Inflation, and the fight against it, have been very much in the public's mind in recent years. The shrinkage in the purchasing power of the dollar in the past, and particularly the fear (or hope by speculators) of a serious further decline in the future, have greatly influenced the thinking of Wall Street.

—Ben Graham, The Intelligent Investor: The Definitive Book on Value Investing. A Book of Practical Counsel

There was once a time in this country when the average Joe didn't have to think hard about retirement. The boss took care of retirement income through a defined benefit pension plan. What the pension plan didn't cover was made up by Social Security. We were a thriftier nation back then. The savings rate was much higher and most mortgages were either paid off by retirement or the big home used to raise the family was sold, and the equity was used to downsize to a smaller home.

Today most private sector companies have switched over to defined contribution plans in the form of a 401(k). What you accumulate is what you get when you retire. Private sector retirement plans no longer offer the guaranteed income of the past unless you happen to work for, well, the government.

Not only has retirement income fallen over the past few decades, but real income has shrunk as inflation has eroded the purchasing power of the average wage earner. As shown in the table below, real incomes have all peaked and are in a current downtrend. Wages and income are no longer keeping pace with inflation.

Source: Doug Short

It's bad enough that wages are falling behind inflation but so have investment returns. The return on the S&P 500 since January of 2000 is a negative -6.74%; 17.08% if dividends were reinvested. This annualizes at 1.29% a year, hardly commensurate with the rate of inflation hovering above 3% for the last decade.

Stocks aren't the only asset class that haven't kept up either, bond yields have fallen precipitously since the recession of 2007–2009, and "cash" yields are close to zero. Even long-term bond yields offer investors returns less than the current inflation rate, and that is before taxes are paid. If you factor in taxes, the rate of return is negative. Investors are being fleeced as the government pursues a policy of financial repression (higher inflation rates and lower bond yields).

Governments Manage Debt through Low Interest Rates: Bad News for Fixed Income Investors

As U.S. budget deficits balloon out of control the government has very few options to deal with a growing debt problem. Throughout history, debt/GDP ratios have been reduced by:

- Economic growth

- Substantial fiscal adjustment/austerity plans

- Explicit default or restructuring of private and/ or public debt as we now see in Greece;

- A sudden burst of inflation (hyperinflation, think Argentina), or

- A steady dosage of financial repression that is accompanied by an equally steady dosage of inflation.

In their paper "The Liquidation of Government Debt," authors Carmen H. Reinhart and M. Belen Sbrancia argue that periods of high indebtedness have been associated with a rising incidence of default or restructuring of public and private debts.

A subtle type of debt restructuring takes the form of "financial repression." Financial repression includes directed lending to government by captive domestic audiences (such as pension funds), explicit or implicit caps on interest rates, regulation of cross-border capital movements, and (generally) a tighter connection between government and banks. In the heavily regulated financial markets of the Bretton Woods system, several restrictions facilitated a sharp and rapid reduction in public debt/GDP ratios from the late 1940s to the 1970s. Low nominal interest rates help reduce debt servicing costs while a high incidence of negative real interest rates liquidates or erodes the real value of government debt. Thus, financial repression is most successful in liquidating debts when accompanied by a steady dose of inflation.1

The authors argue that the more subtle and gradual form of restructuring, or "taxation," through financial repression was used successfully by western governments to reduce their debt burdens after World War II. In essence, financial repression in combination with inflation played an important role in reducing government debt.

For investors and today's retirees, financial repression has important implications. The pillars of financial repression are twofold: explicit or indirect caps on interest rates, and a steady dose of inflation created by government deficits, financed by money printing.

Addressing Low Interest Rates through Dividend Strategies

In a low interest rate environment accompanied by a steady dose of inflation what are the investment options available to investors? As far as the problem of stagnating wages, I don't have an answer other than getting a government job, develop an athletic skill and play professional sports, become a rock star or Hollywood actor, or start a business that provides a product or service that consumers demand.

I do have an option for today's yield starved investors or those who plan to retire and live comfortably: dividend-paying blue-chip stocks. Investing in blue-chip stocks is probably not at the top of your investment list. After two great bear markets in 2000–2002 and 2007–2009, S&P 500 returns have been negative for the last 12 years unless you reinvested your dividends.

The key here is dividends. It may come as a surprise to most investors but stocks historically provided a higher yield than bonds by the very nature of risk. For most of the last century dividend yields on equities were above the interest rate on bonds. It wasn't until the 1960s when inflation rates began to rise that bond yields rose above the yield offered on stocks. This has generally been the case since the '60s until recently.

Today the spread between bonds and stocks has narrowed considerably. In many cases, the yields are higher. As shown in the table below, the dividend yield on the Dow Industrials and the Dow Utilities exceeds the yield on all Treasury notes. The yield on the S&P 500 is slightly above the rate of interest offered on a 10-year treasury note.

| STOCK INDEX YIELDS | TREASURY YIELDS | |||

| Dow Industrials | 2.51% | 2-yr notes | 0.27% | |

| Dow Utilities | 4.08% | 5-yr notes | 0.85% | |

| S&P 500 | 2.00% | 10-yr notes | 1.98% | |

Even the tech-laden NASDAQ is paying a dividend yield of one percent. Many of the tech giants such as Microsoft (MSFT), Intel (INTC), and now Apple (AAPL) are paying dividends. In fact, many of the former high-flying technology companies like Intel and Microsoft offer dividend yields that compete with the yield on 10-yr treasury notes and 30-yr treasury bonds. Even better is the fact that their dividends have been growing at an annual rate of 14–15% per year.

When you think of the stock market most investors think in terms of growth. During the Great Bull Market of 1982–2000 the S&P 500 appreciated 1153.94%. If you had reinvested all of your dividends the rate of return rose to 2041.47%, a total return of 19.02% per year.

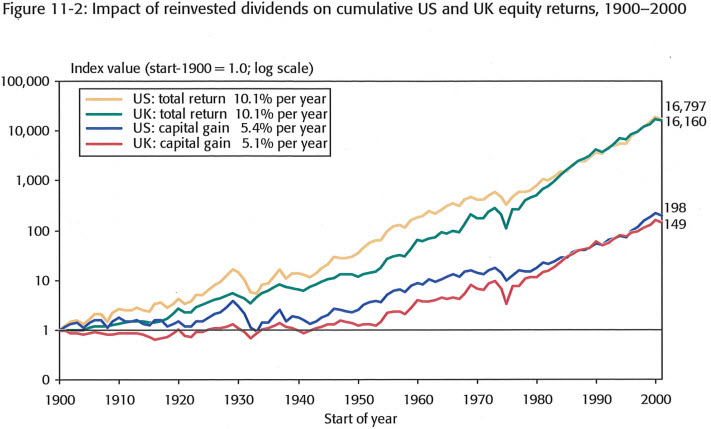

What becomes obvious is the role that dividends play in total return (dividends plus price appreciation). In their seminal work "Triumph of the Optimists: 101 Years of Global Investment Returns," authors Dimson, Marsh and Staunton document the key role that dividends play in investment returns. In the short term, year-to-year performance is driven by capital appreciation, while long-term returns are influenced heavily by reinvested income. The questions for today's investor is: are investment returns driven mainly by price movements and capital gains or by dividends? A U.S. equity portfolio started in 1900 with an initial investment of would have ended 2000 with a value of 8. This represents an annual compound growth rate of 5.4 percent per year. If dividends were reinvested that same would have grown to ,797, an annualized return of 10.1 percent.2

Triumph of the Optimists validates the role that dividends play in enhancing investment returns. This effect is not specific to the United States. This holds true in all of the 16 major markets they covered in their 101 year study. Accordingly, the longer the investment horizon, the more important dividend income becomes.

Source: Triumph of the Optimists: 101 Years of Global Investment Returns, by Elroy Dimson, Paul Marsh, & Mike Staunton, p 151

During the Debt Super Cycle from 1980 to 2007 the role of dividends in investment returns diminished as growth occupied a greater portion of investment returns. Companies within the S&P 500 focused more on increasing earnings per share growth. This was accomplished through stock buybacks and acquisitions. Stock buybacks increased earnings per share while acquisitions increased both the top and bottom line. The result was that the historical dividend payout ratio fell from an 86 year average of 58.1% to today's current payout of 30%.

It is my belief that in an era of financial repression and negative real interest rates, dividends are going to play a more important role in investment returns. There is plenty of room for companies to increase payouts as cash levels and profit levels are well above current payout ratios. I'll have more to say about that in a moment. The more important point I would like to stress is that in an era of financial repression stocks provide a superior return than bonds and T-bills. As shown below the real returns on stocks exceeded the inflation rate and other financial asset classes such as bonds and bills in every decade over the 101 year study of Triumph of the Optimists.

Source: Source: Triumph of the Optimists, by Elroy Dimson, Paul Marsh, & Mike Staunton, p 47

In fact, in every time period under consideration equities outperformed cash and fixed income instruments. These time periods included the great bear of 1906–1907, 1912–1914, 1928–1932, and 1972–1974.

Despite some very scary stock market declines history shows that a strong period of recovery follows. The following two charts from a Federal Reserve Bank of San Francisco show both the declines and recoveries that followed market troughs. The severe stock market distress of 1928–1932 was followed by a five year recovery that saw the Dow advance by nearly 400 percent.3

Source: Federal Reserve Bank of San Francisco

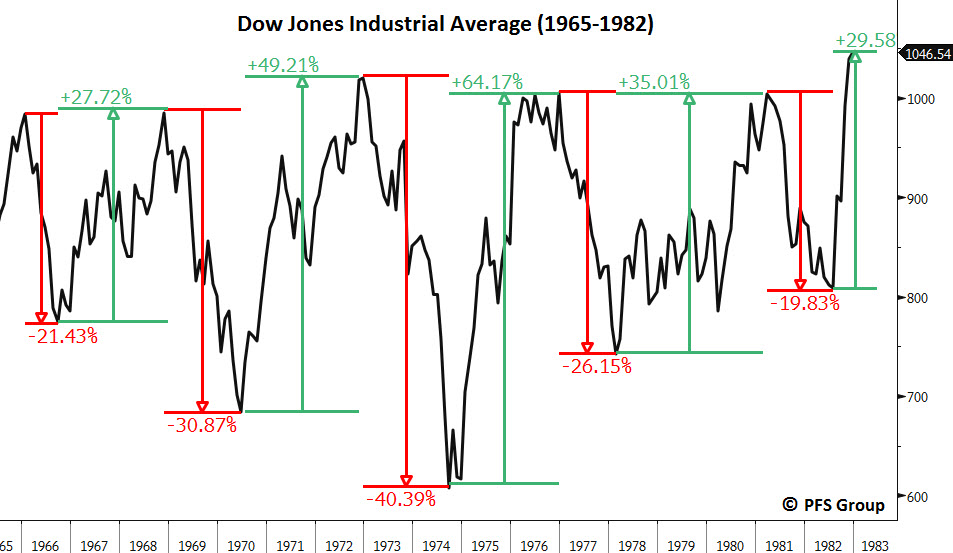

As I pointed out in my last article, "The Story Nobody Wants to Hear", secular bear markets, which can often last more than a decade, are periodically punctuated by sharp cyclical bull markets as shown in the graph of the 1965–1982 secular bear market.

Flight to Bonds Not Exactly a Flight to Safety

Today, investors are flocking to the perceived safety of government bonds in record numbers. Over the last three years almost trillion has flowed into bond funds, with over billion of inflows during the first week of April alone. With each new hiccup in the stock market, investors liquidate stocks and pour billions into bond mutual funds.

At the institutional level the BOBO trade (Bernanke on/Bernanke off or risk on/risk off) can change weekly or monthly. At the individual level the "risk off" trade is in full bloom and ongoing since the credit crisis began in 2007. Each new hiccup in the market causes an exodus out of stocks. During the first six trading days of April, when the S&P 500 shed 68 points, investors poured almost billion into bond funds, a monthly rate of billion if continued. If this trend remains in force for another three years investors will have transferred close to .5 trillion into bonds. All of this is taking place at a time when official Fed policy is to leave interest rates unchanged until at least late 2014. Recently one Fed governor suggested maintaining low interest rates until 2015–2016 as a distinct possibility if the unemployment rate doesn't improve.

On the surface investors flocking into sovereign bonds appears to be understandable. Investors are frightened by what they have experienced—two bear market declines of nearly forty percent in the last decade have left very deep emotional scars. Friends in the business tell me they have clients who call and demand to be taken out of their positions at any cost. "Just get me out," seems to be a common refrain.

The headlines appear frightening. Trillion-dollar budget deficits, sovereign debt downgrades, trillions of dollars of central bank money printing doesn't seem to deter investors from the signs of trouble in the debt markets. A graph of Greek, Spanish, Italian, and Portuguese yields should be a warning as to what may lie ahead for sovereign debt. (Note: increasing yields mean falling bond prices)

To the average investor the risk of bond yields reversing after falling for 30 years seems inconceivable, especially when compared to equity prices which have gone nowhere over the past 12 years. If one considers probabilities, given the global propensity for central banks to print even larger amounts of money, odds favor stocks over bonds. A study of stock market history would also favor this outcome. The following graph depicts S&P 500 earnings yield and the yield difference on 10-year treasury notes. The earnings yield on stocks is plus 2 standard deviations above the norm. The last time this happened was in 2009 and we now know what followed: a 103 percent gain in the S&P. Similar outcomes followed the 1974, 1979, and 1981 bear markets where spreads between the two rose to similar heights. These outcomes are rare events. When they do occur contrarians should take notice.

Look Beyond Fixed Income

In summary, I have shown that wages and investment returns haven't kept pace with inflation over the last twelve years. With ballooning budget deficits that have led to record government debt, which shows no signs of abating, "financial repression" has now become official U.S. government policy. With government debt at nose bleed levels Washington has shown no appetite for austerity. Government spending continues to rise and is now becoming a larger component of GDP. Financial repression is going to be with us for the balance of this decade. Fed officials have spoken clearly that they intend to leave interest rates at zero until at least late 2014, and maybe beyond. This means investors will have to look elsewhere to fill in their investment and income gap.

One way to fill that gap is dividend-paying blue-chip stocks. The authors of Triumph of the Optimists have shown that over the last century investment returns have been superior when dividends are reinvested. The compound return is almost double when long time frames are considered. What I have also tried to show is that major market declines are followed by strong market recoveries. Even more important is that within a long-term secular bear market there can be numerous cyclical bull markets. When investors think of the Great Depression and the stock market crash that led to an 86% decline in the Dow Industrials, that decline was followed by the Dow Industrials advancing close to 400% over a five year period.

In Part II of "How to Give Yourself an Annual Pay Raise", I will illustrate the practical application of using dividends to fill the income gap from investments and retirement plans. In addition, I plan on covering stock market risk, bear markets, stock market crashes, and the impact of quantitative easing on asset returns. Given the uncertainty in the economy and the markets, safe, secure dividends from strong blue-chip companies may be one of the few alternatives that are available to investors. They can help bridge the gap between zero interest rates, higher rates of inflation, and stagnant wages.

Disclaimer: The opinions of James J Puplava are for informational and educational purposes only and should not be considered as a solicitation or offer to purchase or sell any securities. The investments, investment strategies, and investment philosophies presented each involve their own unique risk factors that do not take into account suitability, objectives or risk tolerance. Financial Sense and its parent company shall not be liable for any financial losses that result from investing in any companies profiled. Invest at your own risk.

References

1 The Liquidation of Government Debt, Carmen M. Reinhart and M. Belen Sbrancia, NBER Working Paper Series, Working Paper 16893, March 2011

2 Triumph of the Optimists: 101 Years of Global Investment Returns, by Elroy Dimson, Paul Marsh, & Mike Staunton, Princeton University Press (2002), p 151

3 Federal Reserve Bank of San Francisco, "Ask Dr. Econ", February 2001