On the home front, times are good. It just doesn't get any better than this. People have jobs. Incomes are rising and the unemployment rate is the lowest in three decades. Signs of prosperity are everywhere. The malls are busy with the bustle of consumers shopping and spending money. Confidence about the future is running high in the New Economy. The housing market is booming, prices are heading up and home ownership has risen to record levels.

On the corporate front, businesses are expanding with plans to hire more workers. Anyone who wants a job can get one. Salaries are generous with the possibility of stock options. Blue collar joins white collar for the first time in owning a piece of the American pie. Until recently stock prices have been rising at a double-digit rate for the last five years. It's not just the value of stock options that has been rising – 401(k) plan values have also been increasing.

Politicians in Washington are ecstatic. Everyone from the President of the United States to the Republican-controlled Congress are claiming credit for America's new-found prosperity. Our success is being heralded as a new U.S. paradigm. Our economic expansion is the longest running expansion on record. Unemployment is the lowest it has been in over three decades. Inflation is nonexistent. Interest rates are historically low. Our stock market has delivered double-digit gains for the last five years and created unprecedented wealth. State governments are running surpluses thanks to capital gains tax revenues. America stands alone as the world's superpower. Overall confidence in America reigns supreme. It runs all the way from Washington to Wall Street to the major capitals around the globe. We are at the peak of our game. We dominate the financial world in the same way that we dominate the battlefield.

Politicians in Washington are ecstatic. Everyone from the President of the United States to the Republican-controlled Congress are claiming credit for America's new-found prosperity. Our success is being heralded as a new U.S. paradigm. Our economic expansion is the longest running expansion on record. Unemployment is the lowest it has been in over three decades. Inflation is nonexistent. Interest rates are historically low. Our stock market has delivered double-digit gains for the last five years and created unprecedented wealth. State governments are running surpluses thanks to capital gains tax revenues. America stands alone as the world's superpower. Overall confidence in America reigns supreme. It runs all the way from Washington to Wall Street to the major capitals around the globe. We are at the peak of our game. We dominate the financial world in the same way that we dominate the battlefield.

As far as the natural eye can see, there are no problems on the horizon. The days are pleasant and the nights almost magical. And even if there were a problem, it would only be a momentary squall. Fed Chairman, Mr. Greenspan, remains the most revered central banker of his day. If a potential problem emerges, there is utmost confidence in his ability to fix it.

What Lies Beneath

“The one lesson history teaches in the financial markets is that there will come a day unlike any other day. At this point the participants would like to say, ‘all bets are off’, but in fact, the bets have been placed and cannot be changed. The leverage that once multiplied income will now devastate principal.” – Martin Mayer, 1999

The economic forecast calls for clear and sunny skies well into the future. No major storms appear on the economic horizon. And yet, beyond the horizon, below the ocean's surface, pressure is building between the tectonic plates that form the peripheral trench systems and adjacent mountain ranges. The pressure between adjacent plates accumulates like an elastic strain and can only be relieved in the form of earthquakes. Those pressure strains give way to a natural phenomenon known as tsunamis. They occur at irregular intervals every 5-15 years. These giant waves can come out of nowhere – often without warning. The sea begins to heave and churn forming waves that are above normal swells. A tsunami can flood breakwaters, tear into harbors and shorelines, and leave widespread destruction in their wake. Because earthquakes are the primary source of tsunamis, they can often go undetected until they erupt.

Due to their initial low heights and long wavelengths, tsunamis can often remain hidden on the radar screen. On the open ocean, tsunamis pose no hazard to vessels at sea. It is only when they hit land that the damage is done. The severity of a tsunami depends on the wave size, its distance from land, and the topography offshore. It affects land regions differently. The greatest damage occurs in populated areas where breakwaters and seawalls can be swept away bringing the full force of the wave upon the shoreline.

One of the characteristics of tsunamis is that they are sudden. One moment the beachfront is sunny and calm. The next moment, an enormous wave appears. Today, special seismographic equipment can pick up earthquakes capable of generating these dangerous tsunamis. Scientists are able to measure wavelength and plot travel and time charts for hitting landfall, giving valuable warning to coastal communities.

- How do earthquakes generate tsunamis? (QuickTime simulation)

- Earthquake-Triggered Tsunami (QuickTime simulation)

The Plates Are Shifting in Our Economy

Today, economic seismographs are picking up tremors in our financial system which are forming in the nation's credit markets. The coming earthquake they are sensing, and one of the distinguishing features of the American economy's recent performance in the 1990's, is the meteoric rise in indebtedness. A greater portion of our GDP (Gross Domestic Product) is being powered by consumption. Capital formation and savings are no longer mobilizing economic growth. Outside the tech sector, there is little capital investment. Personal consumption and debt is driving the economy, rather than savings and investment. The result is that over the last decade, debt in this country has mushroomed from .1 trillion to .8 trillion. [1]

Increasingly, it is taking more and more credit to generate GDP growth. In reality, the American economic miracle is based on easy money, credit, and debt. Debt is expanding at the consumer level and rising at the corporate level. Skyrocketing margin debt has powered the stock market gains of the last year. Our financial system has taken on unprecedented leverage and the greatest portion is being used to feed a speculative frenzy in the financial markets. It is this explosion of credit, which is fueling U.S. economic growth and in the process, inflating a financial bubble. The side affects are the rampant excesses of consumer and business spending that is leading to the rapid accumulation of debt. Much of this debt is speculative and directed toward the financial markets. In short, the consumer has embarked on a borrowing and spending binge. Corporations are accumulating massive amounts of debt to fund mergers and acquisitions and stock buyback programs. Our national and state governments have gone on a spending spree based on boon years of tax revenues.

Money Pressure Is Building

This flood of credit is being generated by an expansion of the nation's money supply. All of the monetary aggregates are expanding at an unprecedented rate. Whether it is the monetary base of the nation's banking system, or the various measures of money as reflected in M2, M3, or MZM, they are all growing at above-average growth rates.

In a capitalistic society, money performs its function as a common medium of exchange. It facilitates the creation and movement of goods within an economic system. Its scarcity and demand determine the cost of money. When the demand for money is great, the cost of money rises. Conversely, when demand is slack, the cost of borrowing drops. The supply of money available to finance trade and economic development comes from savings. It is real savings that generate the funds for capital investment. If not enough savings is available to meet demand, then the cost of money would rise to such a point that the demand would weaken until equilibrium was reached between the forces of supply and the forces of demand. Therefore, variations in the ratio between the supply of money available for credit and the demand for money will ultimately exert an influence on the rate of interest.

Fed-Sponsored Money Flood

When nations save extensively, as in the case of Japan, capital is available for investment and the cost of that capital is low because of its ample availability. However, with the advent of central banking, the cost of money can artificially be influenced. Central bankers can create money out of thin air and inject it into the banking system – essentially expanding the availability of credit and depressing its cost. This is what has happened in America this last decade. (See Part 1: An Introduction) Our financial boom has been based upon a system of leverage of biblical proportion. Credit has expanded through the banking system by a continuous expansion of the nation's money supply by the Fed. It has also expanded outside the banking system through GSEs (Government-Sponsored Entities) such as Fannie Mae and Freddie Mack. These government-sponsored entities have expanded credit between 1997-99 by almost .8 trillion through our securities market in the form of asset-backed securities.

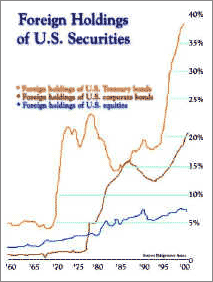

Foreign Capital Helps Credit Expansion

This expansion of credit, through the banking system and through the securities market, has been a substitute for the collapse in personal savings. Adding greatly to this free-flowing credit has been the influx of foreign capital. As a result of the imbalances between the demand for goods and the available supply from domestic producers, the U.S. has been running a record trade deficit. That deficit has been financed by foreign capital, which has been recycled through our securities market. This infusion can be illustrated by the jump in foreign holdings of U.S. Treasury bonds, corporate bonds, and equities.

This expansion of credit, through the banking system and through the securities market, has been a substitute for the collapse in personal savings. Adding greatly to this free-flowing credit has been the influx of foreign capital. As a result of the imbalances between the demand for goods and the available supply from domestic producers, the U.S. has been running a record trade deficit. That deficit has been financed by foreign capital, which has been recycled through our securities market. This infusion can be illustrated by the jump in foreign holdings of U.S. Treasury bonds, corporate bonds, and equities.

The American economy has been the direct beneficiary of the flight of capital that resulted from the Asian meltdown of 1997 and the Russian debt crisis of 1998. Each new international crisis has spawned a demand for U.S. securities in a flight to quality. This movement of capital has further served the purposes of expanding credit as well as fueling the demand for financial assets.

The combination of domestic credit expansion, coupled with foreign financing of our trade deficit has led to a credit expansion that is completely out of control and in danger of toppling the U.S. economy. Kurt Richebächer and other economists from the Austrian School of Economics have recently pointed to the fact that between 1996-99, domestic debt expanded by trillion; while GDP growth increased by only .4 trillion. This amounts to a debt to economic growth ratio of over 4:1. [2] It shows just how dependent our economy and financial markets are on a constant influx of credit and debt fabrication.

Having an understanding of what lies underneath the recent economic boom gives one a better understanding of the outlet for all that financial energy. Just as the shifting of tectonic plates cause tsunamis, today, the Fed has created its own tsunami through the vigorous expansion of the nation's money supply. The potential force of that wave can be measured by the expansion of credit that has worked its way through our economy. In the U.S., it is manifesting through a vast expansion of consumer debt, corporate debt and leverage in our financial markets.

Personal Consumption Shrinks Personal Savings

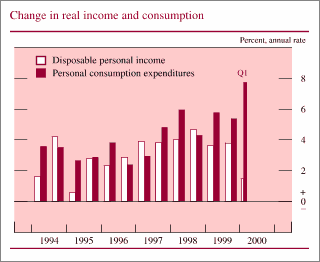

One of the most remarkable aspects of America's economic expansion these past five years has been the evaporation of savings and the vigorous expansion of personal consumption by consumers. An increase in personal income and the degree of wealth created by appreciation in the stock and real estate markets has fueled above-average rates of expenditures in all categories of consumption. As shown in the graph on the left, personal expenditures have outstripped income since 1995. According to the Fed's most recent economic report to Congress, consumer expenditures rose at an annual rate of 7.75%. This represents the sharpest increase since early 1983. Furthermore, it shows no sign of abating. Recent reports for the month of July indicate consumer incomes grew by 0.4%; while spending by consumers grew by 0.5% and consumer debt rose by billion. [3]

One of the most remarkable aspects of America's economic expansion these past five years has been the evaporation of savings and the vigorous expansion of personal consumption by consumers. An increase in personal income and the degree of wealth created by appreciation in the stock and real estate markets has fueled above-average rates of expenditures in all categories of consumption. As shown in the graph on the left, personal expenditures have outstripped income since 1995. According to the Fed's most recent economic report to Congress, consumer expenditures rose at an annual rate of 7.75%. This represents the sharpest increase since early 1983. Furthermore, it shows no sign of abating. Recent reports for the month of July indicate consumer incomes grew by 0.4%; while spending by consumers grew by 0.5% and consumer debt rose by billion. [3]

The current rate of American consumption comes on the heels of two years of very robust spending. Consumption continues to be strong at the retail level. Outlays for big-ticket items from cars, home entertainment systems, personal computers to recreation remain strong. In addition to big-ticket items, spending on consumer services continues to rise at a very brisk pace.

The Wealth Effect

While consumers have been spending beyond their income for the last few years, consumption has been supported by a rapid rise in household net worth. Double-digit gains in the stock market and the appreciation in real estate have tended to make everyone feel wealthier. The wealth effect created by a rise in stock and real estate prices has allowed households to spend beyond their means by taking on more debt and shrinking their personal savings. The personal savings rate has dropped dramatically these last five years. It is now less than one percent. [4]

America on a Debt Binge

Consumer optimism about the future continues to support the spending and debt binge in America. A favorable outlook for income and employment is making consumers confident enough to continue to spend and take on more debt. Even with rising mortgage and consumer loan rates, household debt is still growing at an annual rate of 8 percent. This growth in debt has led to debt levels that are at a record 101% of income. According to a recent article in The Wall Street Journal [5], the average U.S. household now sports 13 credit cards with an average balance of ,500. That is up from ,000 in 1990. It is not unusual to see many consumers carry auto-loan and installment debt balances approaching 0,000.

Consumer optimism about the future continues to support the spending and debt binge in America. A favorable outlook for income and employment is making consumers confident enough to continue to spend and take on more debt. Even with rising mortgage and consumer loan rates, household debt is still growing at an annual rate of 8 percent. This growth in debt has led to debt levels that are at a record 101% of income. According to a recent article in The Wall Street Journal [5], the average U.S. household now sports 13 credit cards with an average balance of ,500. That is up from ,000 in 1990. It is not unusual to see many consumers carry auto-loan and installment debt balances approaching 0,000.

In addition to taking on installment debt, the wealth effect of a rising stock market and a low unemployment rate has encouraged consumers to trade up in the housing market. Low interest rates have enabled Americans to afford bigger homes by taking on larger mortgages. A larger percentage of household income now goes to make house payments. Recently, with mortgage rates rising, home buyers have switched to adjustable rate mortgages which offer lower rates. The hope is that rates will come down when the economy softens. Switching to adjustable rate mortgages has allowed the housing boom to continue to remain strong.

Bankruptcies on the Rise

At one time, debt in this country was only used for making major purchases such as a home or an automobile. This is no longer the case. The stigma of debt or bankruptcy has given way to complacency and acceptance. Americans no longer borrow money just to buy houses. Today Americans use debt for entertainment, vacations, stocks and even groceries. Many baby boomers are paying for their children's education – again with debt. If personal debt levels get too high, consumers find escape from collection agencies by filing bankruptcy. [6]

Lenient bankruptcy laws allow consumers to clear their plate of debt. Once cleared, they can start the process of accumulating debt all over again. There are plenty of banks making generous offers to consumers with great credit card offers. Banks have eased their lending quality during this economic expansion. They see very few signs of credit problems with a booming economy. In fact they are eager to lend. Even my 19-year old son receives free solicitations for credit card enrollment.

Symptomatic Amnesia

In prosperous times, it's hard to foresee the problems beneath the surface should the economy slow down. Today's financial community is suffering from a bad case of amnesia. Banks and financial institutions seem oblivious or have simply forgotten the damaging effects of irresponsible borrowing behavior. A recession, which would increase the rate of unemployment, could make debt burdens unsupportable. In fact a bear market could quickly erase the equity in homes and the personal wealth in stock and mutual fund portfolios. A drop in home values could prompt many borrowers to walk away from their mortgages as they did in the last recession. This time around, however, the mortgages are even bigger and the equity even smaller. Many lenders are making home loans with very little down. Even bank regulators haven't been able to estimate the risk in today's economy. The securitization of mortgages through Wall Street and the issuance of mortgages through Government-Sponsored Agencies such as Freddie Mac and Fannie Mae continue to feed the housing market. It is simply inconceivable to many on Wall Street, Main Street, and Washington that the good times could ever come to an end.

Corporate Debt Deluge Continues

If easy money and low interest rates have helped to spawn record debt at the consumer level, it has also fed into a corporate debt frenzy. Initially, coming out of the last recession, corporations used lower interest rates to refinance debt. This helped to spur profit growth at companies during the early 90's. However, during the mid-nineties, corporations began to use debt to fund stock buybacks in an effort to drive up earnings per share. By retiring stock, companies could divide the profits between fewer shareholders. This enabled many companies to accelerate earnings at above-normal rates. In the process, corporations began to leverage their balance sheets. This is very visible today in many sectors of the S&P 500. The food industry has become highly leveraged with companies such as Kellogg's, Campbell's Soup, and Sara Lee taking on billions in debt. Even blue-chip companies such as IBM no longer carry a pristine balance sheet. IBM's total debt to asset ratio has risen to as high 32.4 as of 1999. Debt levels have been rising at many of America's blue-chip corporations. (See table below)

| IBM | Procter & Gamble | Lockheed Martin | Campbell Soup | |||||

| In Billions | 1995 | 1999 | 1995 | 1999 | 1995 | 1999 | 1995 | 1999 |

| Assets | 80,292 | 87,495 | 28,125 | 32,113 | 17,648 | 30,012 | 6,315 | 5,522 |

| Liabilities | 57,869 | 66,984 | 17,536 | 20,005 | 11,215 | 23,651 | 3,847 | 5,287 |

| Net Worth | 22,423 | 20,511 | 10,589 | 12,108 | 6,433 | 6,361 | 2,468 | 235 |

| Debt Ratios | ||||||||

| Debt/Assets | 26.9 | 32.4 | 21.8 | 29.2 | 21.5 | 39.8 | 27.3 | 60.1 |

| T-Debt/Com Equity | 97.6 | 140.0 | 70.7 | 91.3 | 68.7 | 187.9 | 69.8 | 1,411.5 |

| LT-Debt/Com Equity | 45.4 | 69.7 | 59.5 | 60.6 | 55.4 | 179.6 | 34.7 | 566.0 |

| Lt-Debt/Tot Capital | 22.8 | 29.9 | 30.9 | 29.1 | 29.6 | 62.4 | 20.5 | 37.4 |

| CFO/Debt | 49.5 | 35.7 | 58.2 | 59.1 | 34.6 | 9.0 | 68.8 | 28.1 |

| Net Debt/Shr Equity | 62.1 | 109.8 | 37.3 | 54.6 | 47.9 | 180.8 | 67.6 | 1,409.0 |

Source: Bloomberg * See explanation of terms in endnotes [7]

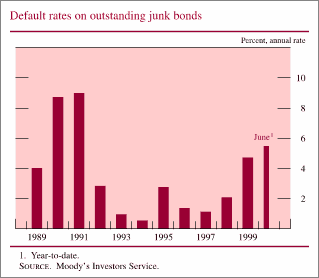

Junk Tremors

Companies have also been borrowing at record levels to fund acquisitions. According to The Wall Street Journal [8] corporate debt now represents 46% of the nation's Gross Domestic Product. Corporate debt has grown by 67% to a record .5 trillion. Even more ominous is the fact that junk bonds have soared to 9 billion. [9] Companies with the highest credit risk issue junk bonds. Even in these good times the level of defaults in the junk bond market has increased. In the last year, 5.4% of companies issuing junk bonds have defaulted on their debt. This year that ratio of defaults is expected to rise to 8%. And these are good times!

Underscoring the market's concern about the creditworthiness of borrowers, Moody's Investors Services has downgraded more debt in the business sector than it has upgraded. [10] Despite these early warnings, business credit demands continue to grow, fueled by the need for cash to finance merger and acquisition activity. According to a recent Federal Reserve report, non-financial business debt increased at a 10.5% clip in the first quarter. Recent evidence indicates that corporate borrowing remains strong during the second quarter. [11]

Underscoring the market's concern about the creditworthiness of borrowers, Moody's Investors Services has downgraded more debt in the business sector than it has upgraded. [10] Despite these early warnings, business credit demands continue to grow, fueled by the need for cash to finance merger and acquisition activity. According to a recent Federal Reserve report, non-financial business debt increased at a 10.5% clip in the first quarter. Recent evidence indicates that corporate borrowing remains strong during the second quarter. [11]

With interest rates rising, corporations, like consumers, are switching the maturity of their debt. Businesses are relying on shorter-term sources of credit. Bond interest rates have soared and credit spreads have widened between Treasury debt and corporate bonds. This fact is forcing many companies to alter their funding mix to shorter-term debt in an effort to keep interest payments low. Corporations increasingly rely on commercial paper and turn to banks for financing.

Easy Money Fuels the Fire

This apparent credit binge by consumers and corporations has been made possible by the easy credit policies of the Federal Reserve. As the graphs below indicate, the supply of money in the economy has been allowed to expand at above-normal rates. By keeping the printing presses running, the Fed has kept the financial system pumped up with liquidity. It has also served to suppress the true cost of credit by making it amply available. The Fed's job of maintaining financial liquidity and accessibility has been made easier by the help of foreigners. In addition to the Fed manning the printing presses, the U.S. trade deficit has been financed by foreign capital. Because we are currently running record trade deficits with other foreign countries, our nation has been able to finance more consumption than would have been the case if we had to rely on our own savings. The willingness of foreigners to recycle dollars into U.S. capital markets has served to support our bond and stock markets. It is doubtful whether this will continue forever. At some point, those dollars could be withdrawn from our markets.

In the meantime, the Fed continues to provide liquidity to the financial system. That fact, along with the recycling of foreign dollars, has helped to prop up our financial markets. But even our financial markets are leveraged. Last year, of the .2 trillion of credit growth in this country, approximately one-half of the new borrowing was initiated by the financial sector. [12] Unfortunately, the greater portion of that money has fed the speculative mania in our stock market.

While large financial institutions speculate with derivatives, the small investor is leveraging his bets with margin loans. Already individual investors account for more than 60% of Nasdaq trading volume. The individual investor holds over half of all margin debt. It was the doubling-up of online margin debt last fall that funded the frenzied run-up in the Nasdaq last year. As the graph on the left indicates, margin debt is also at record levels. From September 1999 to March 2000, margin debt has risen to 1.5% of total stock market value.

While large financial institutions speculate with derivatives, the small investor is leveraging his bets with margin loans. Already individual investors account for more than 60% of Nasdaq trading volume. The individual investor holds over half of all margin debt. It was the doubling-up of online margin debt last fall that funded the frenzied run-up in the Nasdaq last year. As the graph on the left indicates, margin debt is also at record levels. From September 1999 to March 2000, margin debt has risen to 1.5% of total stock market value.

Chart Source: Contrary Investor

Derivatives – A Complex and Dangerous Debt Instrument

Everyone is doing it. Banks, brokers, hedge funds, insurance companies and individual investors are using leverage to increase their investment returns. The more sophisticated of the groups are using derivatives which allows people to control large amounts of stock with little or no money up front. The margin debt at brokerage houses looks minuscule when compared to the amount of leverage on the books with derivatives. Since banks and other intermediaries began using these complex financial instruments, they have risen to over trillion. This unregulated source of leverage nearly brought the financial world to the brink in the fall of 1998 when Long Term Capital Management bet the ranch on the wrong side of interest rates. Does anyone remember Orange County back in 1994?

Wall Street remains unfettered by the risk. The financial markets seem to ignore the inherent risk and instability of credit (false prosperity). Many believe the bigger you are, the harder you fall, the more likely you are to be bailed out by the government. It is similar to sailors who ignore storm warnings on the belief that, if things get rough, the Coast Guard will come to the rescue.

Greenspan has warned of the risk of the explosion in the derivative market. No one knows whether this system of leverage will be able to withstand a period of economic weakness or a period of rising interest rates. Each time the Fed has gone through an interest rate raising cycle this decade, there has been collateral damage. It happened in 1994 and again in 1998. Martin Mayer wrote in 1999, "The one lesson history teaches in the financial markets is that there will come a day unlike any other day. At this point the participants would like to say, 'all bets are off', but in fact, the bets have been placed and cannot be changed." The leverage that once multiplied income will now devastate principal." [13]

Reg T Revisions Expand Margin Debt

While the use of derivatives by sophisticated investors continues to multiply like an uncontrolled virus, the use of margin debt by day traders continues to mushroom. Prior to 1996, the Federal Reserve, which controls margin debt under Reg T, limited margin to 50% of an initial stock purchase. Reg T rules prohibit brokerage houses from adding to customer indebtedness by lending money to their investors in order to meet margin calls. However, in 1996 the Fed revised Reg T to permit brokers to participate as a conduit for loans made through other customers. This change has allowed day-trading firms and their traders to bend the rules to arrange loans from other customers or employees of the firm.

"The House" Bends the Rules

This deregulation is a lot like having a rich uncle. It allows traders losing money to meet margin calls by borrowing additional money to pay for the losses generated by trading. In a sense, the gambler is playing with the house's money. This enables people to invest without having their own money at risk. In Vegas, this loan process would be the equivalent of the house turning to the gambler next to you and asking them to lend you their chips. Even though your credit is exhausted, it allows you to continue to play. In the financial world, it allows the house to keep the casino full with a steady stream of bets. It allows the firm's customers to buy in the morning and sell in the afternoon and make money – with none of their money at risk. (Margin is required only on positions that are held at the end of the day. If those positions are closed out by the close of the market, then no margin is required.) This finagling makes it possible for day traders to trade without ever having to pick up the tab as long as they can keep even – that is until the day of reckoning.

Debt Tsunami on Its Way

Short-Term Forecast:

At the moment, the weather forecast calls for balmy days filled with clear skies and calm seas. The stock market has been especially volatile this year, but investors remain optimistic longer-term. The economic growth rate has recently slowed down, but the financial world has confidence that Greenspan may have engineered a soft landing. At the moment no trouble appears on the horizon. And yet, if you look below the surface, something is brewing.

Stock market volatility is becoming seismic. Brokerage firms and fund managers are creating unusually large price gyrations in an effort to increase performance – moving in and out of stocks en masse based on the latest news or innuendo. Debt defaults on junk bonds are on the rise and credit agencies are on heightened alert. Consumer balance sheets continue to be burdened by additional debt; while corporations continue to leverage up their balance sheets in order to fund acquisitions or buy back stock.

Extended Forecast:

America's debt binge persists. Economists and others are concerned that those consumers and companies least able to afford debt are the ones borrowing the fastest. Bankruptcies, though off record highs, are still rising. They have grown from 0.8% to the present 1.3% of all U.S. households over the last few years. [14] At some point, all of this debt will come home to roost. Consumers can't spend and borrow forever. Eventually the reality of interest payments will set in. If growth in the economy begins to slow, and as a consequence unemployment increases, debt burdens could become unsustainable.

A retrenchment by consumers will lead to an economic slowdown or worse – even a recession. That could put an end to rising corporate profits and along with it, the bull market in stocks. A decline in the stock market will have dramatic supply and demand effects. A significant drop in stock prices would mean a loss of wealth, which also implies a reduction in consumption. Collapsing stock prices will also have a direct effect on the federal budget. The budget surpluses over the next decade assume over 0 billion in tax revenues coming from capital gains. [15] The loss of capital gain tax revenues that would come from a bear market in stocks, combined with an economic downturn, could lead once again to a large federal budget deficit.

A drop in the stock market and an economic recession might also have inflationary implications for the economy. Salaried workers might no longer be content to own stock options in lieu of higher pay. Companies would be forced to shift from options to straight wage and salary increases. A drop in the dollar resulting from a fall in our financial markets could also result in inflation.

It seems fair to conclude that the high levels of debt in our economy now pose a risk to the financial system. If there were a large drop in asset values or a significant rise in interest rates, marginal borrowers would begin to default on their loans. Margined traders might also be exposed to weakness in the stock market. In fact, a downdraft in stock prices might be accelerated as weak positions are liquidated, thus generating a downward spiral of forced selling.

The dangers of a severe and prolonged recession are being seriously underestimated. The credit expansion that has created this financial bubble is not sustainable. The Clinton Administration and the Fed daily proclaim the economic miracles of the era. In reality they have created an economic and financial bubble of epic proportion. Efforts should have been made to deflate this bubble years ago. But the political capital of this credit boom has been hard to resist. Unfortunately, our generation and our children's generation will very likely pay a substantial price for this policy failure.

In future editions of my Storm Series, I will highlight the problems of America's twin bubbles in the economy and in the stock market. The final installments of "The Perfect Financial Storm?" will include an article on the trigger mechanism that might cause the storm fronts to collide and form the perfect storm. Because I have had numerous requests on how to survive the coming financial storms, I will add a final installment on investing under storm conditions.

Many of the graphs in this article may be found in the Federal Reserve Board July 2000 Report to Congress

Continue reading with Part 3: Bear-O-Metric Pressure →

References:

[1] The Richebächer Letter, June 2000, p. 4 Subscription: 888.737.9358

[2] The Richebächer Letter, June 2000, p. 7 Subscription: 888.737.9358

[3] Bloomberg - U.S. Economy: Consumer Borrowing Rose Bln in June

[4] Federal Reserve Board July 2000 Report to Congress

[5] "Borrowing Levels Reach A Record", The Wall Street Journal, July 5, 2000

[6] Federal Reserve Board July 2000 Report to Congress

[7] T-Debt = total debt, Com Equity = common equity or total value of common stock, LT-Debt = long-term debt, Tot Cap = combination of total debt + common stock, CFO = cash flow

[8] "Borrowing Levels Reach A Record", The Wall Street Journal, July 5, 2000

[9] "Borrowing Levels Reach A Record", The Wall Street Journal, July 5, 2000

[10] Federal Reserve Board July 2000 Report to Congress

[11] Federal Reserve Board July 2000 Report to Congress

[12] Federal Reserve Board July 2000 Report to Congress

[13] "The Dangers of Derivatives" by Martin Mayer, The Wall Street Journal, May 20, 1999

[14] Federal Reserve Board July 2000 Report to Congress

[15] Congressional Budget Office

Interesting Resources