I was originally going to publish the latest article in our option series today, wrapping up our discussion on getting paid to buy stocks, but the market reaction to North Korea seems more pressing, so we’ll discuss that instead.

When most people think about potential events that could derail financial markets quickly, war seems to be near the top of that list. But counterintuitively, the prospect of war is not necessarily bad for stocks. In order to appreciate this, we need to take a look at how some prior conflicts have unfolded.

As we get into this discussion, the first thing I’d like to point out is that this is all conjecture. None of us know what events lay ahead, and therefore none of us can have any certainty in how to proceed. But the goal with any analysis is to assign probabilities to various events as accurately as possible, thereby illuminating the most advisable path forward.

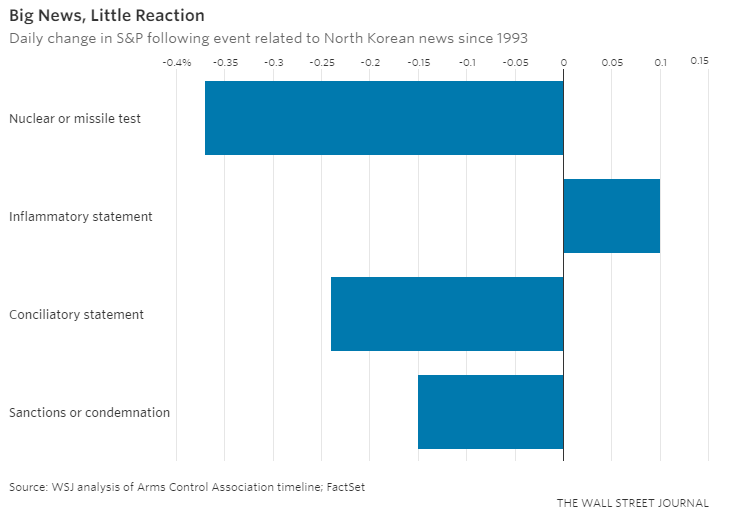

With that in mind, it’s important to recognize that the financial markets have a long history of ignoring North Korea’s provocations. Consider the chart below, courtesy of the Wall Street Journal.

This chart examines the one-day change in the S&P 500 following 80 international incidents involving North Korea’s nuclear program since 1993.

According to the Arms Control Association, there have been 36 North Korean nuclear or missile tests since 1993. Following those events, the S&P declined an average of less than 0.4%. They point out that the drop would be less than half that were it not for a big decline 19 years ago that was more directly related to Russia’s debt default rather than North Korea’s missile testing.

Interestingly, as you can see above, stocks in the US have actually risen on average following 19 inflammatory statements involving North Korea. These include North Korea’s threat to turn South Korea into a “sea of fire” in 2011 and George W. Bush’s “Axis of Evil” speech from 2002.

All of this shows that financial markets tend to be good at shrugging off events that have little impact on global trade. As I harped on last week, professional investors always view events through the lens of corporate profits. If something doesn’t stand a good chance of impacting future cash flows – which would, therefore, impact current present value calculations – most investors simply don’t care.

That being said, there is something different about the conflict this time.

So far, the US and UN have ramped up sanctions slowly in response to N. Korea’s actions. These sanctions have been specific and aimed at cutting off North Korea’s export revenues. While it’s hard to determine the effects of sanctions, the new ones imposed in Resolution 2371 attempt to cut off one-third of North Korea’s estimated billion in annual exports.

You may also like Todd Mariano: Turkey Greater Risk than North Korea

The problem is that the sanctions rely on UN members, particularly Russia and China, for implementation. Without cooperation from these countries, sanctions are likely to have little effect.

The US administration knows this well, and their frustration came to a boil with Trump’s direct warning that the US may halt trade with countries doing business with North Korea. This was seen as a direct shot at China, which purchases approximately 83% of North Korea’s exports. China is also responsible for about 85% of North Korea’s imports, based on data from MIT’s Observatory of Economic Complexity.

This threat changed the game because it brought global trade into the mix. Now we’re not talking about restrictions on trade with a tiny little hermit nation, we’re talking about trade restrictions between the top two largest economies in the world. Corporate profits are now at risk …

In my opinion, that is what the market is reacting to. The question then becomes: What do we do about it?

Before attempting to answer that question, I’d like to voice an opinion that may piss some of you off, but I think has a bit of relevance here. When I heard Trump’s threat earlier this week, I was shocked, but actually a bit pleased. In my mind, what the administration is doing is standing next to China, pulling the pin from the economic grenade, and saying, “your move.”

While this type of reaction is very scary, we have a bit of history on our side. Historically, the communist party in China has been very worried about losing power. This has forced them to take exotic measures to protect and bolster their economy. In this sense, China’s leadership may have more to lose from a trade war with the US than the US does itself.

BUT, let’s be very clear here: Any disruption to global trade will sink global stock markets. Just because it may hurt China more (politically) does not mean that our stock markets will get away unscathed. On the contrary, a disruption in trade between China and the US would hurt both of us, perhaps very significantly.

But apparently, that’s a risk that the US administration is willing to take, in an attempt to wind down this problem before it escalates further. How it works out, we’ll just have to see.

Okay, now how do we handle this from an investing perspective?

Check out Waiting for a Buy Signal

The first thing I’d like to point out is that major stock market tops do not occur as a result of geopolitical tensions, rather they occur when broad economic conditions begin to deteriorate and the best that can be seen ahead has been fully discounted in the stock market.

I don’t think we’re there yet. The global economy has been showing signs of life recently, and these types of economic moves tend to have a lot of inertia behind them. That is, they don’t stop on a dime simply because of a problem in one part of the world.

So the economic backdrop to the financial markets is currently healthy, as we’ve been pointing out for some time, but we still have to deal with this little mess. So here’s my take:

If you’re older and more concerned with capital preservation than growth, no one can blame you for taking some chips off the table. But it’s important that you understand the tradeoff to a move like this.

Risk and reward go hand in hand; while becoming defensive now may help you in the event of a worst-case scenario, it also increases the likelihood that your portfolio will underperform should all of this blow over. As long as you recognize that, taking chips off the table may be the right thing for you to do from a risk-management perspective.

Read Is the US Economy Doing Just Fine?

For those with a longer time-horizon, I would suggest watching this situation unfold carefully with an eye toward using it as a buying opportunity. This may be the type of volatility that has nothing to do with economic growth and corporate profits (assuming we don’t stop trade with China and/or Russia), and that’s the EXACT type of volatility you want to use to accumulate positions.

Why? Because once this blows over, asset prices will once again rise to reflect the outlook for global growth, which, at least now, remains healthy.

There’s another perspective here that also backs up this approach. As Spencer Jakab of the WSJ points out, the larger a potential conflagration, the smaller the market reaction should be. He notes that “If the outcome is binary – a choice between nothing happening and thermonuclear conflict – then it makes no sense to sell stocks.”

This logic seems to have prevailed during the Cuban Missile Crisis when the world came closer than ever to ending and the Industrials declined less than 1% for the week.

Another option for circumventing a potentially serious decline as this situation works itself out is buying portfolio insurance. Volatility definitely spiked yesterday, making insurance more expensive, but it still remains quite low by historical standards (a further indication that major market participants still expect this to eventually blow over).

Positions in fixed income and gold should also do well in the short-term as fear spikes and some investors seek out safe havens.

The game of Poker is a fantastic analog to geopolitical positioning that involves reading your opponent, bluffing, and putting a player on a decision. Trump appears to have done just this with his most recent warning (which Nikki Haley doubled down on at an emergency meeting of the UN Security Council).

Because China is responsible for about one-fifth of our imports and is our third-largest export market, the stakes are extremely high and many do see this as a type of “bluff,” as it would ruin both of our economies. But Trump has made trade a focus of his administration and has acted in many counterintuitive ways, so it remains to be seen how this will all play out.

Hopefully, for the sake of all of us, we can find a peaceful resolution to this madness and go back to enjoying the fruits of a global bull market. But until then, now that major trade disruption is potentially at stake, we need to be on alert with our portfolios as this situation unfolds.

The preceding content was an excerpt from Dow Theory Letters. To receive their daily updates and research, click here to subscribe. Matt is also the Chief Investment Strategist at Model Investing. For more information about algorithmic based portfolio management, click here.