Originally published at The Boock Report

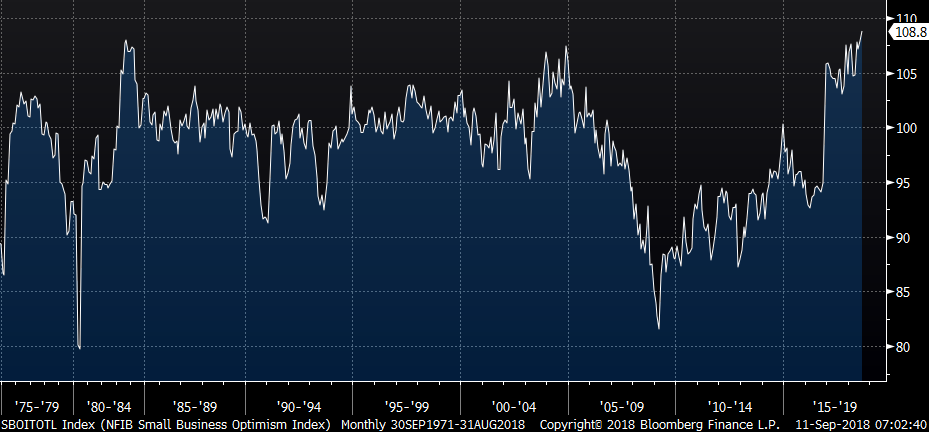

The NFIB small business optimism index for August rose almost 1 pt m/o/m to 108.8, the highest level in the history of this survey dating back to 1973. Plans to Hire rose 3 pts to the most also on record. Capital spending plans, after remaining in a range all year, finally broke above by rising 3 pts to the highest since 2006. Plans to increase inventory was up by 6 pts to the highest since 2005. This all led to those saying it's a Good Time to Expand to rise 2 pts to match the best since the question was asked in 1973. Impressive.

However, those that Expect a Better Economy fell 1 pt and those that Expect Higher Sales dropped by 3 pts to match a 4 month low. Finding those employees to fill those plans to hire continues to get more difficult as Positions Not Able to Fill rose 1 pt to the most on record and remains the 'Single Biggest Business Problem' according to NFIB. Current compensation plans held at 32%, near a multi-year high while future plans fell 1 pt after rising by 1 pt last month. Lastly, expectations for better earnings did improve by 2 pts.

The NFIB CEO bottom lined the report by saying, "As the tax and regulatory landscape changed, so did small business expectations and plans. We're now seeing the tangible results of those plans as small businesses report historically high, some record-breaking, levels of increased sales, investment, earnings, and hiring."

My bottom line is that this is great to see, especially since small business is such an engine of overall growth. We do though have to reconcile those strong results in key components with muted expectations on the economy and sales. That is, will this be more than just an inventory build? Also, when looking at confidence numbers whether via business or consumer, as opposed to hard data, when it's this good, any market participant has to ask themselves whether this is as good as it gets. At least in this cycle, it means the Fed will keep on raising interest rates. The 2 yr yield is now rising to 2.73% and the 10 yr yield is back at 2.95%, about to knock on that 3% door again. Also, if overseas growth continues to moderate, it will certainly matter at some point in the US.

NFIB SMALL OPTIMISM INDEX

We're also seeing selling in European bonds with the 10 yr German bund yield back above .40%, the highest in 5 weeks. We are 3 weeks away from the ECB cutting its monthly purchases to just 15b euros. It peaked at 80b last year. The 10 yr gilt yield is at 1.50% for the first time since May after good wage data seen today (see below). Both the ECB and BoE meet on Thursday and I expect boring meetings for both.

It's not just the ECB and BoE central bank meetings of relevance. We see some important EM ones too. The Argentinian central bank meets today, Turkey on Thursday and I have to believe they finally hike rates again. Russia meets on Friday. The pressure is, of course, extraordinary to keep on hiking in order to stabilize their currencies and inflation. The Argentines have an overnight rate now of 60%. There is serious value being created in EM from this fallout.

I keep talking about a slowdown in global trade. In case you missed it, on Friday, Taiwan (a tech bellwether) said August exports rose by 1.9% y/o/y, well less than the estimate of up 5.1% and imports were up 7.9% vs the forecast of up 15.6%. This was followed by China's trade news over the weekend. Today, the China Association of Auto Manufacturers said vehicle sales in China fell 4.6% y/o/y in August.

In the UK, for the 3 months ended July, 3k jobs were added after the solid 42k in the prior period. The estimate was up 10k. The unemployment rate did hold at 4%, the lowest since the 1970s. Encouragingly for the UK wage earner and a story being seen in the US was the 2.9% y/o/y wage gain ex-bonuses' matching the best since July 2015. The BoE is getting caught in waiting way too long in raising interest rates. Mark Carney, the author of this, today agreed to stay in his job up until January 2020. I'm not a fan, as you can probably tell, of his stewardship. The more up to date number on jobs saw August jobless claims rise by 8.7k, the 3rd straight month of gains.

The September German ZEW investor confidence index on the German economy rose 3 pts to -10.6 and that is better than the slight increase expected to -13. It is still negative though for the 6th straight month. The ZEW said “During the survey period, the currency crises in Turkey and Argentina intensified, while German industrial production and incoming orders were surprisingly low in July. Despite these unfavorable circumstances, economic expectations for Germany improved slightly. The considerable fears displayed by the survey participants regarding the economic development have diminished somewhat, which may in part be attributable to the new trade agreement between the USA and Mexico." I prefer the IFO number instead of a number of relevance. Either way, the hard data of late out of Germany, in factory orders, export orders and IP has clearly slowed as they are highly sensitive to global trade flows. The euro is little changed as this is rarely a market-moving number.

For daily macroeconomic analysis and asset class positioning, visit boockreport.com