Roth conversions are a powerful planning tool for retirement and can be beneficial to many individuals. The Tax Cuts and Jobs Act made this an interesting year to consider a conversion, but it’s important to understand if it’s the right choice for you as conversions are now permanent.

Why Consider a Roth Conversion Now?

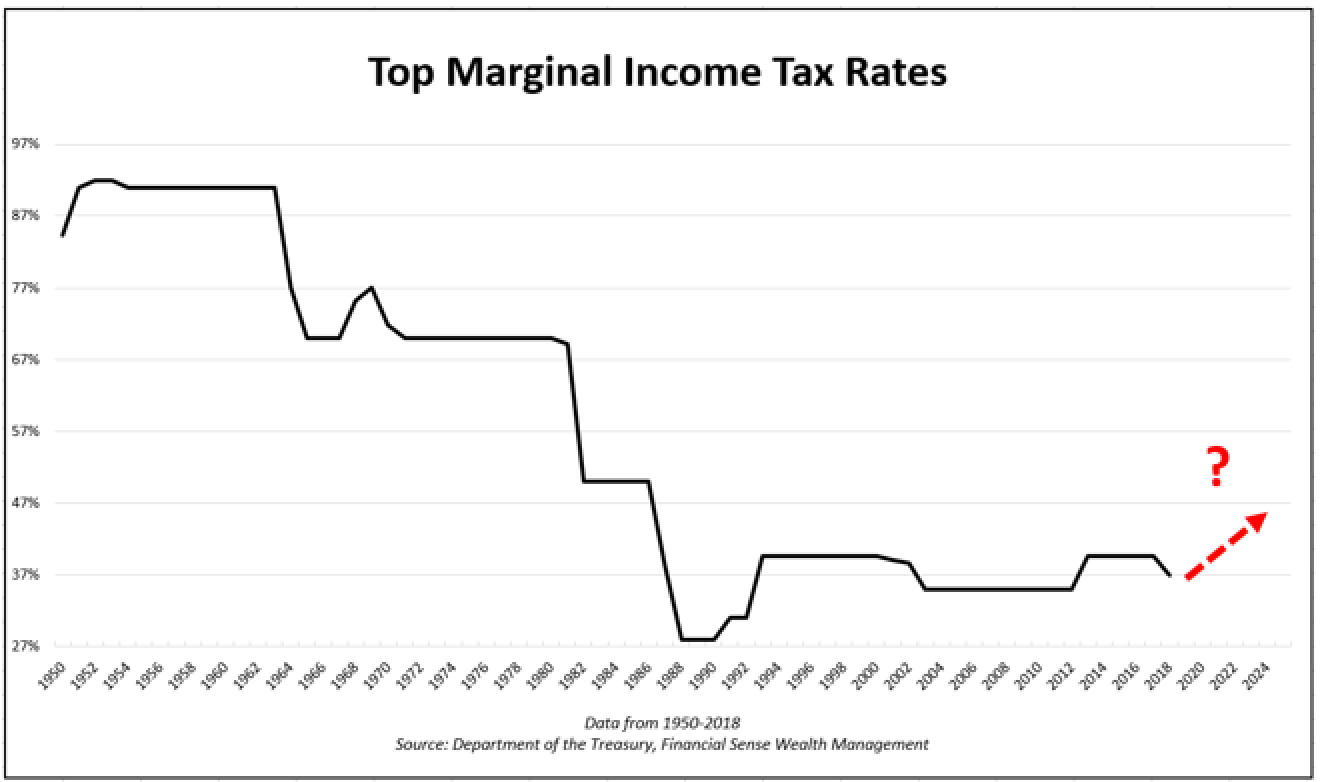

Impact of Tax Reform

With the recent tax law changes, many individuals are looking at a window of time where they will pay lower taxes. The Roth conversion becomes more attractive while you’re paying taxes at a lower rate and, historically, we are still near lows in the top marginal tax rates.

Current tax rates are unlikely to stay at these levels forever and, like many other experts, I do expect tax rates to increase in the future. With government deficits expected to reach $1 Trillion dollars next year, tax increases are anticipated to help cover the shortfall. Ideally, you’ll want to do conversions if you’re expected to be in a higher tax bracket going forward. Here's why...

Roth Conversion Advantages

1. Tax Free Growth and Withdrawals

Imagine having $100,000 at the beginning of retirement. Over 20 years at a six percent growth rate, it would increase to over $300,000. Having that money in a Roth would provide you $200,000 tax free where that same $200,000 would be taxable in a traditional IRA.

2. Tax Diversification

Diversification is not only great for investments but also for taxes. Too often, the vast majority of someone’s net worth is in a tax-deferred account like a 401(k). In retirement, when they start taking distributions, this creates more taxes that must be paid. Multiple account types like taxable, tax deferred and tax free provide greater flexibility in planning to meet expenses. Another advantage of diversification is its ability to help mitigate the potential impact of changes, and we don’t know how tax laws will change in the future so this is important to keep in mind.

3. No Required Minimum Distributions (RMDs)

The IRS requires individuals to take withdrawals from tax-deferred accounts when they reach age 70 ½. If the money is not needed, this will trigger unwanted taxes that could be avoided using a Roth account because there are no RMD requirements from the IRS.

4. Pass Money Tax Free to Heirs

When you pass, the beneficiaries will receive the money—and access to it tax free. This is a great advantage if individuals are receiving the assets but not as important if it’s going to a charity since an IRA would provide the same benefit at that point.

Disadvantages of Roth Conversion

1. Triggers additional taxes now

If the assets remain in an IRA, taxes are not due until a distribution is made. Upon completing a conversion you’re pulling forward future taxes and will increase your tax bill in the year you complete a conversion.

2. Conversions are now permanent

In the past you got a mulligan using recharacterization if needed, but unfortunately this option was removed with the recent tax changes.

3. Roth Accounts have a five-year rule

The rule requires assets be held in the Roth for five years before distributions can be tax free. This is not five years for each contribution or conversion, but simply five years from the original contribution/conversion.

When Should You Consider Roth Conversion?

- When the owner can pay the tax on conversion from non-account assets

- If there is a long-time horizon (i.e. beginning of retirement)

- When the owner anticipates that income tax rates will stay the same or increase

When Should You Not Consider a Roth Conversion?

- When the owner expects tax rates to decline or expects to be in a much lower marginal tax bracket in the future

- When there is a shorter time horizon

- If taxes on conversion are paid from the IRA/qualified plan

Roth conversions are not an all or nothing proposition.

You can choose the amount to convert. Often this leads to using what I like to call a fill-the-bucket-approach where we try and convert enough without increasing the overall tax bracket.

For example, assume a married couple has income of $100,000 per year and are interested in doing a conversion. They currently are in the 22 percent tax bracket and can have taxable income up to $165,000 before they jump to the next bracket. Using the fill-the-bucket- approach, it is simply $165k (highest income for current bracket) - $100k (current bracket) = $65k they could theoretically convert without increasing tax brackets.

Utilizing the fill-the-bucket-approach over several years can be a useful strategy for some but also consider applying it all in one year depending on your individual circumstances.

Consult with a Tax and Financial Professional

You have until year end to complete a Roth conversion so speak with a tax professional to help understand the implications of completing a conversion. Ideally, you want to complete conversions near year end when you have a better idea regarding your tax situation.

Roth conversions are most commonly done by those in or near retirement. If you are still working and would like to learn more about better alternatives in using a Roth account, read Are You Harnessing the Most Powerful Tool for Retirement?

To find out more about Financial Sense® Wealth Management and our investment services, click here to contact us.

Advisory services offered through Financial Sense® Advisors, Inc., a registered investment adviser. Securities offered through Financial Sense® Securities, Inc., Member FINRA/SIPC. DBA Financial Sense® Wealth Management.