as typically bond yields decline when economic prospects worsen and rise when economic growth picks up. Thus, many investors are taking the decline in interest rates as a sign that the economy is set to roll over. However, rather than mirror bond yields, economic activity is supporting the message of the markets. For example, the ISM Manufacturing PMI shows strong directional similarity with the 10-yr UST yield and since January has been heading higher while rates have been falling.

Source: Bloomberg

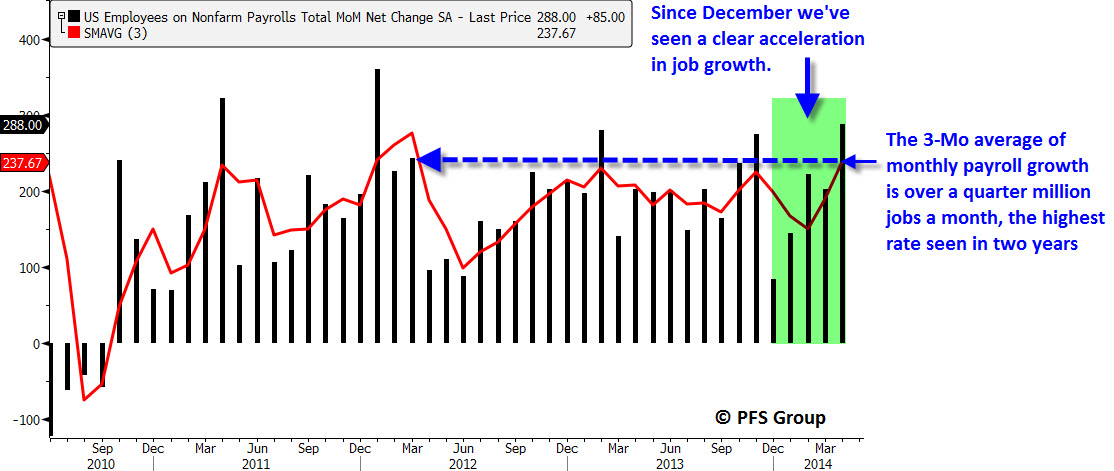

It’s not just U.S. manufacturing that is diverging with bond yields but so has employment data. Since December U.S. payroll growth has been accelerating at the same time, 10-Yr UST yields have been falling.

Source: Bloomberg

If the U.S. economy was truly set to enter a soft patch ahead we would not expect developments like initial jobless claims dropping to a new best for this cycle. We learned today thatInitial jobless claims dropped 24,000 to 297,000 during the week ending May 10, the lowest reported of the expansion so far.

Source: Bloomberg

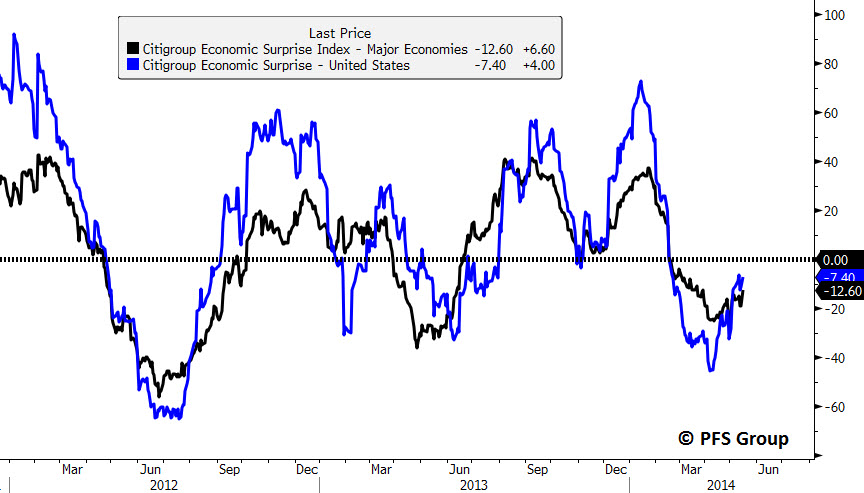

While the argument that yields are falling as economic prospects are worsening may have been a good explanation during the first part of the year, the argument is weakening by the day. The Citigroup Economic Surprise Index for both the U.S. and major economies bottomed in April and has been heading higher as more economic reports have been surprising to the upside.

Source: Bloomberg

A case in point is the Empire Manufacturing PMI for May, which was estimated to be 6.00 and the actual was 19.01. The 19.01 reading beat ALL 51 estimates and was a big positive surprise. I think we can lay to rest the argument weakening economic growth is pushing down rates.

Source: Bloomberg

3. Investors Playing the Arbitrage Between U.S. and European Debt on ECB Stimulus Plans

Yields in Europe have been declining sharply for the last few years I believe for two reasons. The first is that Europe faces a deflationary threat as many country CPI indexes in Europe have turned negative and most, if not all, are below 1% annual inflation rates. In addition to the low inflation rates, I argued in February that the Eurozone economy was set to cool (click for article link). Since that time European economic releases have been surprising to the downside and missing estimates with the Citigroup Economic Surprise Index hitting nearly a 1-yr low.

Source: Bloomberg

The threat of disinflation and a weakening economy is why I made the argument in February and again in April (click for article) as to why the ECB was set to bring out the monetary bazookas, which is the second reason rates in Europe are falling. With weakening economic growth, waning inflation rates, and the prospect of ECB stimulus many investors have front-run the ECB by bidding up European debt. According to a recent Reuters article, the ECB may even start charging banks to hold excess reserves by having a negative deposit rate at the ECB, as highlighted below.

ECB readies package of rate cuts and targeted measures

The European Central Bank is preparing a package of policy options for its June meeting, including cuts in all its interest rates and targeted measures aimed at boosting lending to small- and mid-sized firms (SMEs).

Five people familiar with the measures being prepared detailed plans involving a potential rate cut, including the ECB's deposit rate going negative for the first time, along with the targeted SME measures…

A second source echoed that sentiment, and added: "This will be the first major central bank to move to a negative deposit rate. That would move the exchange rate."

If you invested in European debt back in 2012, you received rates that were 5-6% higher than a comparable U.S. debt on 10-yr bonds when buying Spanish or Italian debt. Similarly, two years ago, German 10-yr bunds were at parity with the 10-yr UST, no longer. Now we’ve seen European peripheral debt yields collapse to near parity with US Treasuries and German bunds yield more than 1% less than US 10-yr bonds as shown below.

Source: Bloomberg

So if you are an aggressive debt investor buying European debt you are no longer being compensated for taking undue risk in buying peripheral European debt like Italy or Spain, and if you are a high-quality debt investor that buys the safe end of the government bond spectrum in Europe, yields are next to nothing in German debt. Thus, it makes sense for both aggressive and conservative debt investors buying European debt to invest in U.S. Treasuries. For the aggressive investor you can get comparable yields and for less risk and for the conservative investor you can get more yield in UST bonds. This, I believe is one of the large factors as to why U.S. Treasury rates are plunging and yet our economy is humming along and the stock market is near its highs.

4. Rising Credibility of the Fed’s ZIRP Pledge

At Janet Yellen’s first testimony as Fed Chairwoman, when asked how long after the Fed ends their purchase program could the Fed Funds be raised she said six months. Markets were unsettled by that but Janet later back peddled and confirmed the Fed’s commitment to keep rates low for a considerable time. Investors took Janet at her word as expectations for higher interest rates in 2015 came down. This can be seen when looking at Fed Futures probabilities for the January 2015 FOMC meeting. Four months ago roughly 25% of investors thought the Fed would have already hiked rates to 0.50% and that has fallen to less than 10%. Notice the big jump in the percentage of investors betting rates will be at 0%, which increased from just over 30% to more than 50%. With investors having a greater belief that the Fed will keep rates low into next year, there is less of a fear of rising interest rates that would hurt bond investors and so we are likely seeing more money come back into the bond market.

Source: Bloomberg

Other Reasons

There was an excellent article in Bloomberg earlier this month that highlighted a more simplistic view as to why U.S. Treasury rates were heading down: simply more demand than supply.

Can’t Find Enough 30-Year Treasuries to Buy? Here’s Why

In a world awash with U.S. government bonds, buyers of the longest-term Treasuries are facing a potential shortage of supply.

Excluding those held by the Federal Reserve, Treasuries due in 10 years or more account for just 5 percent of the .1 trillion market for U.S. debt. New rules designed to plug shortfalls at pension funds may now triple their purchases of longer-dated Treasuries, creating 0 billion in extra demand over the next two years that would equal almost half the 2 billion outstanding, Bank of Nova Scotia estimates…

Pensions that closed deficits are pouring into Treasuries and exiting stocks to reduce volatility after a provision in the Budget Act of 2013 raised the amount underfunded plans are required to pay in insurance premiums over the next two years. It also imposed stiffer fees on those with shortfalls.

In the next 12 months alone, buying from private pensions will create 0 billion in demand for longer-maturity Treasuries, based on Bank of Nova Scotia’s estimates…

Net issuance of interest-bearing Treasuries will fall to 5 billion next year, estimates from primary dealer Deutsche Bank AG show. That’s a 36 percent decrease from last year.

The scarcity will act as a counterbalance to the Fed as it tapers, according to Dominic Konstam, Deutsche Bank’s New York-based global head of interest-rate research.

There truly is an emerging scarcity of long-term U.S. Treasuries as a narrowing in the deficit from tighter spending and higher taxes along with an expanding economy leads to a lower net issuance of Treasuries. The budget surplus of 6.9B seen in April was the third largest monthly surplus seen in this recovery and now the 12-month moving average of the monthly deficit/surplus is at -.6B, much improved from the -3B average seen in early 2010.

Source: Bloomberg

So What Is Driving U.S. Rates Lower?

It’s important to understand what is driving U.S. Treasury rates down as the reason will shape your outlook for the market. If you believe that yields are lower as investors price in greater geopolitical risk and/or a worsening US economic growth forecast, then you would expect the stock market has it wrong and shouldn’t be near its highs and will recouple with bond yields and sell off. However, if you feel it is more of a U.S. and European bond arbitrage and/or more credibility being given to the Fed that they will keep rates low for a long time, then the stock market does not have it wrong and one should not be fearful of falling US interest rates. In addition to the factors making the rounds on trading desks there is also the issue of supply as the U.S. government issues less UST’s to finance its budget.

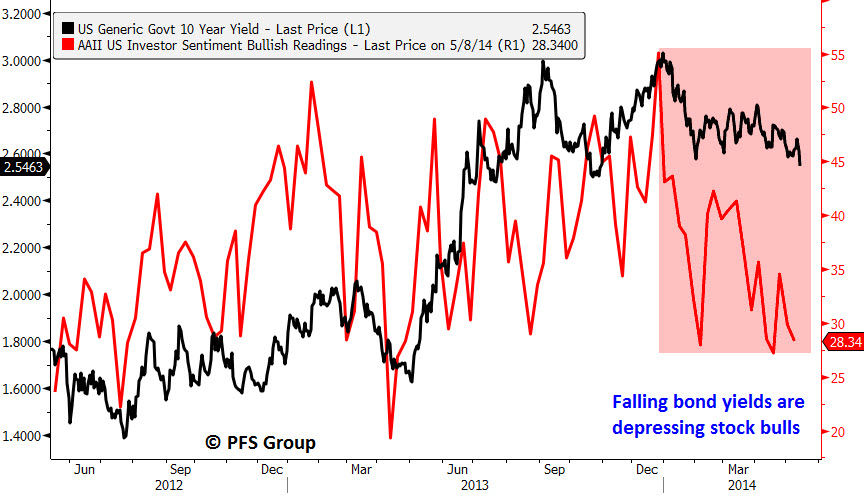

So, while many look at lower rates as a reason to become defensive, they may want to think again since the likely causes for lower rates do not have bearish implications. Moreover, lower rates are helping the market by bringing down overly bullish sentiment. Markets perform best when sentiment is bearish and with AAII % bullish readings near levels that have marked short-term lows in interest rates, we may be near a low in rates and the stock market, with both standing a good chance of rallying in the weeks ahead.

Source: Bloomberg

Summary

In summary, the likely reasons for U.S. Treasury yields selling off do not carry bearish implications for the stock market. As such, the belief that the bond market is signaling a bearish message for the stock market is likely to be proven unfounded. Rather, the bearish sentiment that has coincided with falling bond yields has actually helped provide a bullish support for the market and may now start to act as a tailwind.