Originally posted at ExecSpec.net

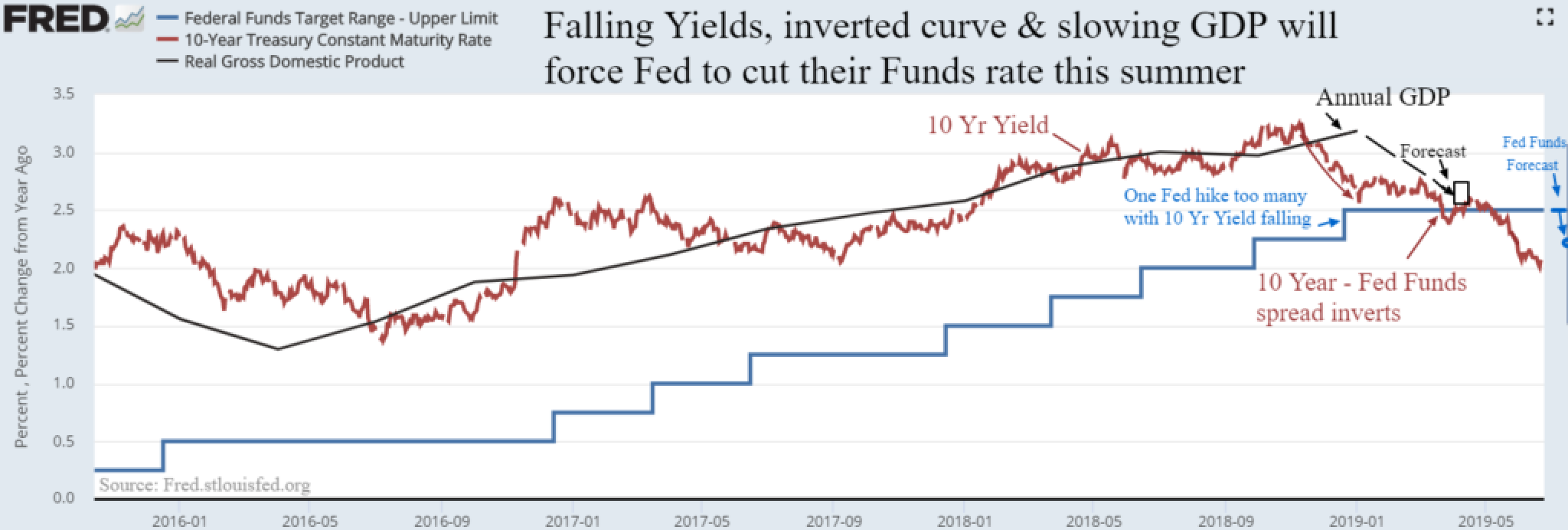

Prominent St. Louis Fed Chair James Bullard doesn’t like gaming investor expectations. The Federal Reserve has conveyed to the markets that they will not cut rates in June but hinted the Fed will oblige in late July. Bullard feels that if you see weakness now that warrants lower interest rates, as the Fed does, then why wait? Just cut rates now. Like other Federal Open Market Committee (FOMC) members, Bullard feels inflation and economic (GDP) expectations have fallen below targets and when added to the current inverted yield curve, it supports acting now for a 25-basis point cut to a 2.25% fed funds rate.

We agree with Bullard’s assessment as well as his 2018 view that rates should not have been raised so much in an effort toward “normalization” given the modest inflation data and slowing global economies. Currently James Bullard and the marketplace are expecting at least two 25 basis point rate cuts before year end 2019.

Fed Chairman Powell has only begun to see a sharp rise in global growth risks as of May 2019, downplaying falling inflation and bond spreads. Powell is a good Fed chair, but like most he appears to be overly patient and willing to fall behind the curve. Look for a Fed rate cut at the end of July, but unfortunately it will not erase the inverted yield curve the Fed created and will keep the markets expecting a further cut in September as worries persist that our economy is creeping toward a recession.

Our personal ExecSpec exposure to the manufacturing sector made us highly skeptical of the strong 3.1% first quarter GDP report as new orders and backlogs have been falling in the industrial sector since last October. The consensus for the second quarter GDP due out at the end of July is currently at 1.75 to 2%. True domestic manufacturing activity would be more in sync with a 2 to 2.5 percent GDP growth rate in early 2019 and expectations are for flat order rates through year end if there is no China trade deal.

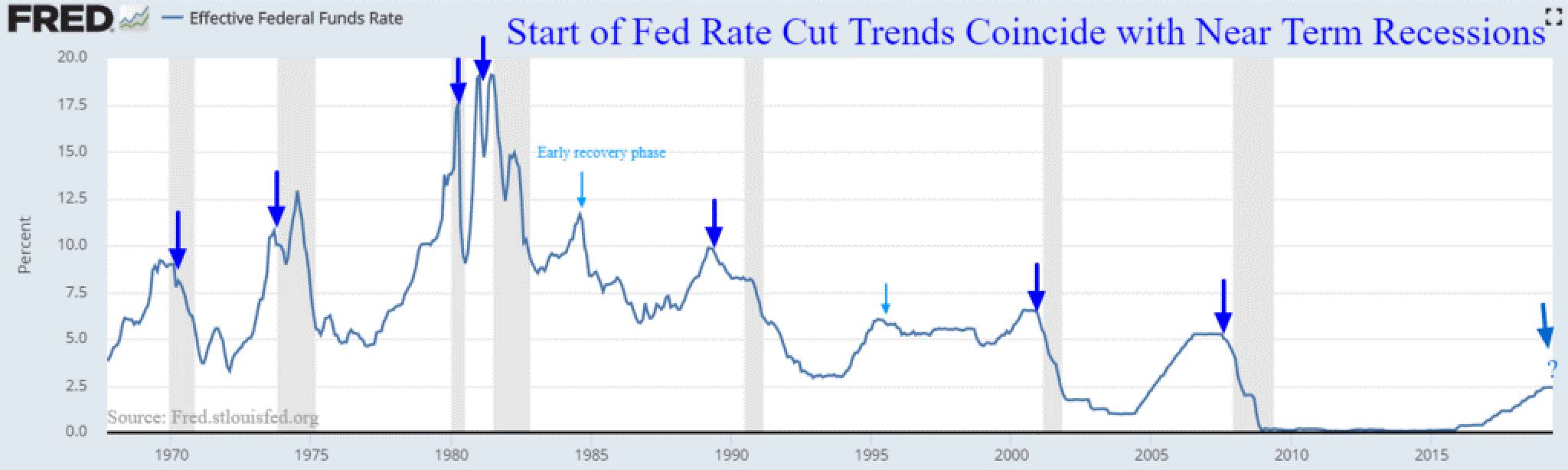

While we remain cautiously optimistic longer term, history is not on our side once the Fed begins cutting rates. Other than a couple early to mid-cycle Fed rate cut phases that had no negative impact on the economy, almost every time the Fed began a rate cut trend, the U.S. economy was heading into a recession and stocks were in trouble. Is this time different? Let’s hope so. Geopolitics are unpredictable, but the markets and the economy need a U.S. trade agreement with China more than Fed rate cuts.