Originally published at The Boock Report

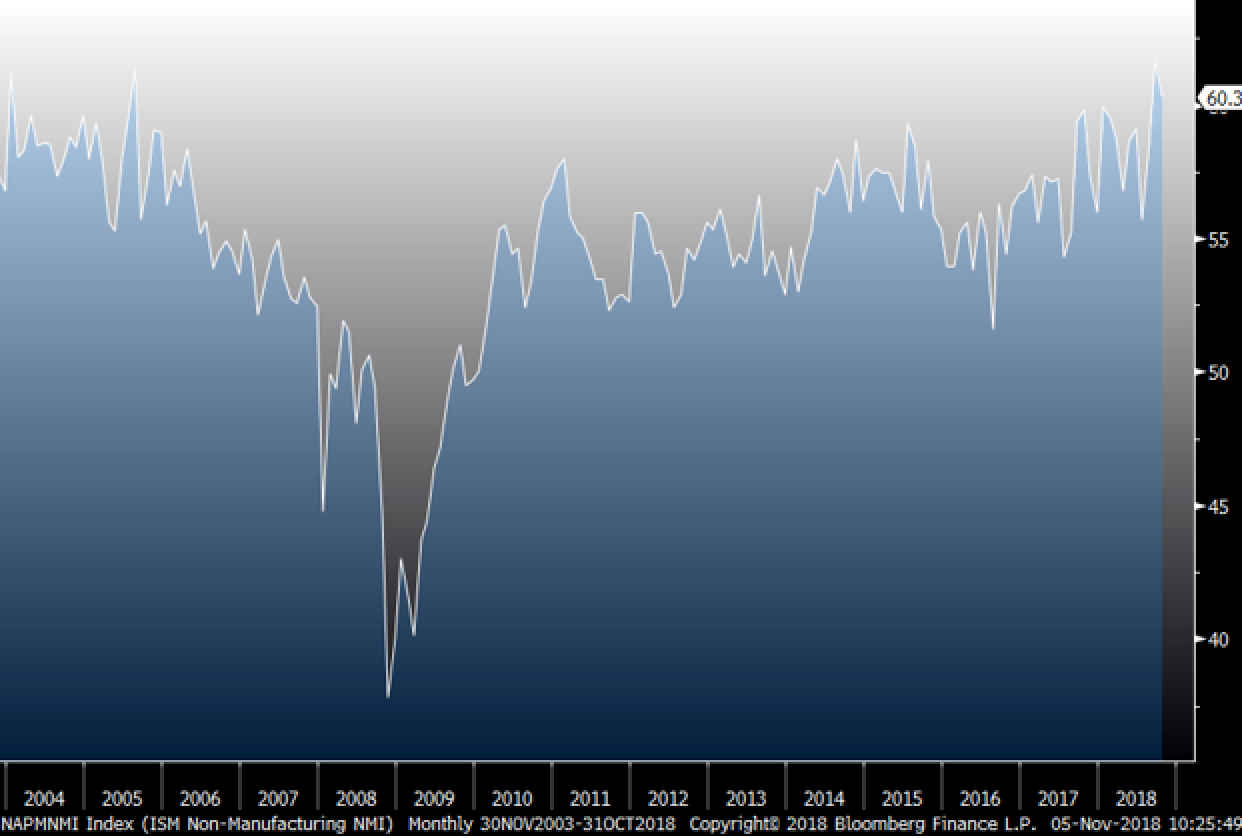

The October ISM services index fell 1.3 points to 60.3, however it was 1.3 points better than expected and is the second best print since 2005. Internally, new orders were little changed but backlogs did fall five points to a three month low. Employment fell by 2.7 points after rising by 5.7 points last month. Export orders (only some service companies report exports) were unchanged. Prices paid did recede by 2.5 points to a four month low.

The breadth of growth remained good with 17 of 18 industries surveyed seeing it. (The same number as last month.) Under the hood though, the number of industries seeing an increase in employment was 10-- the lowest since the same print in April.

The ISM summed up the report saying, “The non-manufacturing sector has again reflected strong growth despite a slight cooling off after a record month in September. There are continued concerns about capacity, logistics and tariffs. The respondents are positive about current business conditions and the economy.”

Bottom line: businesses are juggling these challenges with what is still a pretty good economic backdrop, save housing and autos. It is not an easy balance-- this tariff situation could be very binary going into year-end and capacity (labor too) and logistics constraints could stay with us well into 2019. We should focus on the continued rise in the cost of capital and how that might impact cash flows. Keep in mind too, many U.S. service companies service U.S. manufacturers that do business overseas. While that is not a direct export if the work is done in the states, service companies are still exposed to what their customer business is abroad.

Below are some of the comments from businesses that reflect the issues we’re facing. Not included are businesses in healthcare and education that are mostly immune.

“Tariffs are beginning to impact business. We ask our suppliers to hold pricing for six months, but we are experiencing difficulties.” (Construction)

“Wrapping up fiscal year budgets [and] seeing modest increases in volume and spend. Some price increases due to tariffs on computers/peripherals.” (Finance & Insurance)

“Stable at the moment. Still continuing to look at opportunities to reduce costs and improve efficiencies.” (Health Care & Social Assistance)

“The promotional-products trade continues to stay strong going into the end of the year. This reflects the overall macroeconomics of how the economy is doing thus far. We have not yet begun to see the impacts on prices due to the additional tariffs against China. We anticipate that price increases may start to work into the supply chain early in the first quarter.” (Management of Companies & Support Services)

“It has been very difficult to make decisions due to instability brought by the latest trading dispute. In this environment, clients tend to postpone capital-expenditure decisions.” (Mining)

“Increasing oil prices should provide an uptick in customer orders for our services in the fourth quarter. Conversely, it will likely lead to higher prices for consumables, specifically bulk chemicals and plastics. Also, hiring is becoming an issue, as finding suitable workers is more difficult as time passes.” (Professional, Scientific & Technical Services)

“Business has been strong. Continuing momentum seen in past month. Anticipating continued strong sales through remainder of the year.” (Retail Trade)

“Transportation capacity shortages remain our largest challenge.” (Wholesale Trade)

For daily macroeconomic analysis and asset class positioning, visit boockreport.com