Summary

- We are currently witnessing some of the largest divergences between equities and economic data

- Corporate bond spreads and treasury yields suggest there are risks being mispriced

- Ongoing trade negotiations parallel a game of prisoner’s dilemma

- No clear signs that the global growth slowdown is over

- After Powell’s testimony before congress on July 10 – green light on July rate ‘cut’

The market seems to think there are more reasons to be optimistic for the remainder of 2019 – we would be cautious to feel the same. To paint this picture, here are a few key observations we think are significant…

Divergences. Divergences Galore

Divergences don’t always precede a crisis or a market correction, but they do highlight converging signals that typically correct themselves overtime – most often there’s always a side of the market that has it wrong. We’ve highlighted a few divergences we think are noteworthy reasons to be cautious:

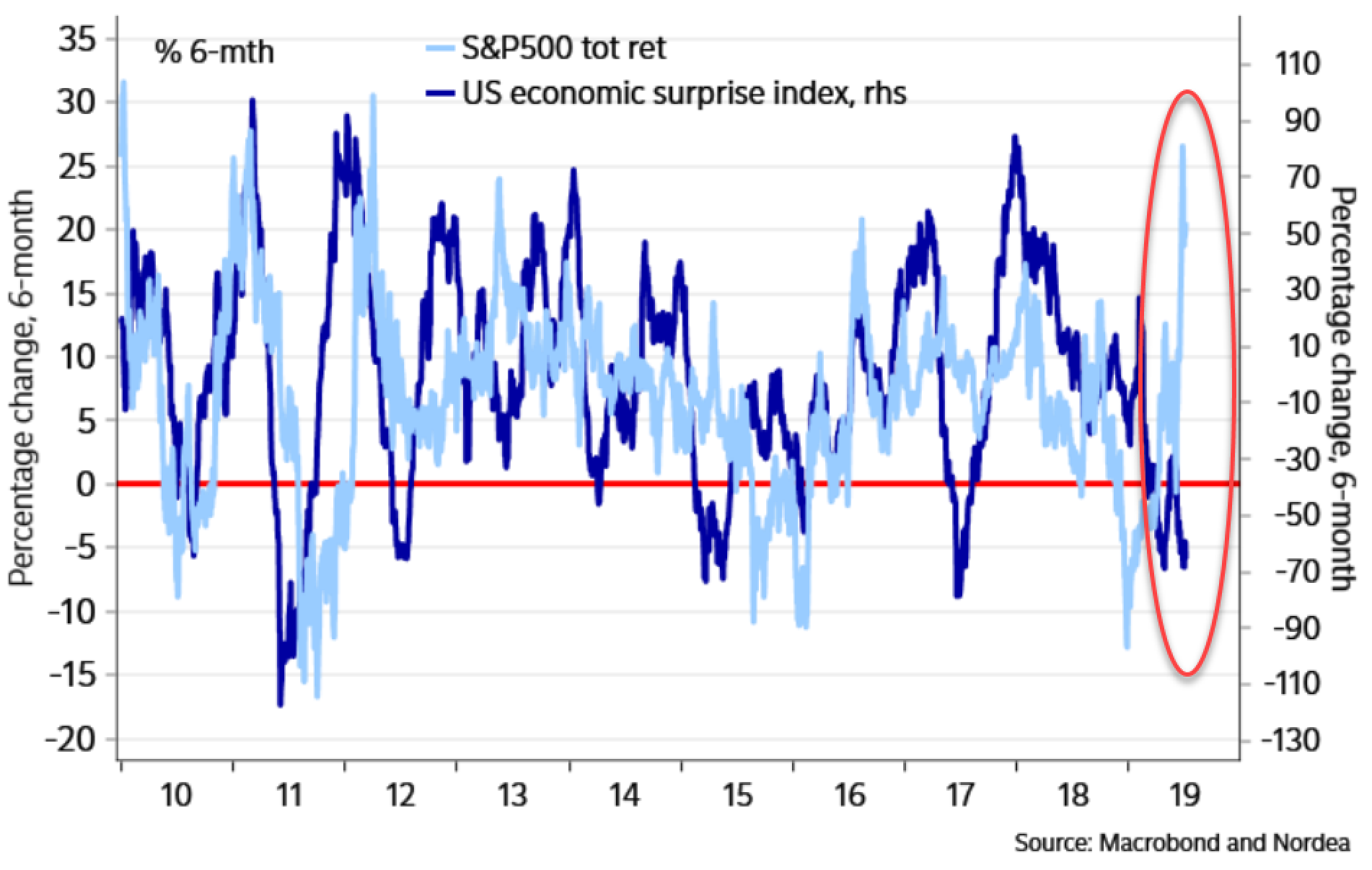

We’re currently witnessing one of the largest divergences ever between equities and U.S. macroeconomic surprises. In other words, the market is performing far better than it should, given a backdrop of deteriorating economic data.

Corporate bond spreads were closely in sync with large caps until the beginning of this year. Since January, the S&P hit new all-time highs while spreads have continued to widen – suggesting that there could be a significant mispricing of risk in equity markets.

The U.S. 10-year yield was closely in sync with the market in 2018; that is until we saw the S&P’s rally after December’s correction. Since then, market gains have not been supported by a rise in the 10-year yield – suggesting that one of the markets has it wrong. Our view is that while the 10-year continues to fall on the back of deteriorating economic data, the equity markets have yet to fully price this in.

No Clear Bottom in the Global Growth Story…Yet

An important observation Chris Puplava and others made earlier this year is that the global growth slowdown materialized before the U.S. entered a trade war with China. Trade tensions have exacerbated the story. Not to say that one event is more important than the other; our point is that it is important to understand which came first. There are two angles we take when looking at global growth picture.

The first angle is on the trade front. In recent weeks, economists and strategists developed a thesis illustrating the ongoing trade negotiations between the U.S. and China as a situation resembling a game of prisoner’s dilemma (also known as game theory).

In this framework (see figure above), both countries have two options: cooperate or escalate. In the prisoner’s dilemma, both sides will escalate if they perceive a greater benefit of doing so. However, both sides won’t choose to cooperate until each side realizes the greater payoff from cooperation and decide to independently trust the other. Most recently, at the G-20 summit in Osaka, Japan, President Trump and Chinese President Xi met to restart the trade talks. However, there was still no substantial progress on the issues that significantly divide them: how to codify IP protections, when to remove existing trade tariffs and how much to reduce the current trade deficit. According to Morgan Stanley’s Chief U.S. Public Policy and Municipal Strategist, Michael Zezas, “These conflicts reset the payoffs, suggesting that escalation is preferable at this point to meeting the other’s demands.” Any further progress should be constructive but the timeline for something substantial could very well be a 2020-2021 story, meaning that any further escalation could likely erode global growth even further.

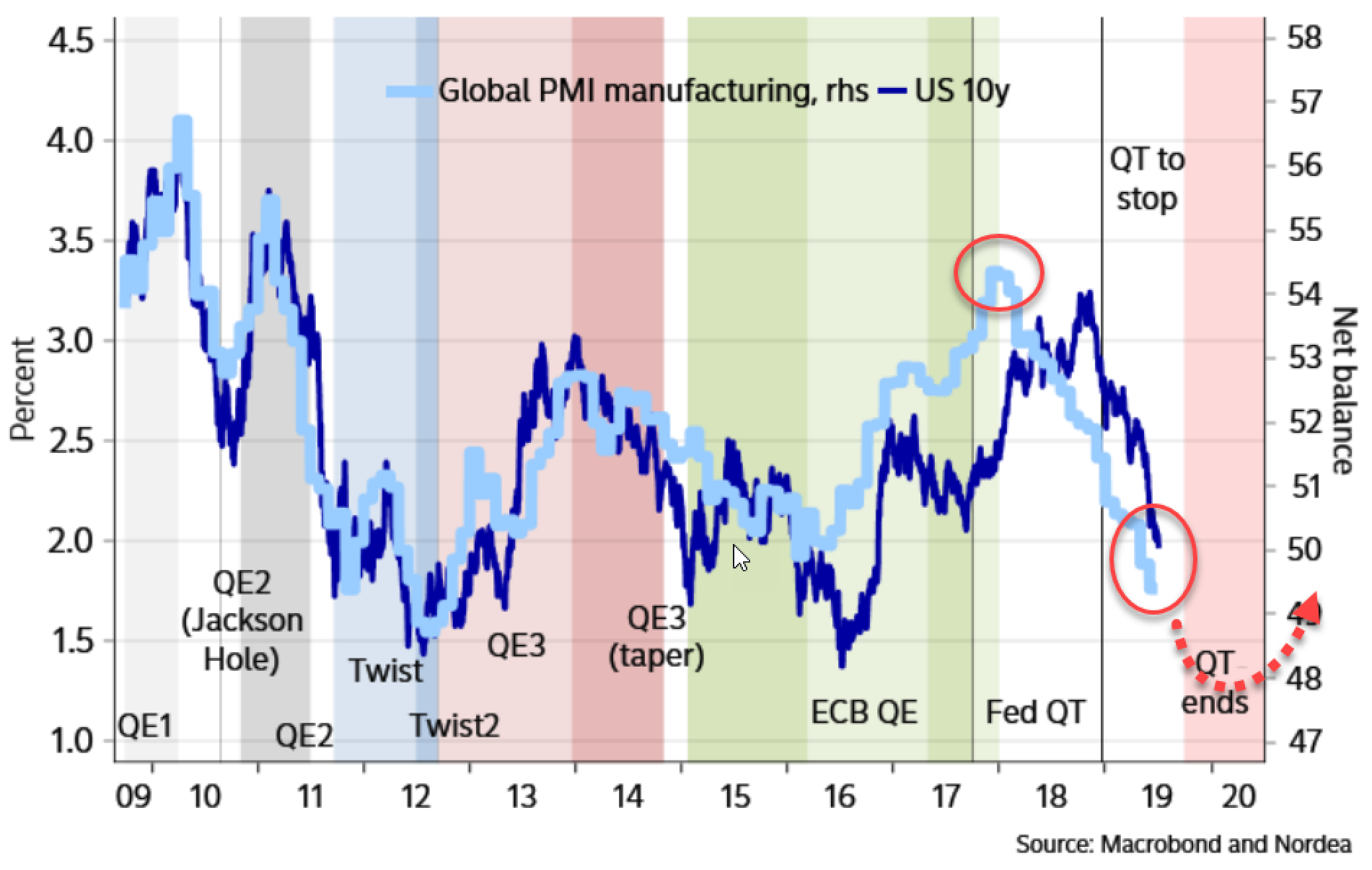

Our second angle takes into consideration the global slowdown that has already been in play since the later half of 2017. Global financial markets experienced a period of synchronized growth that began in 2016 as a result of lower interest rates, fiscal stimulus, a weaker U.S. dollar and accommodative central bank policy employed by central banks around the world. However, higher global interest rates and a stronger dollar began to splinter the fabric of the global economy – the first signs of this could be seen anywhere but in the U.S. economy. Pain was first felt overseas and global growth began to falter. Global manufacturing activity peaked in December 2017 as shown below:

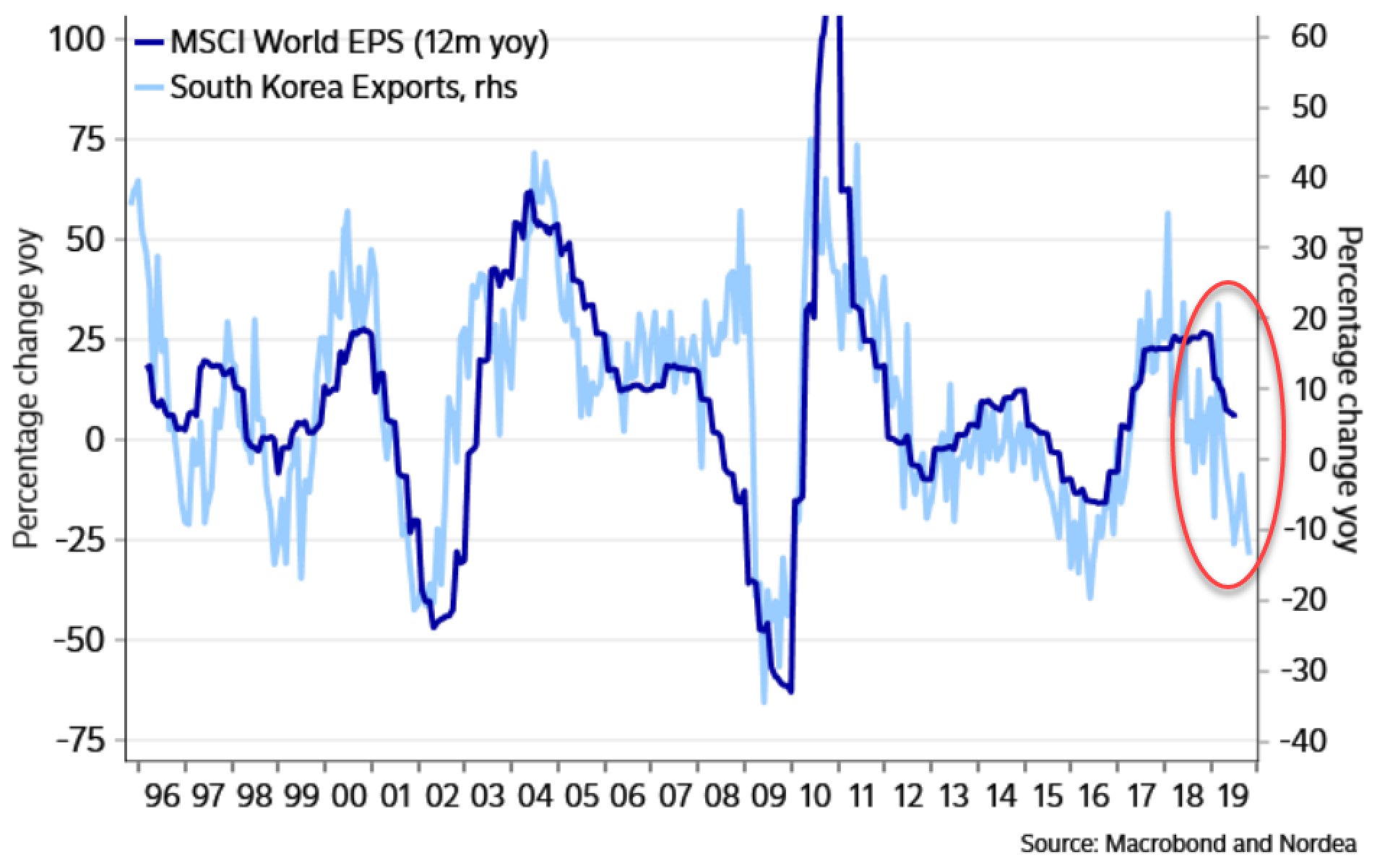

Twelve months later, China’s manufacturing activity entered contraction and reached its weakest level in three years. The most recent deterioration of global PMIs this year has mainly been driven by trade tensions. Shown below, South Korean exports, a proxy for global trade growth, have suffered in 2019 and suggest weaker earnings growth this year and into next year.

With no clear sign of a bottom, we believe the pass-through effects of further economic weakness on company balance sheets have yet to be fully priced in. This will be especially significant for companies with higher leverage and weaker balance sheets as earnings growth slows, costs rise and financial conditions tighten. Guidance and earnings revisions will be in extra focus as we enter the upcoming earnings season.

Synchronization of Global Central Bank Policy

If you aren’t too familiar with the U.S. monetary landscape over the last 12 months, I would highly suggest reading Chris Puplava’s brilliant piece from June Policy Misstep Déjà Vu?

Twelve months ago, the Fed was raising interest rates and executing its asset purchasing program at the tune of nearly $60 billion in purchases per month. Since December’s market correction, the Fed has shifted its approach to making policy decisions from ‘autopilot’ to ‘data dependent.”

In May’s FOMC meeting, the committee saw no strong case for a change in monetary policy citing encouraging data from China and the Euro area as well as reports of progress in trade negotiations in China. However, in Fed Chairman Powell’s testimony on July 10 before Congress, Powell noted since their May meeting, “these crosscurrents have reemerged, creating greater uncertainty.” Powell went on to say, “Growth indicators from around the world have disappointed on net, raising concerns that weakness in the global economy will continue to affect the U.S. economy.” As it stands now, we are facing what could be the first interest rate cut (Fed decision scheduled for July 31) since the start of the economic recovery and a Fed who is set to end its asset purchasing program in September.

The Fed isn’t the only central bank on the precipice of a new accommodative monetary cycle. The European Central Bank, India, Australia, New Zealand, and China’s central bank are also making efforts toward easier policy to help encourage bank lending to small businesses.

While the Fed joins the ‘accommodative’ party, we believe it is important to understand the dynamic at play. Typically, in the context of an expanding economy, a rate cut (accommodative policy) is effective in spurring economic growth/recovery as it incentivizes more businesses and consumers to borrow. However, in the context of an economy that has grown old after not just one or two, but three rounds of quantitative easing and a decade of sub three percent interest rates, the potency of an accommodative U.S. Fed leads us to believe that weaker economic growth may outweigh the positives of easier policy.