Overview:

- Monitoring the credit markets serves as an invaluable risk-management tool

- Junk bond market has been signaling stress, though appears contained to energy

- Record inflows into the energy sector suggest a bottom has not been made

“The essence of investment management is the management of risks, not the management of returns. ALL good portfolio management begins with this premise!” Benjamin Graham, The Intelligent Investor

Perhaps the most important message I learned from the 2007-2009 financial crisis was to listen intently to the message of the credit markets. I learned a lot from reading the articles by the late Bennet Sedacca, a money manager who first blew the credit alarm (click for link) and tragically died just a few weeks after the bear market ended in 2009. He highlighted over and over again the meltdown in the credit markets while everyone in early 2008 was still arguing if we were in a bear market and/or recession. The message was as clear as day for anyone listening and eventually the equity markets crashed.

Looking at the message from the credit markets was not only helpful at providing an early warning to the 2007-2009 crisis but also the 1998 LTCM and Russian Ruble Crisis, the 2000-2003 bear market, the 2011 Euro Crisis, and the US debt downgrade. At every event the credit markets worsened while the stock market marched on, eventually to tumble. This is shown below with the yields on junk bonds shown in red and inverted for directional similarity and the S&P 500 in black. Pay special attention to the place I highlighted in yellow:

Source: Bloomberg

Since the 2007-2009 financial crisis I make it a point to pay attention daily to the credit markets and whenever I see the credit and equity markets out of sync I try to send out the alarm to readers of Financial Sense (see here and here for the most recent examples). What has been bothering me lately is the continued weakness in the junk bond market and the red flag it provides to equity investors.

The biggest culprit for the weakness in the junk bond market is the energy sector, which has been one of the biggest issuers of junk bonds in recent years. While the argument makes sense I wanted to dig a little deeper to see if the warning from the junk bond market was only due to energy or if there was a contagion into other sectors. To do that I took a look at the total returns for the junk bond (AKA: “High Yield”) indices for all ten sectors of the market going back to the start of 2014. What I found was that only a single sector out of the ten had negative returns and that sector was energy (blue line below) while the other sectors ranged from flat to up more than 8%.

Source: Bloomberg

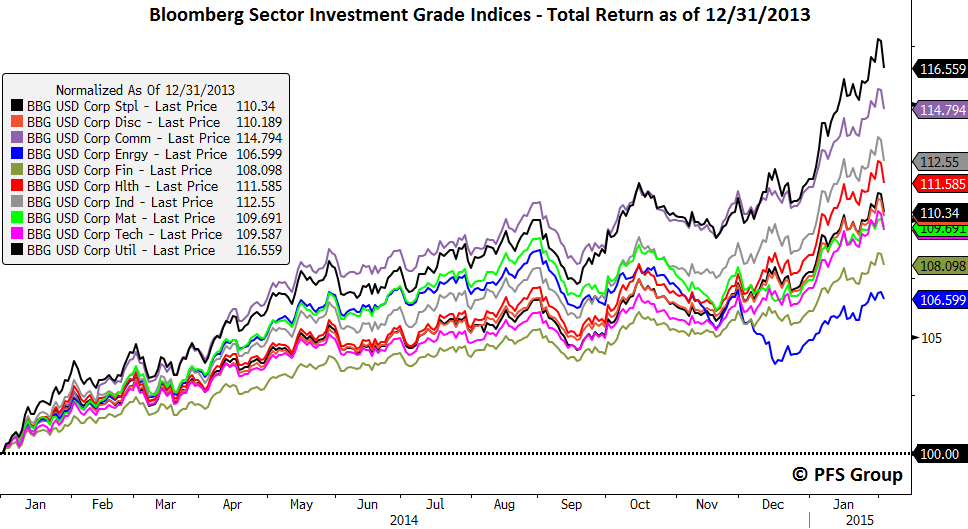

Looking at the investment grade sector indices shows that all ten sectors were up since 2014 with energy posting the weakest gains, though up still over 6%.

Source: Bloomberg

When viewing the message from the corporate bond market of the credit spectrum there is a lack of significant warnings coming from investment-grade bonds and only elevated risk coming from the energy sector for junk bonds. There is no contagion whatsoever from energy into other sectors of the junk or investment-grade sector of the corporate bond markets.

Turning specifically towards the energy sector, some strategists are calling for a bottom in the sector and when viewing money flows there is a tremendous amount of bottom fishing as sentiment towards the sector is turning more optimistic. Typically, capitulation is seen when investors are loathed to even think of an investment and everyone has sold. How is the biggest surge into energy ETFs in years reminiscent of a bottom? The recent spike in inflows looks like what occurred just before the 2014 or 2011 tops.

Source: Bloomberg

When looking at inflows for all ten sector ETFs for the year we see that the energy sector (XLE) has seen the largest inflows to date with investors dumping financials (XLF) and consumer discretionary (XLY).

Source: Bloomberg

I think it is premature to call for a bottom in the energy sector with the credit markets for the sector not showing any signs of life yet. The option adjust spread (OAS, red line below) for the junk bond energy sector is not confirming the recent improvement in the SPDR Oil & Gas Exploration & Production ETF (XOP) which makes the recent improvement in energy equities suspect.

Source: Bloomberg

Summary:

Investors who fail to listen to the message from the credit markets are missing out on an incredible tool that should be in every investor’s tool kit for managing risk. The credit markets have done an invaluable job at flashing warning lights at major market peaks and their message should always be respected. That said, sometimes digging deeper than just what the headline data is saying is warranted as is the current case. We see an understandably significant amount of stress in the energy junk bond market given the slide in oil prices, which is weighing heavily on credit spreads for U.S. junk bond indices and ETFs. Thankfully, so far there is no contagion into other sectors of the market, which softens the warning coming from the overall junk bond market, particularly given there is no weakness in the investment-grade segment of the corporate bond market.

The slide in the energy sector has brought out value investors in waves as we are seeing record inflows, which is not the hallmark of a sustainable bottom that usually occurs when sentiment is overwhelming bearish and devoid of bottom fishers. The lack of bearishness by investors in the sector coupled with the lack of improvement in the energy junk bond market suggests that recent investors into the sector may be playing with fire and a bottom may still elude them.

The bottom line as I see it is that bears using the junk bond market to make their case should soften their resolve and dip buyers into the energy sector should be cautious as the hallmarks of a bottom are not present and the credit markets for the sector are not giving the all clear.